McDonalds 2008 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2008 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

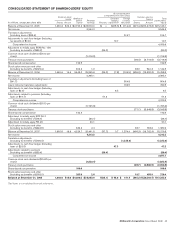

|

|

adjusted debt, a term that is commonly used by the rating agencies

referred to above, includes debt outstanding on the Company’s

balance sheet plus an adjustment to capitalize operating leases.

Based on their most recent calculations, these agencies add

between $6 billion and $12 billion to debt for lease capitalization

purposes, which increases total debt as a percent of total capital-

ization and reduces cash provided by operations as a percent of

total debt for credit rating purposes. The Company believes the

rating agency methodology for capitalizing leases requires certain

adjustments. These adjustments include: excluding percent rents in

excess of minimum rents; excluding certain Company-operated

restaurant lease agreements outside the U.S. that are cancelable

with minimal penalties (representing approximately 30% of

Company-operated restaurant minimum rents outside the U.S.,

based on the Company’s estimate); capitalizing non-restaurant

leases using a multiple of three times rent expense; and reducing

total rent expense by a percentage of the annual minimum rent

payments due to the Company from franchisees operating on

leased sites. Based on this calculation, for credit analysis purposes,

approximately $4 billion to $5 billion of future operating lease

payments would be capitalized.

Certain of the Company’s debt obligations contain cross-

acceleration provisions and restrictions on Company and subsidiary

mortgages and the long-term debt of certain subsidiaries. There are

no provisions in the Company’s debt obligations that would accel-

erate repayment of debt as a result of a change in credit ratings or

a material adverse change in the Company’s business. Under exist-

ing authorization from the Company’s Board of Directors, at

December 31, 2008, the Company has approximately $2.3 billion

of authority remaining to borrow funds, including through (i) public

or private offering of debt securities; (ii) issuance of commercial

paper; (iii) direct borrowing from banks or other financial

institutions; and (iv) other forms of indebtedness. In addition to

registered debt securities on a U.S. shelf registration statement and

a Euro Medium-Term Notes program, the Company has $1.3 billion

available under a committed line of credit agreement (see Debt

financing note to the consolidated financial statements). Debt

maturing in 2009 is approximately $400 million of long-term

corporate debt and $230 million of outstanding commercial paper.

In 2009, the Company expects to issue commercial paper and

long-term debt in order to refinance this maturing debt and poten-

tially finance a portion of the Company’s previously disclosed

2007-2009 expectation to return $15 billion to $17 billion to

shareholders. The Company also has $625 million of foreign cur-

rency bank line borrowings outstanding at year-end.

Historically, the Company has not experienced difficulty in

obtaining financing or refinancing existing debt. Although the

recent instability in the financial markets has resulted in con-

straints on available credit, the Company’s ability to raise funding in

the long-term and short-term debt capital markets has not been

adversely affected. In November 2008, the Company directly bor-

rowed 40 billion Japanese Yen ($440 million) via a floating-rate

syndicated term loan maturing in 2014. In January 2009, the

Company issued $400 million of 10-year U.S. Dollar-denominated

notes at a coupon rate of 5.0%, and $350 million of 30-year

U.S. Dollar-denominated bonds at a coupon rate of 5.7%.

The Company uses major capital markets, bank financings and

derivatives to meet its financing requirements and reduce interest

expense. The Company manages its debt portfolio in response to

changes in interest rates and foreign currency rates by periodically

retiring, redeeming and repurchasing debt, terminating exchange

agreements and using derivatives. The Company does not use

derivatives with a level of complexity or with a risk higher than the

exposures to be hedged and does not hold or issue derivatives for

trading purposes. All exchange agreements are over-the-counter

instruments.

In managing the impact of interest rate changes and foreign

currency fluctuations, the Company uses interest rate exchange

agreements and finances in the currencies in which assets are

denominated. Derivatives were recorded at fair value on the

Company’s Consolidated balance sheet at December 31, 2008 as

follows: miscellaneous other assets–$88 million; prepaid expenses

and other current assets–$44 million; accrued payroll and other

liabilities–$22 million; and other long-term liabilities (excluding

accrued interest)–$4 million. For the year ended December 31,

2007, the Company’s derivatives were recorded in miscellaneous

other assets–$64 million and other long-term liabilities (excluding

accrued interest)–$70 million. See Summary of significant

accounting policies note to the consolidated financial statements

related to financial instruments for additional information regarding

their use and the impact of SFAS No. 133 regarding derivatives.

The Company uses foreign currency debt and derivatives to

hedge the foreign currency risk associated with certain royalties,

intercompany financings and long-term investments in foreign

subsidiaries and affiliates. This reduces the impact of fluctuating

foreign currencies on cash flows and shareholders’ equity. Total

foreign currency-denominated debt was $4.5 billion and $6.1 bil-

lion at December 31, 2008 and 2007, respectively. In addition,

where practical, the Company’s restaurants purchase goods and

services in local currencies resulting in natural hedges.

The Company does not have significant exposure to any

individual counterparty and has master agreements that contain

netting arrangements. Certain of these agreements also require

each party to post collateral if credit ratings fall below, or

aggregate exposures exceed, certain contractual limits. At

December 31, 2008, neither the Company nor its counterparties

were required to post collateral on any derivative position.

The Company’s net asset exposure is diversified among a

broad basket of currencies. The Company’s largest net asset

exposures (defined as foreign currency assets less foreign cur-

rency liabilities) at year end were as follows:

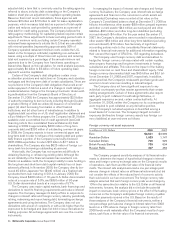

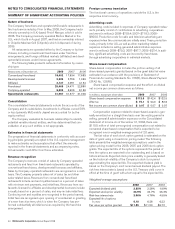

Foreign currency net asset exposures

In millions of U.S. Dollars 2008 2007

Euro $4,551 $3,999

Australian Dollars 1,023 1,147

Canadian Dollars 795 929

British Pounds Sterling 785 634

Russian Ruble 407 463

The Company prepared sensitivity analyses of its financial instru-

ments to determine the impact of hypothetical changes in interest

rates and foreign currency exchange rates on the Company’s results

of operations, cash flows and the fair value of its financial instru-

ments. The interest rate analysis assumed a one percentage point

adverse change in interest rates on all financial instruments but did

not consider the effects of the reduced level of economic activity

that could exist in such an environment. The foreign currency rate

analysis assumed that each foreign currency rate would change by

10% in the same direction relative to the U.S. Dollar on all financial

instruments; however, the analysis did not include the potential

impact on revenues, local currency prices or the effect of fluctuating

currencies on the Company’s anticipated foreign currency royalties

and other payments received in the U.S. Based on the results of

these analyses of the Company’s financial instruments, neither a

one percentage point adverse change in interest rates from 2008

levels nor a 10% adverse change in foreign currency rates from

2008 levels would materially affect the Company’s results of oper-

ations, cash flows or the fair value of its financial instruments.

36 McDonald’s Corporation Annual Report 2008