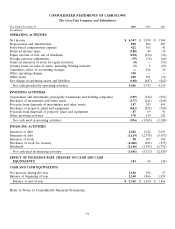

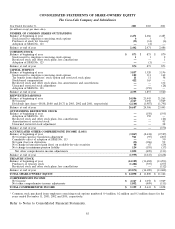

Coca Cola 2003 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

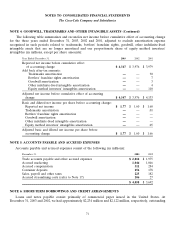

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 1: ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Contingencies

Our Company is involved in various legal proceedings and tax matters. Due to their nature, such legal

proceedings and tax matters involve inherent uncertainties including, but not limited to, court rulings,

negotiations between affected parties and governmental actions. Management assesses the probability of loss for

such contingencies and accrues a liability and/or discloses the relevant circumstances, as appropriate. Refer to

Note 11.

Business Combinations

In accordance with SFAS No. 141, ‘‘Business Combinations,’’ we account for all business combinations by

the purchase method. Furthermore, we recognize intangible assets apart from goodwill if they arise from

contractual or legal rights or if they are separable from goodwill.

New Accounting Standards

Effective January 1, 2003, the Company adopted SFAS No. 146, ‘‘Accounting for Costs Associated with Exit

or Disposal Activities.’’ SFAS No. 146 addresses financial accounting and reporting for costs associated with exit

or disposal activities and nullifies Emerging Issues Task Force (‘‘EITF’’) Issue No. 94-3, ‘‘Liability Recognition

for Certain Employee Termination Benefits and Other Costs to Exit an Activity (including Certain Costs

Incurred in a Restructuring).’’ SFAS No. 146 requires that a liability for a cost associated with an exit or disposal

plan be recognized when the liability is incurred. Under SFAS No. 146, an exit or disposal plan exists when the

following criteria are met:

• Management, having the authority to approve the action, commits to a plan of termination.

• The plan identifies the number of employees to be terminated, their job classifications or functions and

their locations, and the expected completion date.

• The plan establishes the terms of the benefit arrangement, including the benefits that employees will

receive upon termination (including but not limited to cash payments), in sufficient detail to enable

employees to determine the type and amount of benefits they will receive if they are involuntarily

terminated.

• Actions required to complete the plan indicate that it is unlikely that significant changes to the plan will

be made or that the plan will be withdrawn.

SFAS No. 146 establishes that fair value is the objective for initial measurement of the liability. In cases

where employees are required to render service beyond a minimum retention period until they are terminated in

order to receive termination benefits, a liability for termination benefits is recognized ratably over the future

service period. Under EITF Issue No. 94-3, a liability for the entire amount of the exit cost was recognized at the

date that the entity met the four criteria described above. Refer to Note 17.

Effective January 1, 2003, our Company adopted the recognition and measurement provisions of Financial

Accounting Standards Board (‘‘FASB’’) Interpretation No. 45 (‘‘Interpretation 45’’), ‘‘Guarantor’s Accounting

and Disclosure Requirements for Guarantees, Including Indirect Guarantees of Indebtedness of Others.’’ This

interpretation elaborates on the disclosures to be made by a guarantor in interim and annual financial

statements about the obligations under certain guarantees. Interpretation 45 also clarifies that a guarantor is

required to recognize, at the inception of a guarantee, a liability for the fair value of the obligation undertaken in

61