Coca Cola 2003 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

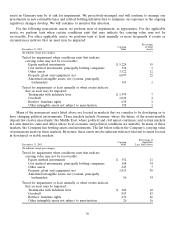

Equity Method and Cost Method Investments. For most publicly traded investments, the fair value of our

Company’s investment is often readily available based on quoted market prices. For non–publicly traded

investments, management’s assessment of fair value is based on valuation methodologies including discounted

cash flows, estimates of sales proceeds and external appraisals, as appropriate. The ability to accurately predict

future cash flows, especially in developing and unstable markets, may impact the determination of fair value.

In the event a decline in fair value of an investment occurs, management may be required to determine if

the decline in market value is other than temporary. Management’s assessments as to the nature of a decline in

fair value are based on the valuation methodologies discussed above and our ability and intent to hold the

investment. We consider our equity method investees to be strategic long-term investments; therefore, we

generally complete our assessments with a long-term viewpoint. If the fair value is less than the carrying value

and the decline in value is considered to be other than temporary, an appropriate write-down is recorded.

Management’s assessments of fair value in accordance with these valuation methodologies represent our best

estimates as of the time of the impairment review and are consistent with our internal planning. If different fair

values were estimated, this could have a material impact on the financial statements.

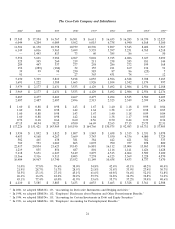

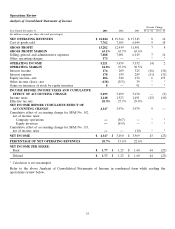

The following table presents the difference between calculated fair values, based on quoted closing prices of

publicly traded shares, and our Company’s carrying values for significant publicly traded bottlers accounted for

as equity method investees (in millions):

Fair Carrying

December 31, 2003 Value Value Difference1

Coca-Cola Enterprises Inc. $ 3,695 $ 1,260 $ 2,435

Coca-Cola FEMSA, S.A. de C.V. 1,568 674 894

Coca-Cola Hellenic Bottling Company S.A. 1,109 941 168

Coca-Cola Amatil Limited 1,083 652 431

Grupo Continental, S.A. 266 169 97

Coca-Cola Bottling Company Consolidated 131 61 70

Coca-Cola Embonor S.A. 126 135 (9)

Coca-Cola West Japan Company Ltd. 78 123 (45)

Embotelladoras Polar S.A. 38 41 (3)

$ 8,094 $ 4,056 $ 4,038

1In instances where carrying value exceeds fair value, the current decline in value is considered to be

temporary.

Other Assets. Our Company invests in infrastructure programs with our bottlers that are directed at

strengthening our bottling system and increasing unit case volume. Additionally, our Company advances

payments to certain customers to fund future marketing activities intended to generate profitable volume and

expenses such payments over the applicable period. Advance payments are also made to certain customers for

distribution rights. Payments under these programs are generally capitalized as other assets in our balance

sheets. Management periodically evaluates the recoverability of these assets by preparing estimates of sales

volume, the resulting gross profit, cash flows and other factors. If the assets are assessed to be recoverable, they

are amortized over the periods benefited. If the carrying value of these assets is considered to be not

recoverable, such assets are written down as appropriate.

Property, Plant and Equipment. Certain events or changes in circumstances may indicate that the

recoverability of the carrying amount of property, plant and equipment should be assessed. Such events or

changes may include a significant decrease in market value, a significant change in the business climate in a

particular market, or a current-period operating or cash flow loss combined with historical losses or projected

future losses. If an event occurs or changes in circumstances are present, we estimate the future cash flows

expected to result from the use of the asset and its eventual disposition. If the sum of the expected future cash

31