McDonalds 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

|

|

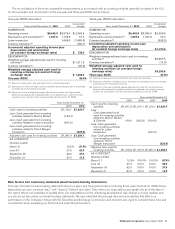

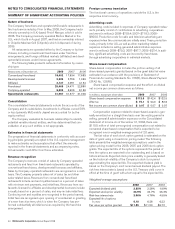

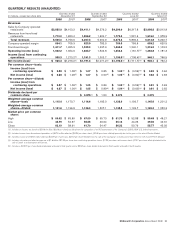

Boston Market’s and Chipotle’s results of operations (exclusive

of the transaction gains), which previously were included in Other

Countries & Corporate, consisted of revenues and pretax income

(loss) as follows:

In millions 2007 2006

Boston Market

Revenues $444.1 $691.2

Pretax income (loss) (17.0) 12.0

Chipotle

Revenues $631.7

Pretax income 39.8

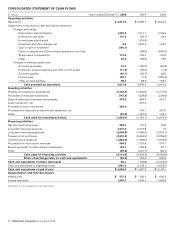

LATAM TRANSACTION

In August 2007, the Company completed the sale of its

businesses in Brazil, Argentina, Mexico, Puerto Rico, Venezuela

and 13 other countries in Latin America and the Caribbean, which

totaled 1,571 restaurants, to a developmental licensee orga-

nization. The Company refers to these markets as “Latam”. Based

on approval by the Company’s Board of Directors on April 17,

2007, the Company concluded Latam was “held for sale” as of that

date in accordance with the requirements of SFAS No. 144. As a

result, the Company recorded an impairment charge of $1.7 billion

in 2007, substantially all of which was noncash. The total charges

for the full year included $895.8 million for the difference between

the net book value of the Latam business and approximately

$675 million in cash proceeds received. This loss in value was

primarily due to a historically difficult economic environment cou-

pled with volatility experienced in many of the markets included in

this transaction. The charges also included historical foreign cur-

rency translation losses of $769.5 million recorded in

shareholders’ equity. The Company recorded a tax benefit of

$62.0 million in connection with this transaction. The tax benefit

was minimal in 2007 due to the Company’s inability to utilize most

of the capital losses generated by this transaction. As a result of

meeting the “held for sale” criteria, the Company ceased recording

depreciation expense with respect to Latam effective April 17,

2007. In connection with the sale, the Company agreed to

indemnify the buyers for certain tax and other claims, certain of

which are reflected in other long-term liabilities on McDonald’s

Consolidated balance sheet, totaling $141.8 million at

December 31, 2008 and $179.2 million at December 31, 2007.

The change in the balance was primarily due to foreign currency

translation. The Company mitigates the currency impact to income

through the use of forward foreign exchange agreements.

The buyers of the Company’s operations in Latam entered into

a 20-year master franchise agreement that requires the buyers,

among other obligations to (i) pay monthly royalties commencing at

a rate of approximately 5% of gross sales of the restaurants in

these markets, substantially consistent with market rates for similar

license arrangements; (ii) commit to adding approximately 150

new McDonald’s restaurants by the end of 2010 and pay an initial

fee for each new restaurant opened; and (iii) commit to specified

annual capital expenditures for existing restaurants.

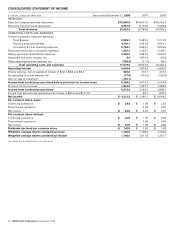

IMPAIRMENT AND OTHER CHARGES, NET

On a pretax basis, the Company recorded impairment and other

charges, net of $6.0 million in 2008, $1,670.3 million in 2007 and

$134.2 million in 2006.

In 2008, the charges primarily related to market restructuring

costs in Greece.

In 2007, the Company recorded a charge of $1.7 billion related

to the sale of the Latam businesses to a developmental licensee.

In addition, the charges for 2007 included a $15.7 million write-off

of assets associated with the Toasted Deli Sandwich products in

Canada and a net gain of $14.1 million as a result of the transfer

of the Company’s ownership interest in three European markets to

a developmental licensee, partly offset by a loss on the transfer of

a small market in Europe to a developmental licensee.

In 2006, the charges primarily related to losses of $35.8 million

incurred on the transfers of the Company’s ownership interest in

certain markets, primarily in APMEA and Europe, to developmental

licensees, costs of $35.3 million related to the closing of certain

restaurants in the U.K. in conjunction with an overall restaurant

portfolio review, costs of $29.3 million to buy out certain litigating

franchisees in Brazil, asset write-offs and other charges in APMEA

of $17.5 million, and a loss of $13.1 million related to the decision

to dispose of supply chain operations in Russia.

OTHER OPERATING (INCOME) EXPENSE, NET

In millions 2008 2007 2006

Gains on sales of restaurant

businesses $(126.5) $ (88.9) $ (38.3)

Equity in earnings of unconsolidated

affiliates (110.7) (115.6) (76.8)

Asset dispositions and other

expense 72.0 193.4 184.2

Total $(165.2) $ (11.1) $ 69.1

• Gains on sales of restaurant businesses

Gains on sales of restaurant businesses include gains from sales

of Company-operated restaurants as well as gains from exercises

of purchase options by franchisees with business facilities lease

arrangements (arrangements where the Company leases the busi-

nesses, including equipment, to franchisees who generally have

options to purchase the businesses). The Company’s purchases

and sales of businesses with its franchisees are aimed at achieving

an optimal ownership mix in each market. Resulting gains or losses

are recorded in operating income because the transactions are a

recurring part of our business.

• Equity in earnings of unconsolidated affiliates

Unconsolidated affiliates and partnerships are businesses in which

the Company actively participates but does not control. The Com-

pany records equity in earnings from these entities representing

McDonald’s share of results. For foreign affiliated markets –

primarily Japan – results are reported after interest expense and

income taxes. McDonald’s share of results for partnerships in cer-

tain consolidated markets such as the U.S. are reported before

income taxes. These partnership restaurants are operated under

conventional franchise arrangements and are included in conven-

tional franchised restaurant counts.

• Asset dispositions and other expense

Asset dispositions and other expense consists of gains or losses

on excess property and other asset dispositions, provisions for

store closings, contingencies and uncollectible receivables, and

other miscellaneous income and expenses.

McDonald’s Corporation Annual Report 2008 49