Sony 2007 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2007 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

|

|

98

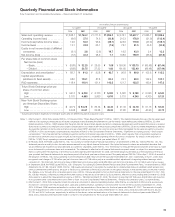

Notes: 1. In January 2003, the Financial Accounting Standards Board (“FASB”) issued FASB Interpretation (“FIN”) No. 46, “Consolidation of Variable Interest Entities—an

Interpretation of Accounting Research Bulletin (“ARB”) No. 51.” FIN No. 46 addresses the consolidation by a primary beneficiary of a variable interest entity (“VIE”).

Sony early adopted the provisions of FIN No. 46 on July 1, 2003. As a result of adopting the original FIN No. 46, Sony recognized a one-time charge with no tax

effect of 2,117 million yen as a cumulative effect of accounting change in the consolidated statement of income, and Sony’s assets and liabilities increased by

95,255 million yen and 97,950 million yen, respectively. These increases were treated as non-cash transactions in the consolidated statement of cash flows. In

addition, cash and cash equivalents increased by 1,521 million yen. Sony subsequently early adopted the provisions of FIN No. 46R, which replaced FIN No. 46,

upon issuance in December 2003. The adoption of FIN No. 46R did not have an impact on Sony’s results of operations and financial position or impact the way

Sony had previously accounted for VIEs.

2. In July 2003, the Accounting Standards Executive Committee of the American Institute of Certified Public Accountants issued Statement of Position (“SOP”) 03-1,

“Accounting and Reporting by Insurance Enterprises for Certain Nontraditional Long-Duration Contracts and for Separate Accounts.” SOP 03-1 requires insurance

enterprises to record additional reserves for long-duration life insurance contracts with minimum guarantee or annuity receivable options. Additionally, SOP 03-1

provides guidance for the presentation of separate accounts. Sony adopted SOP 03-1 on April 1, 2004. As a result of the adoption of SOP 03-1, Sony’s operating

income decreased by 5,156 million yen for the fiscal year ended March 31, 2005. Additionally, on April 1, 2004, Sony recognized a charge of 4,713 million yen (net

of income taxes of 2,675 million yen) as a cumulative effect of an accounting change.

3. In July 2004, the Emerging Issues Task Force (“EITF”) issued EITF Issue No. 04-8, “The Effect of Contingently Convertible Instruments on Diluted Earnings per

Share.” In accordance with Statement of Financial Accounting Standards (“FAS”) No. 128, “Earnings per Share,” Sony had not previously included in the

computation of diluted earnings per share (“EPS”) the number of potential common stock issuable upon the conversion of contingently convertible debt

instruments (“Co-Cos”) that had not met the conditions to exercise the stock acquisition rights. EITF Issue No. 04-8 requires that the maximum number of

common stock that could be issued upon the conversion of Co-Cos be included in diluted EPS computations from the date of issuance regardless of whether the

conditions to exercise the stock acquisition rights have been met. Sony adopted EITF Issue No. 04-8 during the quarter ended December 31, 2004. As a result of

the adoption of EITF Issue No. 04-8, Sony’s diluted EPS of income before cumulative effect of an accounting change and net income for the fiscal year ended

March 31, 2004 were restated. Sony’s diluted EPS of income before cumulative effect of an accounting change and net income for the fiscal year ended March

31, 2005 decreased by 7.26 yen and 7.06 yen, respectively, as a result of adopting EITF Issue No. 04-8.

4. Effective April 1, 2006, Sony adopted FAS No. 123 (revised 2004), “Share-Based Payment” (“FAS No. 123(R)”). This statement requires the use of the fair value-

based method of accounting for employee stock-based compensation and eliminates the alternative to use the intrinsic value method prescribed by Accounting

Principle Board Opinion (“APB”) No. 25. With limited exceptions, FAS No. 123(R) requires that the grant-date fair value of share-based payments to employees be

expensed over the period the service is received. Sony had accounted for its employee stock-based compensation in accordance with the provisions prescribed

by APB No. 25 and its related interpretations and had disclosed the net effect on net income and net income per share (“EPS”) allocated to the common stock as

if Sony had applied the fair value recognition provisions of FAS No. 123 to stock-based compensation as described in Note 2 to the Consolidated Financial

Statements, “Significant accounting policies—Stock-based compensation.” Sony has elected the modified prospective method of transition prescribed in FAS No.

123(R), which requires that compensation expense be recorded for all unvested stock acquisition rights as the requisite service is rendered beginning with the first

period of adoption. As a result of the adoption of FAS No. 123(R), Sony’s operating income decreased by 3,670 million yen for the fiscal year ended March 31, 2007.

5. In February 2006, the FASB issued FAS No. 155, “Accounting for Certain Hybrid Financial Instruments,” an amendment of FAS No. 133 and FAS No. 140. This

statement permits an entity to elect fair value remeasurement for any hybrid financial instrument if the hybrid instrument contains an embedded derivative that

would otherwise be required to be bifurcated and accounted for separately under FAS No. 133. The election to measure the hybrid instrument at fair value is made

on an instrument-by-instrument basis and is irreversible. The statement is effective for all financial instruments acquired, issued, or subject to a remeasurement

event occurring after the beginning of an entity’s fiscal year beginning after September 15, 2006, with earlier adoption permitted as of the beginning of the fiscal

year, provided that financial statements for any interim period of that fiscal year have not been issued. Sony early adopted FAS No. 155 on April 1, 2006. As a

result of the adoption of FAS No. 155, Sony’s operating income increased by 3,828 million yen for the fiscal year ended March 31, 2007. Additionally, on April 1,

2006, Sony recognized a net charge of 3,785 million yen (net of income taxes of 2,148 million yen) as a cumulative-effect adjustment to beginning retained

earnings, which consisted of 1,754 million yen (net of income taxes of 996 million yen) of gross gains and 5,539 million yen (net of income taxes of 3,144 million

yen) of gross losses.

6. In September 2006, the FASB issued FAS No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans,” an amendment to FASB

Statements No. 87, 88, 106 and 132(R). FAS No. 158 requires an employer to recognize the overfunded or underfunded status of a defined benefit pension and

other postretirement benefit plan as an asset or liability in its statement of financial position and to recognize changes in that funded status in the year in which the

changes occur through other comprehensive income. FAS No. 158 was adopted by Sony in the financial statements for the fiscal year ended March 31, 2007. FAS

No. 158 also requires companies to measure the funded status of the plan as of the date of its fiscal year-end, effective for years ending after December 15, 2008.

Sony expects to adopt the measurement provisions of FAS No. 158 effective March 31, 2009. The impact of adopting FAS 158 was a 9,508 million yen reduction in

accumulated other comprehensive income. Refer to Note 14 to the Consolidated Financial Statements, “Pension and severance plans,” for further details.

7. Effective April 1, 2006, Sony reclassified royalty income as a component of sales and operating revenue, rather than as a component of other income as

previously recorded. In connection with this reclassification, sales and operating revenue, operating income and other income for the fiscal years ended March 31,

2003, 2004, 2005 and 2006 have been reclassified to conform with the presentation of these items for the fiscal year ended March 31, 2007. The amounts of

royalty income reclassified from other income to sales and operating revenue for the fiscal years ended March 31, 2003, 2004, 2005 and 2006 were 32,375,

34,244, 31,709, and 35,161 million yen, respectively. In addition to the above, certain reclassifications of the financial statements for the fiscal years ended March

31, 2003, 2004, 2005 and 2006 have been made to conform to the presentation for the fiscal year ended March 31, 2007.