Sysco 2007 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

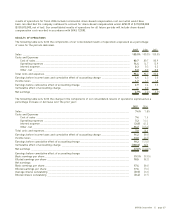

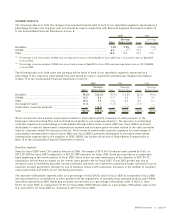

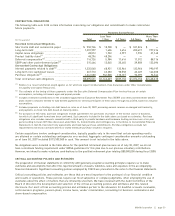

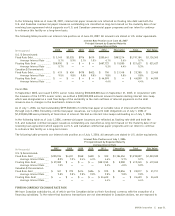

CONTRACTUAL OBLIGATIONS

The following table sets forth certain information concerning our obligations and commitments to make contractual

future payments:

(In thousands) Total

Less Than

1 Year 1-3 Years 3-5 Years

More Than

5 Years

Payments Due by Period

Recorded Contractual Obligations:

Short-term debt and commercial paper ______________ $ 550,726 $ 18,900 $ — $ 531,826 $ —

Long-term debt ___________________________________ 1,201,957 1,636 2,416 200,691 997,214

Capital lease obligations ___________________________ 28,012 1,932 2,997 1,935 21,148

Product liability claim

(1)

____________________________ 48,296 48,296 — — —

Deferred compensation

(2)

___________________________ 116,726 5,984 11,614 11,012 88,116

SERP and other postretirement plans

(3)

______________ 215,464 12,045 30,465 39,858 133,096

Unrecorded Contractual Obligations:

Interest payments related to debt

(4)

__________________ 1,325,060 68,931 132,966 132,966 990,197

Long-term non-capitalized leases ___________________ 367,710 63,383 98,558 63,469 142,300

Purchase obligations

(5)

_____________________________ 1,241,580 942,500 110,137 92,399 96,544

Total contractual cash obligations ___________________ $5,095,531 $1,163,607 $389,153 $1,074,156 $2,468,615

(1)

Relates to a recent arbitration award against us for which we expect reimbursement. (See discussion under Other Considerations

in Liquidity and Capital Resources).

(2)

The estimate of the timing of future payments under the Executive Deferred Compensation Plan involves the use of certain

assumptions, including retirement ages and payout periods.

(3)

Includes estimated contributions to the unfunded Supplemental Executive Retirement Plan (SERP) and other postretirement benefit

plans made in amounts needed to fund benefit payments for vested participants in these plans through fiscal 2016, based on actuarial

assumptions.

(4)

Includes payments on floating rate debt based on rates as of June 30, 2007, assuming amount remains unchanged until maturity,

and payments on fixed rate debt based on maturity dates.

(5)

For purposes of this table, purchase obligations include agreements for purchases of product in the normal course of business,

for which all significant terms have been confirmed. Such amounts included in the table above are based on estimates. Purchase

obligations also includes amounts committed with a third party to provide hardware and hardware hosting services over a ten year

period ending in fiscal 2015 (See discussion under Note 16, Commitments and Contingencies, in the Notes to Consolidated Financial

Statements in Item 8), fixed electricity agreements and fixed fuel purchase commitments. Purchase obligations exclude full

requirements electricity contracts where no stated minimum purchase volume is required.

Certain acquisitions involve contingent consideration, typically payable only in the event that certain operating results

are attained or certain outstanding contingencies are resolved. Aggregate contingent consideration amounts outstanding

as of June 30, 2007 included $113,303,000 in cash. This amount is not included in the table above.

No obligations were included in the table above for the qualified retirement plan because as of July 30, 2007, we do not

have a minimum funding requirement under ERISA guidelines for this plan due to our previous voluntary contributions.

However, we intend to make voluntary contributions to the qualified retirement plan totaling $80,000,000 during fiscal 2008.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in conformity with generally accepted accounting principles requires us to make

estimates and assumptions that affect the reported amounts of assets, liabilities, sales and expenses in the accompanying

financial statements. Significant accounting policies employed by SYSCO are presented in the notes to the financial statements.

Critical accounting policies and estimates are those that are most important to the portrayal of our financial condition

and results of operations. These policies require our most subjective or complex judgments, often employing the use of

estimates about the effect of matters that are inherently uncertain. We have reviewed with the Audit Committee of the

Board of Directors the development and selection of the critical accounting policies and estimates and this related

disclosure. Our most critical accounting policies and estimates pertain to the allowance for doubtful accounts receivable,

self-insurance programs, pension plans, income taxes, vendor consideration, accounting for business combinations and

share-based compensation.

SYSCO Corporation ][ page 25