McDonalds 2000 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2000 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

purchases under the program to $3.3 billion or 91.1 million shares.

The Company expects to purchase the remaining $1.2 billion under

the program in 2001.

In order to reduce the overall cost of treasury stock purchases,

the Company sells common equity put options in connection with its

share repurchase program and receives premiums for these options.

During 2000, the Company sold 16.8 million common equity put

options and received premiums of $56 million, which were reflected

in shareholders’ equity as a reduction of

the cost of treasury stock purchased. At

December 31, 2000, 21 million common

equity put options were outstanding.

During February 2001, 4.2 million com-

mon equity put options were exercised

for $175 million. The remaining options

expire at various dates through

November 2001, with exercise prices

between $30.11 and $32.26.

Given the Company’s returns on equity

and assets, management believes it is

prudent to reinvest a significant portion

of earnings back into the business and use free cash flow for share

repurchases. Accordingly, the common stock dividend yield is modest.

However, the Company has paid dividends on common stock for

25 consecutive years and has increased the dividend amount every

year. Additional dividend increases will be considered after reviewing

returns to shareholders, profitability expectations and financing needs.

Beginning in 2000, cash dividends are declared and paid on an

annual, instead of quarterly, basis. As in the past, future dividends

will be declared at the discretion of the Board of Directors.

Financial position and capital resources

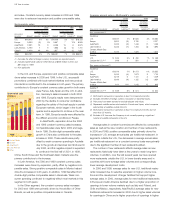

Total assets and returns

Total assets grew by $700 million or 3% in 2000 and $1.2 billion or

6% in 1999. At year-end 2000 and 1999, more than 65% of consoli-

dated assets were located in the major markets excluding Japan.

Net property and equipment rose $723 million in 2000 and repre-

sented 79% of total assets at year end.

Operating income is used to compute return on average assets,

while net income is used to calculate return on average common

equity. Month-end balances are used to compute both average

assets and average common equity.

Returns on assets and equity

2000 1999 1998(1)

Return on average assets 15.9% 16.6% 16.4%

Return on average common equity 21.6 20.8 19.5

(1) Excludes Made For You costs and the special charge. Including Made For You

costs and the special charge, return on average assets was 14.7% and return

on average common equity was 17.1%.

In 2000, return on average assets declined primarily due to lower

returns in emerging markets, which require substantial investment in

infrastructure to support rapid restaurant growth, as well as investing

in Other Brands. In general, returns benefited from the Company’s

continued focus on more efficient capital deployment. This included

a more prudent site selection process, leasing a higher proportion

of new sites, the U.S. building program that began in 1998, and the

use of free cash flow for share repurchases. Also contributing to the

increases in return on average common equity in 2000 and 1999

were increases in the average amount of common equity put

options outstanding, which reduced average common equity.

Financings and market risk

The Company is exposed to the impact of interest-rate changes and

foreign currency fluctuations. McDonald’s strives to minimize these

risks by employing established risk management policies and proce-

dures and by financing with debt in the currencies in which assets

are denominated. See summary of significant accounting policies

on page 40 for additional information regarding the use of financial

instruments and the impact of new accounting rules on derivatives.

The Company uses global capital markets along with various

techniques to meet its financing requirements and reduce interest

expense. For example, foreign currency exchange agreements in

conjunction with borrowings help obtain desired currencies at attrac-

tive rates and maturities. Accordingly, foreign currency-denominated

debt as a percent of total debt fluctuates based on market

conditions. Interest-rate exchange agreements effectively convert

fixed-rate to floating-rate debt, or vice versa. The Company also

manages the level of fixed-rate debt to take advantage of changes

in interest rates.

The Company uses foreign currency debt and derivatives to

hedge foreign currency royalties, intercompany financings and

long-term investments in foreign subsidiaries and affiliates. This

reduces the impact of fluctuating foreign currencies on net income

and shareholders’ equity. Total foreign currency-denominated debt,

including the effects of foreign currency exchange agreements, was

$5.1 billion and $5.3 billion at year-end 2000 and 1999, respectively.

Debt highlights

2000 1999 1998

Fixed-rate debt as a percent of total debt 58% 70% 67%

Weighted-average annual interest

rate of total debt 5.8 5.9 6.6

Foreign currency-denominated debt

as a percent of total debt 60 76 75

Total debt as a percent of total capitalization

(total debt and total shareholders’ equity) 48 43 43

Moody’s and Standard & Poor’s have rated McDonald’s debt

Aa2 and AA, respectively, since 1982. Fitch (formerly Duff & Phelps)

began rating our debt in 1990 and currently rates it AA. A strong

rating is important to the Company’s global development plans. The

Company has not experienced, and does not expect to experience,

difficulty in obtaining financing or refinancing existing debt. At year-

end 2000, the Company and its subsidiaries had $1.9 billion available

under committed line of credit agreements and $561 million under

shelf registrations for future debt issuance. In early 2001, the

Company reduced the amount available under committed line of

credit agreements to $1.5 billion.

34 Year in review