Siemens 2008 Annual Report Download - page 231

Download and view the complete annual report

Please find page 231 of the 2008 Siemens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

|

|

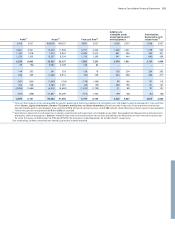

Notes to Consolidated Financial Statements 135

(in millions of €, except where otherwise stated and per share amounts)

credit agencies, in order to be awarded supply contracts. In addition, the Company provides direct vendor

nancing and grants guarantees to banks in support of loans to Siemens customers when necessary and

deemed appropriate.

Impairment – Siemens tests at least annually whether goodwill has suffered any impairment, in accordance

with its accounting policy. The determination of the recoverable amount of a division to which goodwill is allo-

cated involves the use of estimates by management. The recoverable amount is the higher of the division’s fair

value less costs to sell and its value in use. The Company generally uses discounted cash ow based methods to

determine these values. These discounted cash ow calculations use ve-year projections that are based on the

nancial budgets approved by management. Cash ow projections take into account past experience and repre-

sent management’s best estimate about future developments. Cash ows after the planning period are extrapo-

lated using individual growth rates. Key assumptions on which management has based its determination of fair

value less costs to sell and value in use include estimated growth rates, weighted average cost of capital and tax

rates. These estimates, including the methodology used, can have a material impact on the respective values

and ultimately the amount of any goodwill impairment. Likewise, whenever property, plant and equipment and

other intangible assets are tested for impairment, the determination of the assets’ recoverable amount involves

the use of estimates by management and can have a material impact on the respective values and ultimately the

amount of any impairment.

Employee benet accounting – Obligations for pension and other post-employment benets and related net

periodic benet costs are determined in accordance with actuarial valuations. These valuations rely on key

assumptions including discount rates, expected return on plan assets, expected salary increases, mortality rates

and health care trend rates. The discount rate assumptions reect the rates available on high-quality xed-

income investments of appropriate duration at the balance sheet date. Expected returns on plan assets assump-

tions are determined on a uniform basis, considering long-term historical returns and asset allocations. Due

to changing market and economic conditions the underlying key assumptions may differ from actual develop-

ments and may lead to signicant changes in pension and other post-employment benet obligations. Such

differences are recognized in full directly in equity in the period in which they occur without affecting prot or

loss. For a discussion of the current funding status and a sensitivity analysis with respect to the impact of certain

critical assumptions on the net periodic benet cost see Note 24.

Siemens has implemented and will continue to run restructuring projects, such as the SG&A program

announced in scal year 2008. The program will result in a reduction of primarily administrative workforce.

Costs in conjunction with terminating employees and other exit costs are subject to signicant estimates and

assumptions. See Note 5 for further information.

Provisions – Signicant estimates are involved in the determination of provisions related to onerous contracts,

warranty costs and legal proceedings. A signicant portion of the business of certain operating divisions is per-

formed pursuant to long-term contracts, often for large projects, in Germany and abroad, awarded on a competi-

tive bidding basis. Siemens records a provision for onerous sales contracts when current estimates of total con-

tract costs exceed expected contract revenue. Such estimates are subject to change based on new information as

projects progress toward completion. Onerous sales contracts are identied by monitoring the progress of the

project and updating the estimate of total contract costs which also requires signicant judgment relating to

achieving certain performance standards, for example in the IT service business, the Mobility Division and the

Energy Sector as well as estimates involving warranty costs.