Sony 2004 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2004 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

90

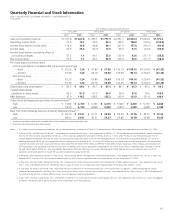

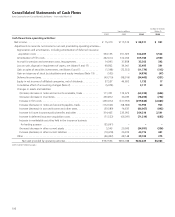

Notes: 1. U.S. dollar amounts have been translated from yen, for convenience only, at the rate of ¥104=U.S.$1, the approximate Tokyo foreign exchange market rate as of March 31, 2004.

2. Per share data for the year ended March 31, 2000 have been adjusted to reflect the two-for-one stock split that has completed on May 19, 2000. However, no adjustment to reflect such

stock split has been made to the number of shares issued at year-end.

3. In January 2003, the FASB issued FIN No. 46, “Consolidation of Variable Interest Entities — an Interpretation of ARB No. 51”. FIN No. 46 addresses consolidation by a primary beneficiary

of a VIE. For VIEs created or acquired prior to February 1, 2003, Sony early adopted the provisions of FIN No. 46 on July 1, 2003. Under FIN No. 46, any difference between the net

amount added to the balance sheet and the amount of any previously recognized interest in the VIE shall be recognized as a cumulative effect of accounting changes. As a result of

adopting the original FIN No. 46, Sony recognized a one-time charge with no tax effect of ¥2,117 million ($20 million) as a cumulative effect of accounting change in the consolidated

statement of income, and Sony’s assets and liabilities increased by ¥95,255 million ($916 million) and ¥97,950 million ($942 million), respectively. These increases were treated as non-

cash transactions in the consolidated statement of cash flows. In addition, cash and cash equivalents increased by ¥1,521 million ($15 million). In December 2003, the FASB issued FIN

No. 46R, which replaces FIN No. 46. Sony early adopted the provisions of FIN No. 46R upon its issuance. The adoption of FIN No. 46R did not have an impact on Sony’s results of

operations and financial position or impact the way Sony had previously accounted for VIEs.

4. In November 2002, the FASB issued EITF Issue No. 00-21, “Accounting for Revenue Arrangements with Multiple Deliverables”. Sony adopted EITF Issue No. 00-21 on July 1, 2003. The

adoption of EITF Issue No. 00-21 did not have a material impact on Sony’s results of operations and financial position for the year ended March 31, 2004.

5. In May 2003, the FASB issued Statement of FAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity”. Sony adopted FAS No. 150 on

April 1, 2003. The adoption of FAS No. 150 did not have an impact on Sony’s results of operations and financial position for the year ended March 31, 2004.

6. In June 2002, the FASB issued FAS No. 146, “Accounting for Costs Associated with Exit or Disposal Activities” which nullifies EITF Issue No.94-3, “Liability Recognition for Certain

Employee Termination Benefits and Other Costs to Exit an activity (including Certain Costs Incurred in a Restructuring)”. Sony adopted FAS No. 146 on January 1, 2003. The adoption of

this statement did not have a material effect on Sony’s results of operations and financial position.

7. On April 1, 2001, Sony adopted FAS No. 133, “Accounting for Derivative Instruments and Hedging Activities” as amended by FAS No.138, “Accounting for Certain Derivative

Instruments and Certain Hedging Activities — an Amendment of FASB statement No.133”. As a result, Sony’s operating income, income before income taxes and net income for the year

ended March 31, 2002 decreased by ¥3.0 billion, ¥3.4 billion and ¥2.2 billion, respectively. Additionally, Sony recorded a one-time non-cash after-tax unrealized gain of ¥1.1 billion in

accumulated other comprehensive income in the consolidated balance sheet, as well as an after-tax gain of ¥6.0 billion in the cumulative effect of accounting changes in the consolidated

statement of income. In April 2003, the FASB issued FAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging Activities”. Sony adopted FAS No. 149 on July

1, 2003. The adoption of FAS No. 149 did not have an impact on Sony’s results of operations and financial position.

8. In July 2001, the FASB issued FAS No. 142, “Goodwill and Other Intangible Assets”. Sony adopted FAS No. 142 retroactive to April 1, 2001. As a result, Sony’s operating income and

income before income taxes for the year ended March 31, 2002 increased by ¥20.1 billion and income before cumulative effect of accounting changes as well as net income for the year

ended March 31, 2002 increased by ¥18.9 billion.

9. In June 2000, the Accounting Standards Executive Committee of the American Institute of Certified Public Accountants issued Statement of Position (“SOP”) 00-2, “Accounting by

Producers or Distributors of Films”. Sony adopted SOP 00-2 retroactive to April 1, 2000. As a result, Sony’s net income for the year ended March 31, 2001 included a one-time, non-cash

charge with no tax effect of ¥101.7 billion, primarily to reduce the carrying value of its film inventory.

10. In December 1999, the Securities and Exchange Commission issued Staff Accounting Bulletin (“SAB”) No. 101, “Revenue Recognition in Financial Statements”. Sony adopted SAB No. 101

in the fourth quarter ended March 31, 2001 retroactive to April 1, 2000. As a result, a one-time no-cash cumulative effect adjustment of ¥2.8 billion was recorded in the income

statement directly above the caption of “net income” for a change in accounting principle. In December 2003, SAB No. 101 was amended by SAB No. 104, “Revenue Recognition”.

The amendment did not have an impact on Sony’s results of operations and financial position.