Coca Cola 2003 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2003 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

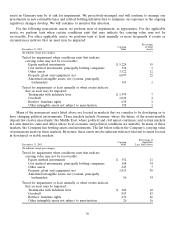

Our Company eliminates from our financial results all significant intercompany transactions, including the

intercompany portion of transactions with equity method investees.

Effective February 2002, our Company acquired control of Coca-Cola Erfrischungsgetraenke AG

(‘‘CCEAG’’), the largest bottler of the Company’s beverage products in Germany. Under our policy, we

concluded that CCEAG should be consolidated in our financial statements based on the following.

Prior to February 2002, our Company accounted for CCEAG under the equity method of accounting. Our

Company had an approximate 41 percent ownership interest in the outstanding shares of CCEAG. In

February 2002, in accordance with the terms of the Control and Profit and Loss Transfer Agreement (‘‘CPL’’),

our Company obtained control of CCEAG for a period of up to five years. Furthermore, we also entered into a

Pooling Agreement with certain share owners of CCEAG that provided our Company with voting control of

CCEAG. In return for control of CCEAG, the Company guaranteed annual payments, in lieu of dividends by

CCEAG, to all other CCEAG share owners. Additionally, all other CCEAG share owners entered into either a

put or a put/call option agreement with the Company, exercisable at any time up to the December 31, 2006

expiration date. Our Company entered into either put or put/call agreements for shares representing an

approximate 59 percent interest in CCEAG. The spread in the strike prices of the put and call options is only

approximately 3 percent.

Because the terms of the CPL transferred control and all the economic risks and rewards of CCEAG to the

Company immediately, we determined consolidation was appropriate. Refer to Note 18.

In December 2003, the Financial Accounting Standards Board (‘‘FASB’’) issued FASB Interpretation

No. 46 (revised December 2003) (‘‘Interpretation 46’’), ‘‘Consolidation of Variable Interest Entities.’’ We do not

anticipate that Interpretation 46 will have a material impact on our basis of presentation and consolidation.

Refer to Note 1.

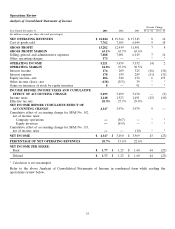

Recoverability of Noncurrent Assets

Management’s assessment of the recoverability of noncurrent assets involves critical accounting estimates.

The assessments reflect management’s best assumptions and estimates. Factors that management must estimate

when performing impairment tests include, among other items, sales volume, prices, inflation, discount rates,

marketing spending, exchange rates, tax rates and capital spending. These factors are interdependent and

therefore do not change in isolation. Significant management judgment is involved in estimating these factors,

and they include inherent uncertainties; however, the assumptions we use are consistent with our internal

planning. Management periodically evaluates and updates the estimates based on the conditions that influence

these factors. The variability of these factors depends on a number of conditions, including uncertainty about

future events, and thus our accounting estimates may change from period to period. If other assumptions and

estimates had been used in the current period, the balances for noncurrent assets could have been materially

impacted. Furthermore, if management uses different assumptions or if different conditions occur in future

periods, future operating results could be materially impacted.

Operating in more than 200 countries subjects our Company to many uncertainties and risks related to

various economic, political and regulatory environments. Refer to MD&A heading ‘‘Our Business—

Opportunities, Challenges and Risks.’’ As a result, many assumptions must be made by management when

determining the recoverability of noncurrent assets. An example of one uncertainty relates to the deposit law on

certain nonreturnable beverage packages enacted by the German government in the first quarter of 2003. The

change in law on January 1, 2003 and subsequent developments resulted in most retailers delisting

nonreturnable packages. After an initial decrease in volume growth, our management acted quickly to address

this matter and, as a result, our business posted sequential quarterly improvements. The new deposit law has

created a difficult environment for the industry, but we believe our management successfully positioned our

Company to respond to German consumers’ increasing preference for returnable packaging. However, if other

unexpected political matters or abrupt market shifts occur that impact our industry or our Company, certain

29