Sony 2004 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2004 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

80

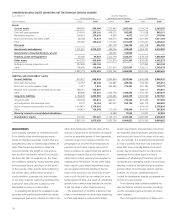

In addition, there are no financial covenants

that would cause an acceleration of the obliga-

tion in the event of a downgrade in Sony’s

credit ratings, in any of Sony’s material financ-

ing agreements.

RATINGS

In order to facilitate access to global capital

markets, Sony obtains credit ratings from two

rating agencies, Moody’s and S&P. In addition,

Sony maintains a rating from Rating and

Investment Information, Inc. (“R&I”), a rating

agency in Japan, for access to the Japanese

capital market.

Sony’s current debt ratings (long-term/

short-term) are: Moody’s: A1 (outlook: nega-

tive)/P-1; S&P: A+ (outlook: negative)/A-1; and

R&I: AA/a-1+.

On June 25, 2003, Moody’s downgraded

Sony’s long-term debt rating from Aa3 to A1

(outlook: negative). R&I downgraded Sony’s

long-term debt rating from AA+ to AA on

June 16, 2003. These actions reflected the

concerns of the two agencies that Sony may

take longer than initially expected to regain its

previous level of profit and cash flow under

the severe competition, particularly in the elec-

tronics business, and deflationary pressures.

Sony’s short-term debt rating from Moody’s

and R&I has been unaffected.

Despite the downgrading of Sony’s long-

term debt rating by Moody’s and R&I, Sony be-

lieves that its access to the global capital markets

will remain sufficient for its financing needs

going forward, and that it will retain its ability

to issue CP to meet its working capital needs.

Sony seeks to maintain a stable credit rating

in order to ensure financial flexibility for liquidity

and capital management, and to continue to

maintain adequate access to sufficient funding

resources in the financial and capital markets.

CASH MANAGEMENT

Sony is centralizing and working to make more

efficient its global cash management activities

through SGTS. The excess or shortage of cash

at most of its subsidiaries is invested or funded

by SGTS after having been netted out, although

Sony recognizes that fund transfer is limited in

certain countries or geographical areas due to

restrictions on capital transactions. In order to

pursue more efficient cash management, Sony

manages uneven cash distribution among its

subsidiaries directly or indirectly through SGTS

so that Sony can reduce unnecessary cash and

cash equivalents as well as borrowings as

much as possible.

The above description covers liquidity and

capital resources for consolidated Sony exclud-

ing Sony Life, Sony Assurance and Sony Bank,

each of which respectively secures liquidity on

its own.

FINANCIAL SERVICES SEGMENT

In the Financial Services segment, the manage-

ment of Sony Life, Sony Assurance and Sony

Bank recognize the importance of securing

sufficient liquidity to cover the payment obliga-

tions that they take on as a result of their

ordinary course of business. These companies

abide by the regulations imposed by regulatory

authorities and establish and operate under

company guidelines that comply with these

regulations. Their purpose in doing so is to main-

tain sufficient cash and cash equivalents and

secure sufficient means to pay their obligations.

Sony Life currently obtains ratings from four

rating agencies: A+ by S&P, A+ by AM Best

Corporation, and AA by R&I and the Japan

Credit Rating Agency Ltd. Sony Bank obtained

an A-/A-2 rating from S&P for its long-term/

short-term debt.

THE USE OF EVA® METHODOLOGY

Aiming to advance corporate value creation

management, Sony uses EVA®*, which reflects

cost of capital, as one of its internal evaluation

measures. The fiscal year ended March 31,

2004 marked the fourth year Sony has used

EVA®. EVA® is used in the Electronics, Game,

Music, and Pictures segments for various

internal evaluation measures such as setting,

monitoring and evaluating financial perfor-

mance targets. EVA® is also linked to compen-

sation. As a result, recognition of return on

invested capital and cost of capital has spread

further within each business unit and proactive

efforts have been made to improve EVA®.

These efforts include focusing on key busi-

nesses in order to concentrate management

resources in highly growing and profitable

areas and controlling investments and invento-

ries to improve capital efficiency.

*EVA® (Economic Value Added) is a trademark of Stern Stewart & Co.

RESEARCH AND DEVELOPMENT

Recognizing that research and development

are indispensable for business growth, Sony is

actively pursuing various technical themes,

including technologies that support current

services and those that will create new markets.

Sony has also done away with the organiza-

tional structure in which there was an Elec-

tronics Chief Technology Officer (“CTO ”), a

Co-CTO and several CTOs for each network

company, moving to a structure in which each

business domain has a CTO. In this way, a

single individual in each business domain over-

sees technological advances in that domain.

■ CTO of Home Electronics

■ CTO of Device Technology

■ CTO of Semiconductor Technology

■ CTO of Material Technology

■ CTO of Information Technology

Furthermore, in accordance with the

strengthening of research and development at

the network companies, the corporate labora-

tories were reorganized on April 1, 2004. In an

effort to reinforce basic research and develop-

ment activity in core science areas, two new

research laboratories were also established,

with the CTO of Material Technology and the

CTO of Information Technology each respon-

sible for one.

■ Materials Laboratories

■ Information Technologies Laboratories

In addition, two independent research labo-

ratories, Sony Computer Science Laboratories,

Inc. (fundamental research and user interface

research) and Sony-Kihara Research Center, Inc.

(three-dimensional computer graphics and

image processing technologies), are conducting

research and development in close collaboration

with each other.