APC 2011 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2011 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

52011 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC

INTERVIEW WITH EMMANUEL BABEAU

EXECUTIVE VICE PRESIDENT FINANCE, MEMBER OF THE MANAGEMENT BOARD

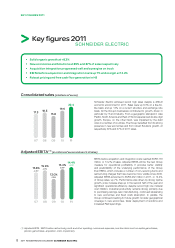

Schneider Electric reached a new record in sales in

2011. How was this performance achieved?

Indeed, we generated record high sales of EUR22.4 billion in 2011,

in comparison with less than EUR14 billion fi ve years ago. This is

the result of a successful long term strategy built upon balancing

organic growth and acquisitions, and on our leading position in high

growth geographies as well as in energy management solutions.

Schneider Electric has fi rst of all delivered solid organic growth

at +8.3%: growth in new economies reached +15%, as in 2010,

and solutions growth accelerated to +12%. These trends were

seen across the Group’s businesses, with growth around +10%

for Industry and IT, and between +7% and +8% for Power and

Infrastructure.

Finally, the deployment of our strategy has been reinforced by

acquisitions such as Telvent for real-time critical infrastructure

management, but also with Luminous, Steck, or Leader & Harvest

in new economies. Acquisitions brought additional growth of 7%

this year.

Is your growth strategy comforted by the fi nancial

results?

Yes, because Schneider Electric also achieved record high results.

Our EBITA* before acquisition and integration costs reached

EUR3.2 billion, up 7%.

However we faced a diffi cult environment, notably with political

instability in Africa and the Middle East, and above all with the

natural disaster in Japan in March and its terrible consequences.

We always privileged our employees’ security but our local

operations were disrupted and our electronic purchases impacted.

The steep raw material infl ation entailed additional costs of over

EUR400million. These diffi culties penalized our margin evolution.

We have nevertheless put in place strong actions to offset these

headwinds by raising the sales prices and controlling our costs. Our

free cash fl ow generation amounting to EUR1.7billion in the second

half was a record.

Over the full year, our Group share net income was up 6% at

EUR1,820million, the highest ever achieved by Schneider Electric.

We will therefore offer a dividend of EUR1.70 per share to our

shareholders, fully paid in cash.

Our net fi nancial debt amounts to EUR5.3 billion, up mainly due

to the dividend pay-out of EUR0.9 billion and to acquisitions for

EUR2.9billion. Our balance sheet is particularly strong, with a solid

net debt to adjusted EBITDA ratio at 1.4x and a free cash fl ow

generation capacity maintained at a very high level.

How do you consider the Group’s outlook for 2012?

The uncertainty surrounding the global economy limits our visibility.

We see continued strength in new economies and opportunities

from a recovering North America, while Western Europe is expected

to weigh on growth.

In this context we foresee fl at to slightly positive organic growth

for sales and an adjusted EBITA margin between 14% and 15%.

But the Group enters 2012 with the strength of its well diversifi ed

geographic and end-market exposure, leadership position across

its businesses that will continue to be very promising in the years

to come, and a clear advantage of its unique organization model

built for excellence in our commercial effi ciency and fi nancial

performance.

What are your ambitions for Connect, the new

company program?

We have just launched Connect which was successively presented

to our teams, our shareholders and investors and to our stakeholders

generally. This company program will obviously be key to accelerate

the development of SchneiderElectric by2014, on all dimensions

including customers, markets and development of our teams. We

have also expressed our ambition to drive the improvement of our

fi nancial results. We therefore reiterate our target of an average

organic growth at world GDP + 3 points across the economic

cycle. This growth should allow us to generate an adjusted EBITA

margin between 13% and 17%, depending on the global economic

conditions and our effi ciency initiatives. Additionally, the quality of

our cash generation and our discipline in terms of industrial and

fi nancial investments should allow us to generate a Return on

Capital Employed (ROCE) between 11% and 15%. Our ambition

is therefore to put Schneider Electric in a dynamic of continuous

profi table growth, consistent with our commitment to sustainable

development.

*EBITA: EBIT before amortization and impairment of purchase accounting intangibles and impairment of goodwill

>

Interview with

Emmanuel Babeau

EXECUTIVE VICE PRESIDENT FINANCE,

MEMBER OF THE MANAGEMENT BOARD