APC 2011 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2011 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

82011 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC

KEY FIGURES 2011

>

Key figures 2011

SCHNEIDER ELECTRIC

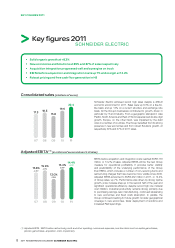

•Solid organic growth at +8.3%

•New economies and Solutions at 39% and 37% of sales respectively

•Acquisition integration progressed well and synergies on track

•EBITA before acquisition and integration costs up 7% and margin at 14.2%

•Robust pricing and free cash flow generation in H2

Consolidated sales (in billions of euros)

07

17.3

11

22.4

08

18.3

09

15.8

10

19.6

Schneider Electric achieved record high sales despite a diffi cult

economic environment in 2011. Sales were up 8.3% on a like-for-

like basis and up 14% on a current structure and exchange rate

basis. All the Group’s businesses contributed to growth, driven in

particular by IT and Industry. From a geographic standpoint, Asia

Pacifi c, North America and Rest of World experienced double digit

growth. Europe, on the other hand, was impacted by the debt

crisis in a number of countries. The Group benefi ted from its strong

presence in new economies and from robust Solutions growth, at

respectively 39% and 37% of 2011 sales.

Adjusted EBITA (1) (in millions of euros and as a % of sales)

(1) Adjusted EBITA : EBITA before restructuring costs and other operating income and expenses (one-time items such as capital gains/losses,

pension gains/losses, acquisition costs, impairment).

15.6%

2,704

15.9%

2,912

13.0%

2,048

15.4%

3,019

14.4%

3,232

07 1108 09 10

EBITA before acquisition and integration costs reached EUR3,178

million , or 14.2% of sales. Adjusted EBITA will be the new Group

measure for operational profi tability. It provides better visibility

and predictability of the underlying performance of the Group

than EBITA, which includes a number of non-recurring items and

restructuring charges that have become more volatile since 2009.

Adjusted EBITA amounted to EUR3,232 million in 2011, or 14.4%

of Group sales, up 7%. Performance was driven by strong topline

growth, price increase step-up in the second half of the year and

signifi cant operational effi ciency, despite record high raw material

cost infl ation. Industrial productivity remains strong primarily due

to purchasing savings, lean manufacturing, continued rebalancing

to new economies and fi xed costs absorption. In parallel, the

Group continued investing for future growth: broader geographical

coverage in new economies, faster deployment of solutions and

increased R&D spendings.