Coca Cola 2003 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

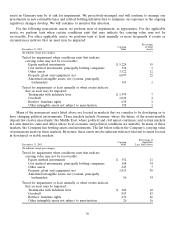

the Asia operating segment. This impact was partially offset by generally weaker currencies negatively impacting

our Latin America operating segment.

The acquisitions of our interests in Odwalla, Inc. (‘‘Odwalla’’), the CCDA water brands and CBC

(structural change) contributed significantly to the increased 2002 net operating revenues.

The most significant structural change in 2002 was the consolidation of CCEAG. This consolidation was

partially offset by the sale and resulting deconsolidation of our Russian and Baltics bottling operations.

The combined 2002 net operating revenues resulting from the structural change of CCEAG and the

acquisitions of our interests in Odwalla, CCDA and CBC were approximately $1.5 billion. The Russian and

Baltics bottling operations accounted for approximately $150 million of 2001 net operating revenues.

Price increases and product/geographic mix in selected countries positively impacted our 2002 net operating

revenues. The improvements in these core business factors reflected a positive trend in 2002.

The strength of the U.S. dollar in 2002 relative to most major currencies had a negative impact on net

operating revenues. The stronger U.S. dollar compared to the Japanese yen, the Argentine peso, the Mexican

peso, the Brazilian real, the Venezuelan bolivar and the South African rand was partially offset by strength in the

euro. Refer to MD&A heading ‘‘Exchange.’’

Information about our net operating revenues by operating segment on a percentage basis is as follows:

Year Ended December 31, 2003 2002 2001

North America 30.1% 32.0% 32.7%

Africa 3.9 3.5 3.6

Asia 24.0 25.8 27.7

Europe, Eurasia & Middle East 31.2 26.9 22.6

Latin America 9.7 10.7 12.4

Corporate 1.1 1.1 1.0

Net operating revenues 100.0% 100.0% 100.0%

The net operating revenues for Europe, Eurasia and Middle East significantly increased in 2003 due to

sound business fundamentals, innovation, strong marketing strategies, rigorous cost management, positive

currency trends and favorable weather during the summer months. The 2002 net operating revenues for Europe,

Eurasia and Middle East increased primarily due to the consolidation of CCEAG. Net operating revenues in

2002 for Latin America were negatively impacted by exchange fluctuations and challenging economic conditions,

primarily in Argentina, Venezuela and Brazil.

Gross Profit

The decrease in 2003 gross profit margin versus 2002 was primarily the result of the inclusion of higher-

revenue, lower-margin CCEAG, CCDA and Evian results for the full year of 2003. These results were partially

offset by the creation of the nationally integrated supply chain company in Japan (previously discussed under

MD&A heading ‘‘Net Operating Revenues’’), the deconsolidation of CBC during the second quarter of 2003

and the receipt during the first quarter of 2003 of a settlement of approximately $52 million from certain

defendants in a vitamin antitrust litigation. Refer to Note 16.

We currently estimate that the creation of the nationally integrated supply chain company in Japan, partially

offset by other structural changes such as consolidation of entities in accordance with Interpretation 46, will

improve the gross profit margin in 2004 compared to 2003. Refer to Note 1 for a discussion of Interpretation 46.

35