Sony 2004 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2004 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

65

The year on year decrease in sales was due

to a significant decrease in intersegment sales

to the Game segment as a result of the out-

sourcing of PlayStation 2 game console pro-

duction to third parties in China. Sales to outside

customers on a yen basis increased 4.7 percent

compared with the previous fiscal year.

Regarding sales to outside customers by

geographic area, sales on a yen basis increased

in Japan by 11 percent, in Europe by 10 percent,

and in non-Japan Asia and other geographic

areas (“Other Areas”) by 8 percent. Sales on a

yen basis in the U.S. decreased 7 percent.

In Japan, mainly due to the strong sales of

Sony Ericsson, sales of cellular phones, prima-

rily to Sony Ericsson, increased significantly. In

addition, sales of charge coupled devices

(“CCDs”), which benefited from an expansion

in demand mainly from digital still cameras,

DVD recorders (including PSX), plasma and

LCD flat panel televisions, and broadcast- and

professional-use equipment increased. On the

other hand, sales of PCs and CRT televisions

decreased. In Europe, sales of digital still

cameras, flat panel televisions, cellular phones,

and PCs increased significantly. Sales of CRT

televisions, portable audio, Aiwa products, and

home audio, however, decreased. In Other

Areas, sales of CD-R/RW and DVD+/-R/RW

drives, digital still cameras, PCs, and video

cameras increased while sales of CRT televisions

decreased. In the U.S., a significant decrease in

the sales of CRT televisions combined with de-

creased sales of Aiwa products, computer dis-

plays, set-top boxes, and personal digital

assistants to cause a decline in sales, but sales

of flat panel televisions, projection televisions,

digital still cameras and PCs increased.

Performance by Product Category

Sales and operating revenue by product cat-

egory discussed below represent sales to cus-

tomers, which do not include intersegment

transactions. Refer to Note 24 of Notes to

Consolidated Financial Statements.

“Audio” sales decreased by 58.9 billion

yen, or 8.6 percent, to 623.6 billion yen. Sales

of home audio declined due to a contraction

of the market and increased price competition.

Regarding headphone stereos, sales declined

primarily due to falling prices, but the unit

shipments of both MD format and CD format

devices slightly exceeded their levels in the

previous year. Worldwide shipments of MD

format devices increased by approximately

40,000 units to approximately 3.36 million

units and worldwide shipments of CD format

devices increased by approximately 240,000

units to approximately 10.96 million units. On

the other hand, sales of car audio increased

due to strong sales in the European market.

“Video” sales increased by 97.0 billion yen,

or 11.4 percent, to 948.1 billion yen. In addition

to a significant increase in the sales of digital

still cameras outside of Japan, sales of DVD

recorders (including PSX) increased significantly

primarily in Japan. Worldwide shipments of

digital still cameras increased by approximately

4.4 million units to approximately 10 million

units. Worldwide shipments of DVD recorders

were approximately 20,000 units in the previ-

ous fiscal year but increased to approximately

650,000 units in the fiscal year ended March

31, 2004. Regarding home-use video cameras,

worldwide shipments of combined analog and

digital devices increased by approximately

850,000 units to approximately 6.6 million

units, but overall sales increased only slightly,

as sales in Japan and the U.S. decreased due to

increased price competition. DVD-video player

sales decreased due to pricing pressure,

although unit shipments increased.

“Televisions” sales decreased by 33.0 billion

yen, or 3.5 percent, to 917.2 billion yen. Sales

of CRT televisions decreased significantly due

to a contraction of the market and declining

prices, resulting primarily from a shift in

demand to flat panel televisions. Worldwide

shipments of CRT televisions decreased

approximately 600,000 units to approximately

9.4 million units compared with the previous

fiscal year. Sales of computer displays also de-

creased worldwide. On the other hand, sales

of plasma and LCD flat panel televisions in-

creased significantly worldwide and sales of

projection televisions in the U.S. increased.

Worldwide shipments of flat panel televisions

increased approximately 480,000 units to

approximately 640,000 units.

“Information and Communications” sales

decreased by 2.0 billion yen, or 0.2 percent, to

834.8 billion yen. Despite a decrease in sales in

Japan, due to price declines in the notebook

PC market, overall sales of PCs increased as

sales in all regions outside of Japan increased.

Worldwide unit shipments of PCs increased

approximately 100,000 units to approximately

3.2 million units. Sales of personal digital assis-

tants decreased due to a contraction of the

market and the effects of price declines. Sales

of broadcast- and professional-use products

were almost unchanged year on year as sales

in Japan increased due to the sale of equipment

installed in two new broadcasting stations,

while many broadcasters in the U.S. and other

countries outside of Japan reduced their capital

expenditures.

“Semiconductors” sales increased by 48.5

billion yen, or 23.7 percent, to 253.2 billion

yen. The increase was due to a significant in-

crease in sales of CCDs, mainly reflecting the

expansion of the market for digital still cameras.

Regarding LCDs, sales of low temperature poli-

silicon LCDs for digital still cameras and cellular

phones increased significantly.

“Components” sales increased by 96.0

billion yen, or 18.2 percent, to 623.8 billion

yen. The increase was primarily due to significant

increases in sales of CD-R/RW and DVD+/-R/RW

drives, and Memory Sticks. Moreover, sales of

lithium-ion batteries increased. Sales of CD-R/

RW drives increased due to a production and

sales alliance with a third party, and sales of

DVD+/-R/RW drives increased as a result of the

expansion of the market for those devices.

Worldwide shipments of Memory Stick increased

approximately 12 million units to approximately

31 million units due to the continued, strong

demand for digital still cameras. On March 31,

2004, Sony’s cumulative shipments of Memory

Stick had reached approximately 66 million

units. Regarding lithium-ion batteries, sales for

use in digital still cameras and PCs increased.

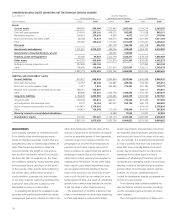

-0.0% 0.8%

-0.7%

02 03 04

0

1,000

2,000

3,000

4,000

5,000

6,000

-250

0

500

1,000

1,500

쐽Sales (left)

쐽Operating income (loss) (right)

쑗Operating margin

* Year ended March 31

Sales and operating income (loss) in the

Electronics segment

(Billion ¥) (Billion ¥)