Sony 2007 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2007 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

93

past several years and will result in an increase in pension costs

as they are recognized.

Sony recorded a minimum pension liability adjustment for the

unfunded accumulated benefit obligation for Japanese pension

plans of 35.8 billion yen as of March 31, 2006. FAS No. 158 was

adopted by Sony in the financial statements for the year ended

March 31, 2007. As a result, Sony recorded a pension liability

adjustment for the prior service cost, net actuarial loss and

obligation existing at transition for Japanese pension plans of

73.5 billion yen as of March 31, 2007. Both adjustments were

established by a charge to stockholders’ equity, resulting in no

impact to the accompanying consolidated statements of

income. Refer to Note 14 of Notes to Consolidated Financial

Statements for more information regarding Sony’s pension and

severance plans.

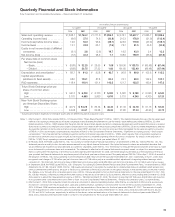

The following table illustrates the effect of changes in the

discount rate and the expected return on pension plan assets,

while holding all other assumptions constant, for Japanese

pension plans as of March 31, 2007.

CHANGE IN ASSUMPTION

Yen in billions

Pre-tax Pension Equity

PBO costs (net of tax)

25 basis point increase /

decrease in discount rate . . .

–/+ 24.9 –/+2.0 +/–1.2

25 basis point increase /

decrease in expected

return on assets. . . . . . . . . .

— –/+ 1.3 +/–0.8

■STOCK-BASED COMPENSATION

Sony accounts for stock-based compensation using the fair

value-based method. The fair value is measured on the date of

grant using the Black-Scholes option-pricing model. Sony

estimates the forfeiture rate based on its historical experience for

the stock acquisition rights plans, and recognizes this compen-

sation expense, net of an estimated forfeiture rate, only for the

stock acquisition rights expected to vest over the requisite

service period. The expense is mainly included in selling, general

and administrative expenses.

The Black-Scholes option-pricing model requires various

highly judgmental assumptions including expected stock price

volatility and the expected life of each award. In addition,

judgment is also required to estimate the expected forfeiture rate

and recognize expense only for those rights expected to vest.

Management believes that these estimates are reasonable;

however, if actual results differ significantly from these estimates,

stock-based compensation expense may differ materially in the

future from that recorded in the current period.

■DEFERRED TAX ASSET VALUATION

Sony records a valuation allowance to reduce the deferred tax

assets to an amount that management believes is more likely

than not to be realized. In establishing the appropriate valuation

allowance for deferred tax assets (including deferred tax assets

on tax loss carry-forwards), all available evidence, both positive

and negative, is considered. Information on historical results is

supplemented by all currently available information on future

years, because realization of deferred tax assets is dependent on

whether each tax-filing unit generates sufficient taxable income.

The estimates and assumptions used in determining future tax-

able income are consistent with those used in Sony’s approved

forecasts of future operations. Although realization is not assured,

management believes it is more likely than not that all of the

deferred tax assets, less valuation allowance, will be realized.

SCE and SCEA have recorded cumulative losses in recent

years primarily due to the sale of the PS3 at a price lower than

production cost during the introductory period, the recording of

other charges in association with the preparation for the launch

of the PS3 platform and a write-down for semiconductor

components used in the PS3. However, Sony expects to

establish the same successful business model with the PS3

that it achieved with the PS2, which has sold over 100 million

units. Taxable income is expected to increase during the tax

carryforward period due to the rapid reduction in hardware

production costs and an enhanced lineup of software titles in

the PS3 business. Accordingly, both companies expect to

recover these losses within the next five years.

Given sufficiently strong evidence to support the conclusion

that a valuation allowance is not necessary, Sony has decided

not to record a valuation allowance for SCE and SCEA’s

deferred tax assets.

■FILM ACCOUNTING

An aspect of film accounting that requires the exercise of

judgment relates to the process of estimating the total revenues

to be received throughout a film’s life cycle. Such estimate of

a film’s ultimate revenue is important for two reasons. First,

while a film is being produced and the related costs are being

capitalized, it is necessary for management to estimate the

ultimate revenue, less additional costs to be incurred, including

exploitation costs which are expensed as incurred, in order to

determine whether the value of a film has been impaired and

thus requires an immediate write off of unrecoverable film costs.

Second, the amount of film costs recognized as cost of sales for

a given film as it is exhibited in various markets throughout its life

cycle is based upon the proportion that current period actual

revenues bear to the estimated ultimate total revenues.