Coca Cola 2004 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2004 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

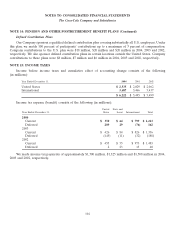

NOTE 15: INCOME TAXES (Continued)

allowances were recorded to offset the future tax benefit of these items, resulting in an increase in our effective

tax rate.

Undistributed earnings of the Company’s foreign subsidiaries amounted to approximately $9.8 billion at

December 31, 2004. Those earnings are considered to be indefinitely reinvested and, accordingly, no U.S.

federal and state income taxes have been provided thereon. Upon distribution of those earnings in the form of

dividends or otherwise, the Company would be subject to both U.S. income taxes (subject to an adjustment for

foreign tax credits) and withholding taxes payable to the various foreign countries. Determination of the amount

of unrecognized deferred U.S. income tax liability is not practical because of the complexities associated with its

hypothetical calculation; however, unrecognized foreign tax credits would be available to reduce a portion of the

U.S. liability.

As discussed in Note 1, the Jobs Creation Act was enacted in October 2004. One of the provisions provides

a one time benefit related to foreign tax credits generated by equity investments in prior years. The Company

recorded an income tax benefit of approximately $50 million as a result of this law change in 2004. The Jobs

Creation Act also includes a temporary incentive for U.S. multinationals to repatriate foreign earnings at an

effective 5.25 percent tax rate. As of December 31, 2004, management had not decided whether, and to what

extent, we might repatriate foreign earnings under the Jobs Creation Act, and accordingly, the consolidated

financial statements do not reflect any provision for taxes on the unremitted foreign earnings that might be

remitted under the Jobs Creation Act. Based on our analysis to date, however, it is reasonably possible that we

may repatriate some amount between $0 and $6.1 billion, with the respective tax liability ranging from $0 to

$400 million. We expect to be in a position to finalize our assessment by December 31, 2005.

106