Microsoft 2013 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2013 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

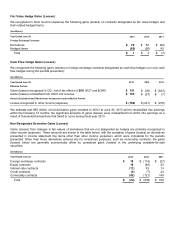

|

|

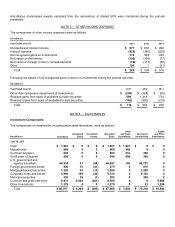

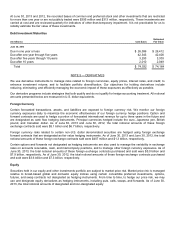

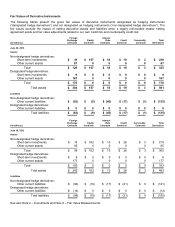

contracts purchased and sold were $898 million and $1.0 billion, respectively. As of June 30, 2012, the total notional

amounts of designated and non-designated equity contracts purchased and sold were $1.4 billion and $982 million,

respectively.

Interest Rate

Securities held in our fixed-income portfolio are subject to different interest rate risks based on their maturities. We

manage the average maturity of our fixed-income portfolio to achieve economic returns that correlate to certain broad-

based fixed-income indices using exchange-traded option and futures contracts and over-the-counter swap and option

contracts, none of which are designated as hedging instruments. As of June 30, 2013, the total notional amounts of fixed-

interest rate contracts purchased and sold were $1.1 billion and $809 million, respectively. As of June 30, 2012, the total

notional amounts of fixed-interest rate contracts purchased and sold were $3.2 billion and $1.9 billion, respectively.

In addition, we use “To Be Announced” forward purchase commitments of mortgage-backed assets to gain exposure to

agency mortgage-backed securities. These meet the definition of a derivative instrument in cases where physical delivery

of the assets is not taken at the earliest available delivery date. As of June 30, 2013 and 2012, the total notional derivative

amounts of mortgage contracts purchased were $1.2 billion and $1.1 billion, respectively.

Credit

Our fixed-income portfolio is diversified and consists primarily of investment-grade securities. We use credit default swap

contracts, not designated as hedging instruments, to manage credit exposures relative to broad-based indices and to

facilitate portfolio diversification. We use credit default swaps as they are a low cost method of managing exposure to

individual credit risks or groups of credit risks. As of June 30, 2013, the total notional amounts of credit contracts

purchased and sold were $377 million and $501 million, respectively. As of June 30, 2012, the total notional amounts of

credit contracts purchased and sold were $318 million and $456 million, respectively.

Commodity

We use broad-based commodity exposures to enhance portfolio returns and to facilitate portfolio diversification. We use

swaps, futures, and option contracts, not designated as hedging instruments, to generate and manage exposures to

broad-based commodity indices. We use derivatives on commodities as they can be low-cost alternatives to the purchase

and storage of a variety of commodities, including, but not limited to, precious metals, energy, and grain. As of June 30,

2013, the total notional amounts of commodity contracts purchased and sold were $1.2 billion and $249 million,

respectively. As of June 30, 2012, the total notional amounts of commodity contracts purchased and sold were $1.5 billion

and $445 million, respectively.

Credit-Risk-Related Contingent Features

Certain of our counterparty agreements for derivative instruments contain provisions that require our issued and

outstanding long-term unsecured debt to maintain an investment grade credit rating and require us to maintain minimum

liquidity of $1.0 billion. To the extent we fail to meet these requirements, we will be required to post collateral, similar to

the standard convention related to over-the-counter derivatives. As of June 30, 2013, our long-term unsecured debt rating

was AAA, and cash investments were in excess of $1.0 billion. As a result, no collateral was required to be posted.