McDonalds 2008 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2008 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

fund capital expenditures and debt repayments as well as return

cash to shareholders.

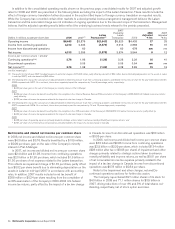

In 2008, capital expenditures of $2.1 billion were primarily

used to open 995 restaurants (590 net, after 405 closings) and

reimage 1,450 locations. In addition, we believe strongly in return-

ing cash to shareholders via dividends and share repurchases. In

2008, we returned $5.8 billion to shareholders, consisting of

$1.8 billion in dividends and $4.0 billion in share repurchases. This

brings total cash returned to $11.5 billion under our 2007-2009

$15 billion to $17 billion target. We are confident we will achieve

this cash return target given the ongoing strength and stability of

cash from operations and our continued evolution toward a more

heavily franchised, less capital-intensive business model.

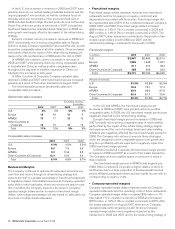

We believe locally-owned and operated restaurants are at the

core of our competitive advantage, making us not just a global

brand but also a locally relevant one. In addition, an optimized mix

of franchised and Company-operated restaurants helps to max-

imize brand performance and further enhance the reliability of our

cash flow and returns. To that end, in August 2007, the Company

completed the sale of its businesses in Brazil, Argentina, Mexico,

Puerto Rico, Venezuela and 13 other countries in Latin America

and the Caribbean, which totaled 1,571 restaurants, to a devel-

opmental licensee organization. Under the new ownership

structure, the Company receives royalties in these markets instead

of a combination of Company-operated sales and franchised rents

and royalties.

In addition, in 2007 we set a three-year target to refranchise

1,000 to 1,500 existing Company-operated restaurants between

2008 and 2010, primarily in our major markets. In 2008, we

refranchised about 675 restaurants, increasing the percent of

franchised restaurants worldwide to 80% from 78% at year-end

2007. This transition to a greater percentage of franchised restau-

rants is expected to affect consolidated financial statements as

follows:

• A negative impact on consolidated revenues as Company-

operated sales shift to franchised sales where we receive rent

and/or royalties, along with initial fees.

• A decrease in Company-operated margin dollars and an

increase in franchised margin dollars, while margin percentages

will vary based on sales and cost structures of refranchised res-

taurants.

• Fluctuations in Other Operating (Income) Expense due to gains

and/or losses resulting from sales of restaurants.

• An increase in combined operating margin percent.

• An increase in return on average assets due primarily to a

decrease in average asset balances.

Highlights from the year included:

• Comparable sales grew 6.9% and guest counts rose 3.1%, build-

ing on 2007 increases of 6.8% and 3.8%, respectively.

• Systemwide sales increased 11% (9% in constant currencies).

• Company-operated margins improved to 17.6% and franchised

margins improved to 82.3%.

• Net income per share from continuing operations was $3.76, an

increase of 16% after adjusting for the impact of the 2007 Latin

America transaction.

• Cash provided by operations totaled $5.9 billion and capital

expenditures totaled $2.1 billion.

• Returned $5.8 billion to shareholders through shares

repurchased and dividends paid, including a 33% increase in the

quarterly cash dividend to $0.50 per share for the fourth quarter

– bringing our current annual dividend rate to $2.00 per share.

• One-year ROIIC was 38.9% and three-year ROIIC was 37.5%

for 2008.

Outlook for 2009

We will continue to drive success in 2009 and beyond by remain-

ing focused on being better, not just bigger. We will do so by

further enhancing our understanding of consumers’ needs and

wants; facilitating greater sharing and adoption of best practices

and new ideas worldwide; and leveraging a strategic approach to

implementing initiatives to drive the best bottom-line impact.

Despite challenging economic conditions, the McDonald’s

System is energized by our current worldwide momentum. We will

continue to build on our strength in five key areas: maintaining the

balance between price and value; maximizing the benefit of avail-

able capital by improving the relevance and contemporary feel of

our existing restaurants; leveraging the equity and unique tastes of

core menu favorites like the Big Mac, the Quarter Pounder with

Cheese and our world-famous French Fries; continuing our finan-

cial discipline and evaluation of success measures to ensure these

measures are driving actions that positively impact our restaurants;

and furthering operations excellence by focusing on improved

execution. As we do so, we are confident we can meet or exceed

the long-term constant currency financial targets previously dis-

cussed.

In the U.S., our 2009 focus is to continue to build relevance

and loyalty by staying connected to customers’ needs for menu

variety and beverage choice, everyday affordability and con-

venience. Our initiatives will include reminding customers of the

enduring appeal of menu classics such as the Big Mac and

encouraging trial of new sandwich and beverage options including

specialty coffees. Also in 2009, we will continue to offer value

across our menu from the Dollar Menu to our premium products,

as well as our classic menu favorites and mid-tier offerings such as

our Double Cheeseburger and Snack Wraps. These initiatives

combined with the convenience of our locations, optimized drive-

thru service, cashless transactions and longer operating hours will

reinforce McDonald’s position as our customers’ preferred place

and way to eat.

Our priorities in Europe remain upgrading the customer and

employee experience, enhancing local relevance and building

brand transparency. In 2009, we will continue upgrading our

restaurants’ ambiance through reimaging, including adding another

200 McCafes primarily in Germany and France. In addition, we will

focus on optimizing our drive-thru service, completing the con-

version of our kitchen operating system in most European

restaurants and increasing total locations offering extended and

24-hour service. We also will strengthen our local relevance by

complementing our tiered menu with new products and a relevant

variety of limited-time food events featuring beef, chicken, desserts

and coffee selections. In the area of brand transparency, we will

remain open and accessible and will continue to inform consumers

about our food quality and reputation as an employer.

In APMEA, our goal is to be consumers’ first choice when eating

out. To achieve this goal, locally-relevant strategies surrounding

convenience, breakfast and branded affordability are essential in

this diverse and dynamic part of the world. Convenience initiatives

include leveraging the success of 24-hour or extended operating

hours, offering delivery service and building our drive-thru

McDonald’s Corporation Annual Report 2008 23