Coca Cola 2004 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2004 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

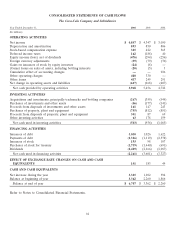

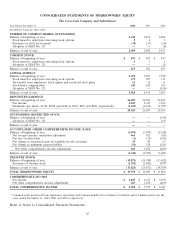

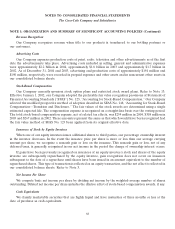

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Coca-Cola Company and Subsidiaries

NOTE 1: ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

2005. Our proportionate share of the stock-based compensation expense resulting from the adoption of SFAS

No. 123(R) by our equity investees will be recognized as a reduction to equity income.

In December 2004, the FASB issued SFAS No. 153, ‘‘Exchanges of Nonmonetary Assets, an amendment of

APB Opinion No. 29.’’ SFAS No. 153 is based on the principle that exchanges of nonmonetary assets should be

measured based on the fair value of the assets exchanged. APB Opinion No. 29, ‘‘Accounting for Nonmonetary

Transactions,’’ provided an exception to its basic measurement principle (fair value) for exchanges of similar

productive assets. Under APB Opinion No. 29, an exchange of a productive asset for a similar productive asset

was based on the recorded amount of the asset relinquished. SFAS No. 153 eliminates this exception and

replaces it with an exception of exchanges of nonmonetary assets that do not have commercial substance. SFAS

No. 153 is effective for our Company as of July 1, 2005. The Company will apply the requirements of SFAS

No. 153 prospectively.

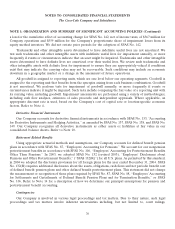

NOTE 2: BOTTLING INVESTMENTS

Coca-Cola Enterprises Inc.

Coca-Cola Enterprises Inc. (‘‘CCE’’) is a marketer, producer and distributor of bottle and can nonalcoholic

beverages, operating in eight countries. On December 31, 2004, our Company owned approximately 36 percent

of the outstanding common stock of CCE. We account for our investment by the equity method of accounting

and, therefore, our operating results include our proportionate share of income (loss) resulting from our

investment in CCE. As of December 31, 2004, our proportionate share of the net assets of CCE exceeded our

investment by approximately $366 million. This difference is not amortized.

73