Sony 1998 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 1998 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

[56] Sony Corporation Annual Report 1998

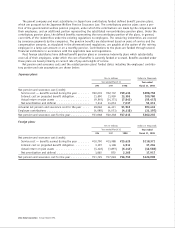

Derivative financial instruments

Derivative financial instruments, which include foreign exchange forward contracts, foreign currency option con-

tracts, interest rate swap agreements, and interest rate and currency swap agreements, are used in the company’s

risk management of foreign currency and interest rate risk exposures of its financial assets and liabilities.

Foreign exchange forward contracts

Foreign exchange forward contracts are used to limit exposure to losses, resulting from changes in foreign

currency exchange rates, on accounts receivable and payable and anticipated transactions denominated in foreign

currencies. Foreign exchange forward contracts which are designated and effective as hedges of such currency

exchange rate risk on existing assets and liabilities are marked to market and included as an offset to foreign

exchange gains/losses recorded on the existing assets and liabilities. Such contracts on anticipated transactions,

including contracts used to hedge intercompany foreign currency commitments which do not qualify as firm

commitments, are marked to market with changes in value recognized in foreign exchange gains/losses.

Foreign currency option contracts

The company enters into purchased foreign currency option contracts to limit exposure to losses, resulting from

changes in foreign currency exchange rates, on accounts receivable and anticipated transactions denominated in

foreign currencies. The company also enters into written foreign currency option contracts, of which the majority

are part of range forward contracts corresponding to the purchased foreign currency option contracts. The carry-

ing values of all foreign currency option contracts are marked to market with changes in value recognized in

foreign exchange gains/losses.

Interest rate swap agreements and interest rate and currency swap agreements

The company enters into interest rate swap agreements or interest rate and currency swap agreements in order to

lower funding costs, to diversify sources of funding and to limit the company’s exposure to loss in relation to under-

lying debt instruments resulting from adverse fluctuations in interest rates or foreign currency exchange rates. The

related interest differentials paid or received under the interest rate swap agreements and under the interest rate

and currency swap agreements are recognized over the terms of the agreements in interest expense. Currency swap

portions of the interest rate and currency swap agreements which are designated and effective as hedges of expo-

sure to losses resulting from changes in foreign currency exchange rates on underlying debt denominated in foreign

currency are marked to market and included as an offset to foreign exchange gains/losses on the underlying debt.

After an underlying hedged transaction is settled or ceases to exist, all changes in fair value of related derivatives

which have not been settled are recognized in foreign exchange gains/losses.

Net income per share

In February 1997, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Stan-

dards No.128 (FAS 128), “Earnings per Share” (EPS), which replaces the presentation of primary earnings per share

with a presentation of basic EPS and also requires dual presentation of basic and diluted EPS with an appropriate

reconciliation of both computations. Basic EPS is computed based on the average number of shares of common stock

outstanding during each period and diluted EPS assumes the dilution that could occur if securities or other contracts

to issue common stock were exercised or converted into common stock or resulted in the issuance of common stock.

Net income per share is appropriately adjusted for any free distributions of common stock. FAS 128 was effective for

both interim and annual periods ending after December 15, 1997. All prior-period EPS data presented have been

restated to conform with FAS 128.

Free distribution of common stock

On occasion, the company may make a free distribution of common stock which is accounted for either by a transfer

of the applicable par value from additional paid-in capital to the common stock account or with no entry if free

shares are distributed from the portion of previously issued shares accounted for as excess of par value in the com-

mon stock account. Under the Japanese Commercial Code, a stock dividend can be effected by an appropriation of

retained earnings to the common stock account by resolution of the general stockholders’ meeting, followed by a

free share distribution with respect to the amount appropriated by resolution of the Board of Directors’ Meeting.

Common stock issue costs

Common stock issue costs are directly charged to retained earnings, net of tax, in the accompanying consolidated

financial statements as the Japanese Commercial Code prohibits charging such stock issue costs to capital accounts

which is the prevailing practice in the United States of America.