Coca Cola 2004 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2004 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

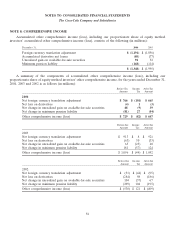

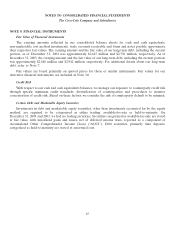

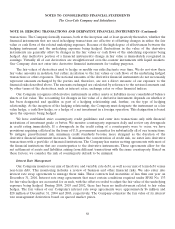

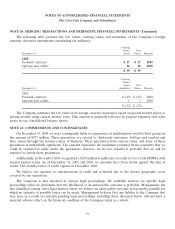

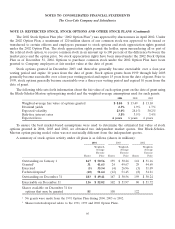

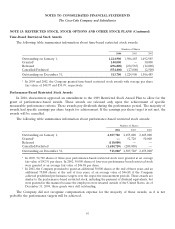

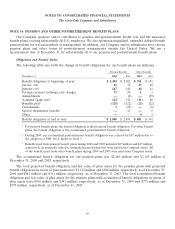

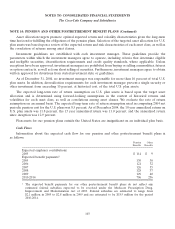

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 11: COMMITMENTS AND CONTINGENCIES (Continued)

from third parties, as well as certain additional comments from the Commission’s legal staff. The Company is in

the process of addressing these comments with the Commission. The Company anticipates that the formal

Undertaking will form the basis of a Commission decision pursuant to Article 9, paragraph 1 of Council

Regulation 1/2003 to be issued in the second quarter of 2005, bringing an end to the investigation. The

submission of the Undertaking does not imply any recognition on the Company’s or the bottlers’ part of any

infringement of Commission competition rules. We believe that the Undertaking, while imposing restrictions,

clarifies the application of competition rules to our practices in Europe and will allow our system to be able to

compete vigorously while adhering to the Undertaking’s provisions.

The Company is also discussing with the Commission issues relating to parallel trade within the European

Union arising out of comments received by the Commission from third parties. The Company is fully

cooperating with the Commission and is providing information on these issues and the measures taken and to be

taken to address any issues raised. The Company is unable to predict at this time with any reasonable degree of

certainty what action, if any, the Commission will take with respect to these issues.

The Spanish competition service made unannounced visits to our offices and those of certain bottlers in

Spain in 2000. In December 2003, the Spanish competition service suspended its investigation until the

Commission notifies the service of how the Commission will proceed in its aforementioned investigation.

The French Competition Directorate has also initiated an inquiry into commercial practices related to the

soft drink sector in France. This inquiry has been conducted through visits to the offices of the Company;

however, no conclusions have been communicated to the Company by the Directorate.

At the time of divesting our interest in a consolidated entity, we sometimes agree to indemnify the buyer for

specific liabilities related to the period we owned the entity. Management believes that any liability to the

Company that may arise as a result of any such indemnification agreements will not have a material adverse

effect on the financial condition of the Company taken as a whole.

The Company is involved in various tax matters. We establish reserves at the time that we determine that it

is probable that we will be liable to pay additional taxes related to certain matters. We adjust these reserves,

including any impact on the related interest and penalties, in light of changing facts and circumstances, such as

the progress of a tax audit.

A number of years may elapse before a particular matter, for which we may have established a reserve, is

audited and finally resolved or when a tax assessment is raised. The number of years with open tax audits varies

depending on the tax jurisdiction. While it is often difficult to predict the final outcome or the timing of

resolution of any particular tax matter, we record a reserve when we determine the likelihood of loss is probable

and the amount of loss is reasonably estimable. Such liabilities are recorded in the line item accrued income

taxes in the Company’s consolidated balance sheets. Favorable resolution of tax matters that had been previously

reserved would be recognized as a reduction to our income tax expense, when known.

The Company is also involved in various tax matters where we have determined that the probability of an

unfavorable outcome is reasonably possible. Management believes that any liability to the Company that may

arise as a result of currently pending tax matters will not have a material adverse effect on the financial condition

of the Company taken as a whole.

The Company is a party to various legal proceedings in which we are seeking to be reimbursed for costs that

we have incurred in the past. Although none of these reimbursements has been realized at this time, the

93