McDonalds 2008 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2008 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

adopted retrospectively. We do not expect the adoption of SFAS

No. 160 to have a significant impact on our consolidated financial

statements.

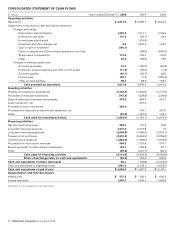

CASH FLOWS

The Company generates significant cash from its operations and

has substantial credit availability and capacity to fund operating

and discretionary spending such as capital expenditures, debt

repayments, dividends and share repurchases.

Cash provided by operations totaled $5.9 billion and exceeded

capital expenditures by $3.8 billion in 2008, while cash provided

by operations totaled $4.9 billion and exceeded capital

expenditures by $2.9 billion in 2007. In 2008, cash provided by

operations increased $1.0 billion or 21% compared to 2007 pri-

marily due to increased operating results and changes in working

capital, partly due to lower income tax payments and the receipt of

$143 million related to an IRS examination completed in 2007. In

2007, cash provided by operations increased $535 million com-

pared to 2006 primarily due to increased operating results and

lower income tax payments.

Cash used for investing activities totaled $1.6 billion in 2008,

an increase of $475 million compared with 2007. Proceeds from

certain asset sales were lower in 2008 (Pret A Manger) than 2007

(Latam and Boston Market). In addition, capital expenditures

increased $189 million in 2008, primarily driven by increases in

Europe and APMEA, partly offset by the elimination of capital

expenditures as a result of the Latam transaction. The increase in

cash used for investing activities was partly offset by higher pro-

ceeds from the sales of restaurant businesses and property and

lower expenditures on purchases of restaurant businesses in con-

junction with our overall refranchising strategy. Cash used for

investing activities totaled $1.2 billion in 2007, a decrease of

$124 million compared with 2006, primarily due to net proceeds

received from the Latam transaction and the sale of Boston Mar-

ket in 2007, partly offset by higher capital expenditures.

Cash used for financing activities totaled $4.1 billion in 2008,

an increase of $118 million compared with 2007. Financing activ-

ities in 2008 reflected lower proceeds from stock option exercises,

mostly offset by higher net debt issuances. In 2007, cash used for

financing activities totaled $4.0 billion, a decrease of $1.5 billion

compared to 2006, primarily due to higher net debt issuances,

partly offset by higher treasury stock purchases and an increase in

the common stock dividend.

As a result of the above activity, the Company’s cash and equiv-

alents balance increased $82 million in 2008 to $2.1 billion,

compared with a decrease of $147 million in 2007. In addition to

cash and equivalents on hand and cash provided by operations, the

Company can meet short-term funding needs through its con-

tinued access to commercial paper borrowings and line of credit

agreements.

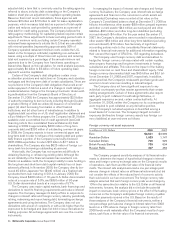

Restaurant development and capital expenditures

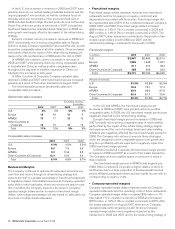

In 2008, the Company opened 918 traditional restaurants and 77

satellite restaurants (small, limited-menu restaurants for which the

land and building are generally leased), and closed 209 traditional

restaurants and 196 satellite restaurants. In 2007, the Company

opened 743 traditional restaurants and 93 satellite restaurants,

and closed 240 traditional restaurants and 265 satellite restau-

rants. About 60% of restaurant openings and more than 75% of

restaurant closings occurred in the major markets in both years.

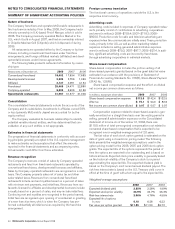

Systemwide restaurants at year end(1)

2008 2007 2006

U.S. 13,918 13,862 13,774

Europe 6,628 6,480 6,403

APMEA 8,255 7,938 7,822

Other Countries & Corporate 3,166 3,097 3,047

Total 31,967 31,377 31,046

(1) Includes satellite units at December 31, 2008, 2007 and 2006 as follows: U.S.–

1,169, 1,233, 1,254; Europe–226, 214, 201; APMEA (primarily Japan)–1,379,

1,454, 1,640; Other Countries & Corporate–447, 439, 417.

In 2009, the Company expects to open about 950 traditional

restaurants and 50 satellite restaurants and close about 200 tradi-

tional restaurants and 150 satellite restaurants. About 60% of total

openings and 70% of total closings will be in major markets.

Approximately 65% of Company-operated restaurants and

about 80% of franchised restaurants were located in the major

markets at the end of 2008. Franchisees operated 80% of the

restaurants at year-end 2008.

Capital expenditures increased $189 million or 10% in 2008

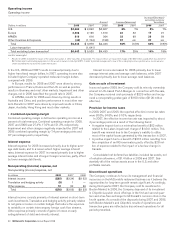

and $205 million or 12% in 2007. The increases in capital

expenditures in both years were primarily due to higher investment

in new restaurants — in Europe and APMEA in 2008 and in

Europe and the U.S. in 2007. Capital expenditures reflected the

Company’s commitment to growing sales at existing restaurants,

including reinvestment initiatives such as reimaging in many mar-

kets around the world in both years and the Combined Beverage

Business in the U.S. in 2008. Capital expenditures related to dis-

continued operations were $10 million and $82 million in 2007

and 2006, respectively. The expenditures in 2007 primarily related

to investment in existing Boston Market restaurants and

expenditures in 2006 primarily related to new Chipotle restaurants.

Capital expenditures invested in major markets, excluding

Japan, represented over 70% of the total in 2008, 2007 and

2006. Japan is accounted for under the equity method, and

accordingly its capital expenditures are not included in con-

solidated amounts.

Capital expenditures

In millions 2008 2007 2006

New restaurants $ 897 $ 687 $ 530

Existing restaurants 1,152 1,158 1,075

Other(1) 87 102 137

Total capital expenditures $ 2,136 $ 1,947 $ 1,742

Total assets $28,462 $29,392 $28,974

(1) Primarily corporate equipment and other office related expenditures.

New restaurant investments in all years were concentrated in

markets with acceptable returns or opportunities for long-term

growth. Average development costs vary widely by market depend-

ing on the types of restaurants built and the real estate and

construction costs within each market. These costs, which include

land, buildings and equipment, are managed through the use of

optimally sized restaurants, construction and design efficiencies

and leveraging best practices. In addition, foreign currency fluctua-

tions affect average development costs. Although the Company is

not responsible for all costs for every restaurant opened, total

development costs (consisting of land, buildings and equipment)

for new traditional McDonald’s restaurants in the U.S. averaged

approximately $2.6 million in 2008.

34 McDonald’s Corporation Annual Report 2008