Coca Cola 2004 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2004 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

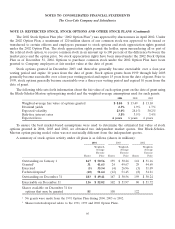

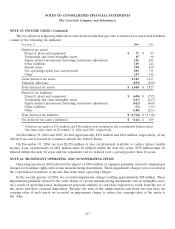

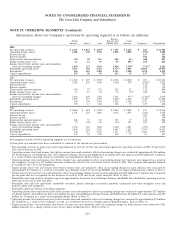

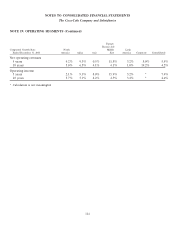

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 15: INCOME TAXES (Continued)

A reconciliation of the statutory U.S. federal rate and effective rates is as follows:

Year Ended December 31, 2004 2003 2002

Statutory U.S. federal rate 35.0 % 35.0 % 35.0 %

State income taxes—net of federal benefit 1.0 0.9 0.9

Earnings in jurisdictions taxed at rates different from the statutory

U.S. federal rate (9.4)1,2 (10.6)7(6.0)

Equity income or loss (3.1)3,4 (2.4)8(2.0)10

Other operating charges (0.9)5(1.1)9—

Write-down/sale of certain bottling investments —— 0.7 11

Other—net (0.5)6(0.9) (0.9)

Effective rates 22.1 % 20.9 % 27.7 %

1Includes approximately $92 million (or 1.4 percent) tax benefit related to the favorable resolution of

various tax issues and settlements.

2Includes tax charge of approximately $75 million (or 1.2 percent) related to recording of valuation

allowance on various deferred tax assets recorded in Germany.

3Includes approximately $50 million (or 0.8 percent) tax benefit related to the realization of certain

foreign tax credits per provisions of the Jobs Creation Act.

4Includes approximately $13 million (or 0.1 percent) tax charge on our proportionate share of the

favorable tax settlement related to Coca-Cola FEMSA.

5Primarily related to impairment of franchise rights at CCEAG and certain manufacturing investments.

Refer to Note 16.

6Includes approximately $36 million (or 0.6 percent) tax benefit related to the favorable resolution of

various tax issues and settlements.

7Includes approximately $50 million (or 0.8 percent) tax benefit for the release of tax reserves due

primarily to the resolution of various tax matters.

8Includes the tax effect of the write-down of certain intangible assets held by bottling investments in

Latin America. Refer to Note 2.

9Includes the tax effect of the charges for streamlining initiatives. Refer to Note 17.

10 Includes the tax effect of the charges by equity investees in 2002. Refer to Note 16.

11 Includes gains on the sale of Cervejarias Kaiser Brazil, Ltda and the write-down of certain bottling

investments, primarily in Latin America. Refer to Note 16.

Our effective tax rate reflects the tax benefits from having significant operations outside the United States

that are taxed at rates lower than the statutory U.S. rate of 35 percent. In 2003, our effective tax rate reflects

further benefit from realization of tax benefits on charges related to streamlining initiatives recorded in locations

with tax rates higher than our effective tax rate.

In 2003, management concluded that it was more likely than not that tax benefits would not be realized on

Coca-Cola FEMSA’s write-down of intangible assets in Latin America in connection with its merger with

Panamco. Refer to Note 2. In 2002, management concluded that it was more likely than not that tax benefits

would not be realized with respect to principally all of the items disclosed in Note 16. Accordingly, valuation

105