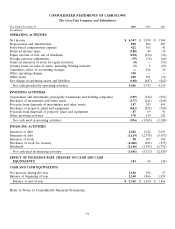

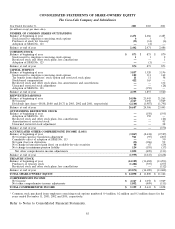

Coca Cola 2003 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 1: ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

assets determined to have definite lives are amortized over their useful lives. We review such trademarks and

other intangible assets with definite lives for impairment to ensure they are appropriately valued if conditions

exist that may indicate the carrying value may not be recoverable. Such conditions may include an economic

downturn in a geographic market or a change in the assessment of future operations. All goodwill is assigned to

reporting units, which are one level below our operating segments. Goodwill is assigned to the reporting unit

that benefits from the synergies arising from each business combination. Goodwill is not amortized. We perform

tests for impairment of goodwill annually, or more frequently if events or circumstances indicate it might be

impaired. Such tests include comparing the fair value of a reporting unit with its carrying value, including

goodwill. Impairment assessments are performed using a variety of methodologies, including cash flow analyses,

estimates of sales proceeds and independent appraisals. Where applicable, an appropriate discount rate is used,

based on the Company’s cost of capital rate or location-specific economic factors. Refer to Note 4.

Derivative Financial Instruments

Our Company accounts for derivative financial instruments in accordance with SFAS No. 133, ‘‘Accounting

for Derivative Instruments and Hedging Activities,’’ as amended by SFAS No. 137 and SFAS No. 138. SFAS

No. 133 was further amended by SFAS No. 149, ‘‘Amendment of Statement 133 on Derivative Instruments and

Hedging Activities.’’ Our Company recognizes all derivative instruments as either assets or liabilities at fair value

in our balance sheets. Refer to Note 10.

Retirement Related Benefits

Using appropriate actuarial methods and assumptions, our Company accounts for defined benefit pension

plans in accordance with SFAS No. 87, ‘‘Employers’ Accounting for Pensions.’’ We account for our nonpension

postretirement benefits in accordance with SFAS No. 106, ‘‘Employers’ Accounting for Postretirement Benefits

Other Than Pensions.’’ In 2003, we adopted SFAS No. 132 (revised 2003), ‘‘Employers’ Disclosures about

Pensions and Other Postretirement Benefits,’’ for all U.S. plans. As permitted by this standard, we will adopt the

disclosure provisions for all foreign plans for the year ending December 31, 2004. SFAS No. 132, as revised,

requires additional disclosures about assets, obligations, cash flows and net periodic benefit cost of defined

benefit pension plans and other postretirement benefit plans. This statement did not change the measurement

or recognition of those plans required by SFAS No. 87, SFAS No. 88, ‘‘Employers’ Accounting for Settlements

and Curtailments of Defined Benefit Pension Plans and for Termination Benefits,’’ or SFAS No. 106.

One of the principal assumptions used to calculate net periodic pension cost is the expected long-term rate

of return on plan assets. The expected long-term rate of return on plan assets may result in recognized returns

that are greater or less than the actual returns on those plan assets in any given year. Over time, however, the

expected long-term rate of return on plan assets is designed to approximate the actual long-term returns.

The discount rate assumptions used to account for pension and nonpension postretirement benefit plans

reflect the rates available on high-quality, fixed-income debt instruments on December 31 of each year. The rate

of compensation increase is another significant assumption used for pension accounting and is determined by

the Company based upon annual reviews.

For postretirement health care plan accounting, our Company reviews external data and our own historical

trends for health care costs to determine the health care cost trend rate assumptions.

Refer to Note 14.

60