McDonalds 2008 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2008 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

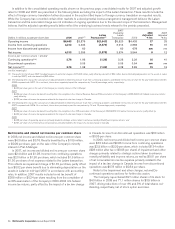

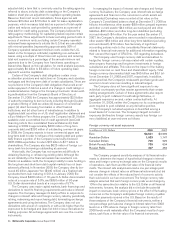

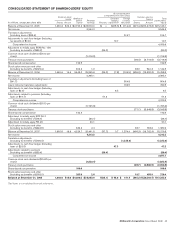

In connection with the Company’s sale of its investment in

Boston Market in August 2007, the Company received proceeds

of approximately $250 million and recorded a gain of $69 million

after tax. In addition, Boston Market’s net income (loss) for 2007

and 2006 was ($9) million and $7 million, respectively.

In first quarter 2006, Chipotle completed an IPO of 6.1 million

shares resulting in a tax-free gain to McDonald’s of $32 million to

reflect an increase in the carrying value of the Company’s invest-

ment as a result of Chipotle selling shares in the public offering.

Concurrent with the IPO, McDonald’s sold 3.0 million Chipotle

shares, resulting in net proceeds to the Company of $61 million

and an additional gain of $14 million after tax. In second quarter

2006, McDonald’s sold an additional 4.5 million Chipotle shares,

resulting in net proceeds to the Company of $267 million and a

gain of $128 million after tax, while still retaining majority owner-

ship. In fourth quarter 2006, the Company completely separated

from Chipotle through a noncash, tax-free exchange of its remain-

ing Chipotle shares for its common stock. McDonald’s accepted

18.6 million shares of its common stock in exchange for the

16.5 million shares of Chipotle class B common stock held by

McDonald’s and recorded a tax-free gain of $480 million.

Chipotle’s net income for 2006 was $18 million.

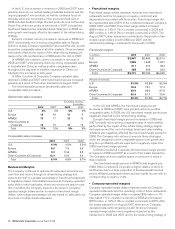

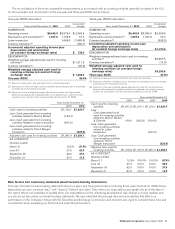

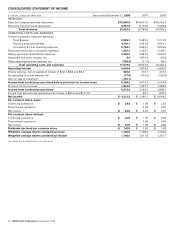

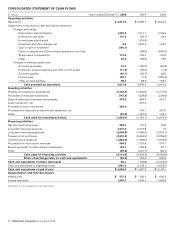

Accounting changes

• SFAS Statement No. 158

In 2006, the Financial Accounting Standards Board (FASB) issued

Statement of Financial Accounting Standards No. 158, Employers’

Accounting for Defined Benefit Pension and Other Postretirement

Plans,an amendment of FASB Statements No. 87, 88, 106 and

132(R) (SFAS No. 158). SFAS No. 158 requires the Company to

recognize the overfunded or underfunded status of a defined

benefit postretirement plan as an asset or liability on the Con-

solidated balance sheet and to recognize changes in that funded

status in the year changes occur through accumulated other

comprehensive income. The Company adopted the applicable

provisions of SFAS No. 158 effective December 31, 2006, as

required. This resulted in a net decrease to accumulated other

comprehensive income of $89 million, for a limited number of

applicable international markets.

• EITF Issue 06-2

In 2006, the FASB ratified Emerging Issues Task Force (EITF)

Issue 06-2, Accounting for Sabbatical Leave and Other Similar

Benefits Pursuant to FASB Statement No. 43, Accounting for

Compensated Absences (EITF 06-2). Under EITF 06-2,

compensation costs associated with a sabbatical should be

accrued over the requisite service period, assuming certain con-

ditions are met. Previously, the Company expensed sabbatical

costs as incurred. The Company adopted EITF 06-2 effective

January 1, 2007, as required and accordingly, recorded a $36 mil-

lion cumulative adjustment, net of tax, to decrease the

January 1, 2007 balance of retained earnings. The annual impact

to earnings is not significant.

• FASB Interpretation No. 48

In 2006, the FASB issued Interpretation No. 48, Accounting for

Uncertainty in Income Taxes (FIN 48), which is an interpretation of

FASB Statement No. 109, Accounting for Income Taxes. FIN 48

clarifies the accounting for income taxes by prescribing the mini-

mum recognition threshold a tax position is required to meet

before being recognized in the financial statements. FIN 48 also

provides guidance on derecognition, measurement, classification,

interest and penalties, accounting in interim periods, disclosure and

transition. The Company adopted the provisions of FIN 48 effec-

tive January 1, 2007, as required. As a result of the

implementation of FIN 48, the Company recorded a $20 million

cumulative adjustment to increase the January 1, 2007 balance of

retained earnings. FIN 48 requires that a liability associated with

an unrecognized tax benefit be classified as a long-term liability

except for the amount for which cash payment is anticipated within

one year. Upon adoption of FIN 48, $339 million of tax liabilities,

net of deposits, were reclassified from current to long-term and

included in other long-term liabilities.

• SFAS Statement No. 157

In 2006, the FASB issued Statement of Financial Accounting Stan-

dards No. 157, Fair Value Measurements (SFAS No. 157). SFAS

No. 157 defines fair value, establishes a framework for measuring

fair value, and expands disclosures about fair value measurements.

This statement does not require any new fair value measurements;

rather, it applies to other accounting pronouncements that require

or permit fair value measurements. The provisions of SFAS

No. 157, as issued, were effective January 1, 2008. However, in

February 2008, the FASB issued FASB Staff Position No. FAS

157-2, Effective Date of FASB Statement No. 157, which allows

entities to defer the effective date of SFAS No. 157, for one year,

for certain non-financial assets and non-financial liabilities, except

those that are recognized or disclosed at fair value in the financial

statements on a recurring basis (i.e., at least annually). The Com-

pany adopted SFAS No. 157 as of January 1, 2008 and elected

the deferral for non-financial assets and liabilities. The effect of

adopting this standard was not significant, and we do not expect

the January 1, 2009 adoption of SFAS No. 157 for non-financial

assets and liabilities to have a significant impact on our con-

solidated financial statements.

• SFAS Statement No. 141(R)

In 2007, the FASB issued Statement of Financial Accounting

Standards No. 141(R), Business Combinations (SFAS No. 141(R)).

SFAS No. 141(R) requires the acquiring entity in a business

combination to record all assets acquired and liabilities assumed at

their respective acquisition-date fair values, changes the recog-

nition of assets acquired and liabilities assumed arising from

preacquisition contingencies, and requires the expensing of

acquisition-related costs as incurred. SFAS No. 141(R) applies

prospectively to business combinations for which the acquisition

date is on or after January 1, 2009. We do not expect the adoption

of SFAS No. 141(R) to have a significant impact on our con-

solidated financial statements.

• SFAS Statement No. 160

In 2007, the FASB issued Statement of Financial Accounting

Standards No. 160, Noncontrolling Interests in Consolidated Finan-

cial Statements (an amendment of Accounting Research Bulletin

No. 51 (ARB 51)) (SFAS No. 160). SFAS No. 160 amends ARB

51 to establish accounting and reporting standards for the non-

controlling interest in a subsidiary and for the deconsolidation of a

subsidiary. SFAS No. 160 becomes effective beginning

January 1, 2009 and is required to be adopted prospectively,

except for the reclassification of noncontrolling interests to equity

and the recasting of net income (loss) attributable to both the con-

trolling and noncontrolling interests, which are required to be

McDonald’s Corporation Annual Report 2008 33