McDonalds 2000 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2000 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52

|

|

the Company reduced home office staffing by approximately

500 positions, consolidated certain home office facilities and reduced

other expenditures in a variety of areas. The special charge was

composed of $85.8 million of employee severance and outplacement

costs, $40.8 million of lease cancellation and other facilities-related

costs, $18.3 million of costs for the write-off of technology invest-

ments made obsolete as a result of the productivity initiative and

$15.1 million of other cash payments made in 1998. The initiatives

identified in the home office productivity plan were completed as of

December 31, 1999, and no significant adjustments were made to

the original plan.

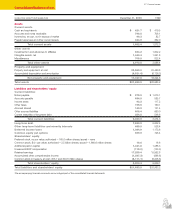

Debt financing

Line of credit agreements

At December 31, 2000, the Company had several line of credit

agreements with various banks totaling $1.9 billion, all of which

remained unused at year-end 2000. Subsequent to year end, the

Company reduced these line of credit agreements to $1.5 billion,

consisting of the following: a $750.0 million line with a renewable

term of 364 days and fees of .04% per annum on the total commit-

ment, with a feature that allows the Company to convert the

borrowings to a one-year term loan at any time prior to expiration;

a $500.0 million line expiring in February 2006 with fees of .06%

per annum on the total commitment; $250.0 million in lines expiring

during 2001 and fees of .04% per annum on the total commitment;

and a $25.0 million line with a renewable term of 364 days and fees

of .07% per annum on the total commitment. Borrowings under the

agreements bear interest at one of several specified floating rates

selected by the Company at the time of borrowing. In addition, cer-

tain subsidiaries outside the U.S. had unused lines of credit totaling

$751.4 million at December 31, 2000; these were principally short

term and denominated in various currencies at local market rates of

interest. The weighted-average interest rate of short-term borrowings,

composed of U.S. Dollar and Euro commercial paper and foreign

currency bank-line borrowings, was 6.9% at December 31, 2000

and 6.1% at December 31, 1999.

Exchange agreements

The Company has entered into agreements for the exchange of

various currencies, certain of which also provide for the periodic

exchange of interest payments. These agreements expire through

2005 and relate primarily to the exchange of Euro. The notional

principal is equal to the amount of foreign currency or U.S. Dollar

principal exchanged at maturity and is used to calculate interest

payments that are exchanged over the life of the agreement. The

Company has also entered into interest-rate exchange agreements

that expire through 2012 and relate primarily to Euro, U.S. Dollars

and Japanese Yen. The net value of each exchange agreement

based on its current spot rate was classified as an asset or liability.

Net interest is accrued as either interest receivable or payable, with

the offset recorded in interest expense.

The counterparties to these agreements consist of a diverse

group of financial institutions. The Company continually monitors its

positions and the credit ratings of its counterparties, and adjusts

positions as appropriate. The Company does not have significant

exposure to any individual counterparty and has entered into master

agreements that contain netting arrangements. The Company’s

policy regarding agreements with certain counterparties is to require

collateral in the event credit ratings fall below A- or in the event that

aggregate exposures exceed certain limits as defined by contract. At

December 31, 2000, no collateral was required of counterparties and

the Company was not required to collateralize any of its obligations.

At December 31, 2000, the Company had purchased foreign

currency options outstanding (primarily Euro, Japanese Yen and

British Pounds Sterling) with a notional amount equivalent to

$453.0 million. The unamortized premium related to these foreign

currency options was $10.6 million, and there were no related

deferred gains recorded as of year end. Forward foreign exchange

contracts outstanding at December 31, 2000 (primarily British

Pounds Sterling, Hong Kong Dollars and Euro) had a U.S. Dollar

equivalent of $781.8 million.

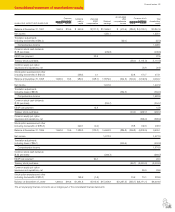

Fair values

December 31, 2000

IN MILLIONS Carrying amount Fair value

Liabilities

Debt $8,154.7 $8,344.0

Notes payable 275.5 275.5

Foreign currency exchange agreements (1) 43.7 45.6

Total liabilities 8,473.9 8,665.1

Assets

Foreign currency exchange agreements (1) 39.6 39.2

Interest-rate exchange agreements (2) 16.3

Net debt $8,434.3 $8,609.6

Purchased foreign currency options $ 10.6 $ 16.9

(1) Gross notional amount equivalent to $462.6 million.

(2) Notional amount equivalent to $2.9 billion.

The carrying amounts for cash and equivalents, notes receivable

and forward foreign exchange contracts approximated fair value.

No fair value was provided for noninterest-bearing security deposits

by franchisees as these deposits are an integral part of the overall

franchise arrangements.

The fair values of debt, notes payable obligations, foreign currency

and interest-rate exchange agreements and foreign currency options

were estimated using various pricing models or discounted cash

flow analyses that incorporated quoted market prices. The Company

has no current plans to retire a significant amount of its debt prior to

maturity. Given the market value of its common stock and its signifi-

cant real estate holdings, the Company believes that the fair value of

its total assets was substantially higher than the carrying value at

December 31, 2000.

Financial review 43