Coca Cola 2003 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

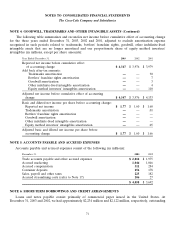

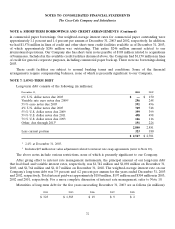

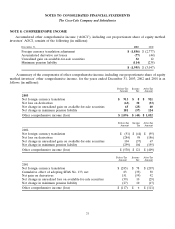

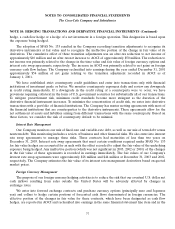

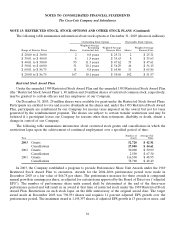

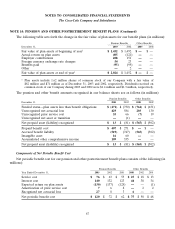

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 10: HEDGING TRANSACTIONS AND DERIVATIVE FINANCIAL INSTRUMENTS (Continued)

hedge, a cash flow hedge or a hedge of a net investment in a foreign operation. This designation is based upon

the exposure being hedged.

The adoption of SFAS No. 133 resulted in the Company recording transition adjustments to recognize its

derivative instruments at fair value and to recognize the ineffective portion of the change in fair value of its

derivatives. The cumulative effect of these transition adjustments was an after-tax reduction to net income of

approximately $10 million and an after-tax net increase to AOCI of approximately $50 million. The reduction to

net income was primarily related to the change in the time value and fair value of foreign currency options and

interest rate swap agreements, respectively. The increase in AOCI was primarily related to net gains on foreign

currency cash flow hedges. The Company reclassified into earnings during the year ended December 31, 2001

approximately $54 million of net gains relating to the transition adjustment recorded in AOCI as of

January 1, 2001.

We have established strict counterparty credit guidelines and enter into transactions only with financial

institutions of investment grade or better. We monitor counterparty exposures daily and review any downgrade

in credit rating immediately. If a downgrade in the credit rating of a counterparty were to occur, we have

provisions requiring collateral in the form of U.S. government securities for substantially all of our transactions.

To mitigate presettlement risk, minimum credit standards become more stringent as the duration of the

derivative financial instrument increases. To minimize the concentration of credit risk, we enter into derivative

transactions with a portfolio of financial institutions. The Company has master netting agreements with most of

the financial institutions that are counterparties to the derivative instruments. These agreements allow for the

net settlement of assets and liabilities arising from different transactions with the same counterparty. Based on

these factors, we consider the risk of counterparty default to be minimal.

Interest Rate Management

Our Company monitors our mix of fixed-rate and variable-rate debt, as well as our mix of term debt versus

nonterm debt. This monitoring includes a review of business and other financial risks. We also enter into interest

rate swap agreements to manage these risks. These contracts had maturities of less than two years on

December 31, 2003. Interest rate swap agreements that meet certain conditions required under SFAS No. 133

for fair value hedges are accounted for as such with the offset recorded to adjust the fair value of the underlying

exposure being hedged. Any ineffective portion (which was not significant in 2003, 2002 or 2001) of the changes

in the fair value of these agreements is recorded in earnings immediately. The fair values of our Company’s

interest rate swap agreements were approximately $28 million and $44 million at December 31, 2003 and 2002,

respectively. The Company estimates the fair value of its interest rate management derivatives based on quoted

market prices.

Foreign Currency Management

The purpose of our foreign currency hedging activities is to reduce the risk that our eventual U.S. dollar net

cash inflows resulting from sales outside the United States will be adversely affected by changes in

exchange rates.

We enter into forward exchange contracts and purchase currency options (principally euro and Japanese

yen) and collars to hedge certain portions of forecasted cash flows denominated in foreign currencies. The

effective portion of the changes in fair value for these contracts, which have been designated as cash flow

hedges, are reported in AOCI and reclassified into earnings in the same financial statement line item and in the

77