Coca Cola 2003 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

• the war in Iraq and continued overall political unrest in the Middle East;

• poor weather conditions in Japan and parts of North America;

• fewer consumers in North American restaurants, hotels and leisure channels;

• outbreak of Severe Acute Respiratory Syndrome (‘‘SARS’’);

• product recall in Japan surrounding two successful new products; and

• accusations, which we believe to be false, that our soft drinks in India contain high levels of pesticides.

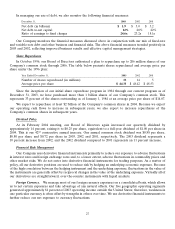

Financial Strategies and Risk Management

The following strategies are intended to optimize our cost of capital. We consider these strategies to be of

critical importance in pursuing our goal of maximizing share-owner value.

Debt Financing

Our Company maintains debt levels we consider prudent based on our cash flow, interest coverage and

percentage of debt to capital. We use debt financing to lower our overall cost of capital, which increases our

return on share-owners’ equity.

As of December 31, 2003, our long-term debt was rated ‘‘A+’’ by Standard & Poor’s and ‘‘Aa3’’ by Moody’s,

and our commercial paper program was rated ‘‘A-1’’ and ‘‘P-1’’ by Standard & Poor’s and Moody’s, respectively.

In assessing our credit strength, both Standard & Poor’s and Moody’s consider our capital structure and

financial policies as well as aggregated balance sheet and other financial information for the Company and

certain bottlers including Coca-Cola Enterprises Inc. (‘‘CCE’’) and Coca-Cola Hellenic Bottling Company S.A.

(‘‘CCHBC’’). While the Company has no legal obligation for the debt of these bottlers, the rating agencies

believe the strategic importance of the bottlers to the Company’s business model provides the Company with an

incentive to keep these bottlers viable. If our credit ratings were reduced by the rating agencies, our interest

expense could increase. Additionally, if certain bottlers’ credit ratings were to decline, the Company’s share of

equity income could be reduced as a result of the potential increase in interest expense for these bottlers.

The rating agencies monitor our interest coverage ratio. Generally, this ratio is computed as income before

taxes plus interest expense, divided by the sum of interest expense and capitalized interest. The interest coverage

ratio was 32x, 28x and 20x, respectively, for the years ended December 31, 2003, 2002 and 2001. Rating agencies

often exclude unusual items from the calculation; however, we calculated the ratios based on our

reported results.

We monitor our interest coverage ratio and, as previously indicated, the rating agencies consider our ratio

in assessing our credit ratings. However, as described above, the rating agencies aggregate financial data for

certain bottlers with our Company when assessing our debt rating. As such, the key measure is the aggregate

interest coverage ratio of the Company and certain bottlers. Both Standard & Poor’s and Moody’s employ

different aggregation methodologies and have different thresholds for the aggregate interest coverage ratio.

These thresholds are not necessarily permanent nor are they fully disclosed to our Company.

Our global presence and strong capital position give us access to key financial markets around the world,

enabling us to raise funds with a low effective cost. This posture, coupled with active management of our mix of

short-term and long-term debt, results in a lower overall cost of borrowing. Our debt management policies, in

conjunction with our share repurchase programs and investment activity, can result in current liabilities

exceeding current assets.

26