Sony 1998 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 1998 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

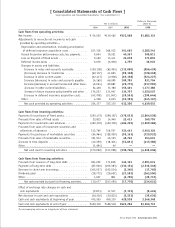

[46] Sony Corporation Annual Report 1998

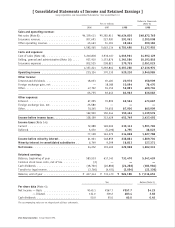

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The financial instruments including financial assets and liabilities that Sony holds in the normal course of business are

continuously exposed to fluctuations in markets, such as currency exchange rates, interest rates, and stock prices of

investments. In applying a consistent risk management strategy in order to remove adverse effects caused by market

fluctuations in the cash flow value of these financial instruments, Sony hedges the market risk of these financial

assets and liabilities by using derivative financial instruments which include foreign exchange forward contracts,

foreign currency option contracts, interest rate swap agreements, and interest rate and currency swap agreements.

Sony utilizes foreign exchange forward contracts and foreign currency option contracts primarily to fix the cash flow

value resulting from accounts receivable and payable and future transactions denominated in foreign currencies in

relation to the core currencies (Japanese yen, U.S. dollars, and German marks) of Sony’s major operating units.

Interest rate swap agreements and interest rate and currency swap agreements are used to diversify funding methods

and lower funding costs. Sony’s basic policy is to use fixed interest rates when procuring funds for investments having

a long-term recovery period and variable interest rates for funding requirements of a short-term nature, such as

working capital. The above swaps are utilized to enable Sony to choose between fixed and variable interest rates

depending on how the funds are to be used, as well as to hedge foreign exchange risks that result when assets

denominated in one currency are funded by liabilities denominated in a different currency. Sony uses these derivative

financial instruments solely for risk hedging purposes as described above, and no derivative transactions are held or

used for trading purposes. In addition, bond option contracts are used as an integral part of short-term investing

activities in order to fix the yields from bonds held by Sony Life Insurance Co., Ltd. on hand to certain ranges. Note

that among the market risks described above, no specific hedging activities are taken against the price fluctuations of

stocks held by Sony as marketable securities (refer to Notes 2 and 12 of Notes to Consolidated Financial Statements).

Sony measures the effect of market fluctuations on the value of financial instruments and derivatives by using

Value-at-Risk (herein referred to as “VaR”) analysis. VaR measures a potential maximum amount of loss in fair value

resulting from adverse market fluctuations, for a selected period of time and at a selected level of confidence. Sony

uses the variance/co-variance model in calculation of VaR. The calculation includes financial instruments such as cash

and cash equivalents, time deposits, marketable securities, non-lease short- and long-term borrowings and debt,

investments and advances and all derivatives including transactions for risk hedging held by Sony Corporation and

consolidated subsidiaries. Sony calculates VaR for one day from the portfolio of financial instruments and derivatives

as of March 31, 1998, at a confidence level of 95%.

Based on this assumption, Sony’s consolidated VaR at March 31, 1998 is calculated to be ¥6.9 billion ($52

million), which indicates the potential maximum loss in fair value resulting from market fluctuations in one day at a

95% confidence level. By item, the VaR of currency exchange rate risk is calculated to be ¥7.2 billion ($55 million)

which mainly consists of risks arising from the volatility of the exchange rates between yen and U.S. dollars in which

relatively large amount of financial assets and liabilities and derivative transactions is maintained. VaR of interest

rate risk and stock price risk are calculated to be ¥3.4 billion ($26 million) and ¥3.3 billion ($25 million), respec-

tively. The net VaR for Sony’s entire portfolio is smaller than the simple aggregate of VaR for each component of

market risk. This is due to the fact that market risk factors such as currency exchange rates, interest rates, and stock

prices are not completely independent, thus have the effect of offsetting a portion of overall profits and losses.

The calculated VaR does not include the effect of accounts receivable and payable and anticipated transactions

denominated in foreign currencies as of March 31, 1998, that are the object of Sony’s derivative hedging. Therefore,

the above amount of VaR does not reflect the full effect of the hedging activities and Sony expects that the actual risk

would be less than the disclosed VaR if those accounts receivable and payable are taken into account in the calcula-

tion. The disclosed VaR amount simply represents the calculated potential maximum loss on the following day and by

no means indicates an estimate of future loss.