Sysco 2007 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

Allowance for Doubtful Accounts

We evaluate the collectibility of accounts receivable and determine the appropriate reserve for doubtful accounts based

on a combination of factors. In circumstances where we are aware of a specific customer’s inability to meet its financial

obligation, a specific allowance for doubtful accounts is recorded to reduce the receivable to the net amount reasonably

expected to be collected. In addition, allowances are recorded for all other receivables based on analysis of historical

trends of write-offs and recoveries. We utilize specific criteria to determine uncollectible receivables to be written off,

including bankruptcy, accounts referred to outside parties for collection and accounts past due over specified periods.

If the financial condition of our customers were to deteriorate, additional allowances may be required.

Self-Insurance Program

We maintain a self-insurance program covering portions of workers’ compensation, general liability and vehicle liability

costs. The amounts in excess of the self-insured levels are fully insured by third party insurers. We also maintain a fully

self-insured group medical program. Liabilities associated with these risks are estimated in part by considering historical

claims experience, medical cost trends, demographic factors, severity factors and other actuarial assumptions. Projections

of future loss expenses are inherently uncertain because of the random nature of insurance claims occurrences and

could be significantly affected if future occurrences and claims differ from these assumptions and historical trends.

In an attempt to mitigate the risks of workers’ compensation, vehicle and general liability claims, safety procedures

and awareness programs have been implemented.

Pension Plans

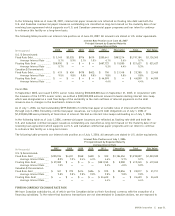

Amounts related to defined benefit plans recognized in the financial statements are determined on an actuarial basis.

Three of the more critical assumptions in the actuarial calculations are the discount rate for determining the current value

of plan benefits, the assumption for the rate of increase in future compensation levels and the expected rate of return on

plan assets.

The measurement date for the pension and other postretirement benefit plans is fiscal year-end for fiscal years 2005 and

prior. In the first quarter of fiscal 2006, we changed the measurement date for pension and other postretirement benefit

plans from fiscal year-end to May 31st to assist us in meeting accelerated SEC filing dates. As a result of this change,

we recorded a cumulative effect of a change in accounting, which increased net earnings for fiscal 2006 by $9,285,000, net

of tax. With the issuance of SFAS 158 (See Accounting Changes for further discussion), we have elected to early adopt the

measurement date provision in order to adopt both provisions of this accounting standard at the same time. As a result,

beginning in fiscal 2008, the measurement date will return to correspond with our fiscal year-end. We have performed

measurements as of May 31, 2007 and June 30, 2007 of our plan assets and benefit obligations. We will record a charge

to opening retained earnings in the first quarter of fiscal 2008 of $3,572,000, net of tax, for the impact of the difference

in our pension expense between the two measurement dates. We will also record a benefit to opening accumulated other

comprehensive loss in the first quarter of fiscal 2008 of $22,780,000, net of tax, for the impact of the difference in our

recognition provision between the two measurement dates. The measurement date used to determine fiscal 2008 net

pension costs for all plans was June 30, 2007.

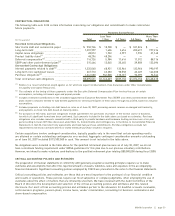

For guidance in determining the discount rates, we calculate the implied rate of return on a hypothetical portfolio of high-

quality fixed-income investments for which the timing and amount of cash outflows approximates the estimated payouts

of the pension plan. The discount rate assumption is reviewed annually and revised as deemed appropriate. The discount

rate assumptions utilized impact the recorded amount of net pension costs. The discount rate utilized to determine net

pension costs for fiscal 2007 increased 1.13% to 6.73% from the discount rate utilized to determine net pension costs for

fiscal 2006 of 5.60%. Of the $56,001,000 decrease in net pension costs for fiscal 2007, this 1.13% increase in the discount

rate decreased SYSCO’s net pension costs for fiscal 2007 by approximately $52,576,000 primarily because the higher

discount rate in fiscal 2007 generated less amortization of unrecognized actuarial losses in fiscal 2007 as compared to

fiscal 2006. The discount rate for determining fiscal 2008 net pension costs for the qualified pension plan (Retirement

Plan), which was determined as of the June 30, 2007 measurement date, increased 0.05% to 6.78%. The discount rate for

determining fiscal 2008 net pension costs for the SERP, which was determined as of the June 30, 2007 measurement date,

decreased 0.09% to 6.64%. The combined effect of these discount rate changes will decrease our net pension costs for

all plans for fiscal 2008 by an estimated $480,000. A 1.0% increase in the discount rates for fiscal 2008 would decrease

SYSCO’s net pension cost by $19,000,000, while a 1.0% decrease in the discount rates would increase pension expense

by $37,000,000. The impact of a 1.0% increase in the discount rates differ from the impact of a 1.0% decrease in discount

page 26 ][ SYSCO Corporation