Coca Cola 2003 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

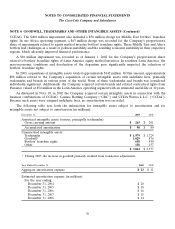

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 9: FINANCIAL INSTRUMENTS (Continued)

The contractual maturities of these investments as of December 31, 2003 were as follows (in millions):

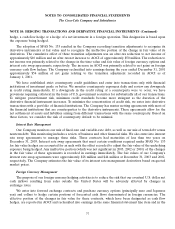

Available-for-Sale Held-to-Maturity

Securities Securities

Fair Amortized Fair

Cost Value Cost Value

2004 $ 190 $ 190 $ 2,162 $ 2,162

2005–2008 — — 1 1

After 2008 4 4 — —

Equity securities 143 232 — —

$ 337 $ 426 $ 2,163 $ 2,163

For the years ended December 31, 2003, 2002 and 2001, gross realized gains and losses on sales of

available-for-sale securities were not material. The cost of securities sold is based on the specific

identification method.

NOTE 10: HEDGING TRANSACTIONS AND DERIVATIVE FINANCIAL INSTRUMENTS

Our Company uses derivative financial instruments primarily to reduce our exposure to adverse fluctuations

in interest rates and foreign exchange rates and, to a lesser extent, in commodity prices and other market risks.

When entered into, the Company formally designates and documents the financial instrument as a hedge of a

specific underlying exposure, as well as the risk management objectives and strategies for undertaking the hedge

transactions. The Company formally assesses, both at the inception and at least quarterly thereafter, whether the

financial instruments that are used in hedging transactions are effective at offsetting changes in either the fair

value or cash flows of the related underlying exposure. Because of the high degree of effectiveness between the

hedging instrument and the underlying exposure being hedged, fluctuations in the value of the derivative

instruments are generally offset by changes in the fair values or cash flows of the underlying exposures being

hedged. Any ineffective portion of a financial instrument’s change in fair value is immediately recognized in

earnings. Virtually all of our derivatives are straightforward over-the-counter instruments with liquid markets.

Our Company does not enter into derivative financial instruments for trading purposes.

The fair values of derivatives used to hedge or modify our risks fluctuate over time. We do not view these

fair value amounts in isolation, but rather in relation to the fair values or cash flows of the underlying hedged

transactions or other exposures. The notional amounts of the derivative financial instruments do not necessarily

represent amounts exchanged by the parties and, therefore, are not a direct measure of our exposure to the

financial risks described above. The amounts exchanged are calculated by reference to the notional amounts and

by other terms of the derivatives, such as interest rates, exchange rates or other financial indices.

On January 1, 2001, the Company adopted SFAS No. 133, as amended by SFAS No. 137 and SFAS No. 138.

SFAS No. 133 was further amended by SFAS No. 149. SFAS No. 149, which did not have a material impact

effect on our financial statements, became effective beginning July 1, 2003. These statements require the

Company to recognize all derivative instruments as either assets or liabilities in our balance sheets at fair value.

The accounting for changes in the fair value of a derivative instrument depends on whether it has been

designated and qualifies as part of a hedging relationship and, further, on the type of hedging relationship. At

the inception of the hedging relationship, the Company must designate the derivative instrument as a fair value

76