Sysco 2007 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

the financial statements. Additionally, FIN 48 provides guidance on the measurement, derecognition, classification and

disclosure of tax positions, along with accounting for the related interest and penalties. The provisions of FIN 48 are

effective for fiscal years beginning after December 15, 2006, and therefore became effective for SYSCO on July 1, 2007.

While we continue to analyze the financial statement impact resulting from the adoption of FIN 48, we estimate that the

cumulative effect adjustment may result in an increase to tax liabilities of $70,000,000 to $100,000,000, with an offsetting

charge to beginning retained earnings.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (SFAS 157). SFAS 157 defines fair value,

establishes a framework for measuring fair value in accordance with generally accepted accounting principles, and

expands disclosures about fair value measurements. The statement is effective for fiscal years beginning after

November 15, 2007. We are currently evaluating the impact of the provisions of SFAS 157.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Liabilities” (SFAS 159).

SFAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value that are

not currently required to be measured at fair value. SFAS 159 also establishes presentation and disclosure requirements

designed to facilitate comparisons between entities that choose different measurement attributes for similar types of

assets and liabilities. SFAS 159 is effective as of the beginning of an entity’s first fiscal year that begins after November 15,

2007. We are currently evaluating the impact the adoption of SFAS 159 may have on our consolidated financial statements.

FORWARD-LOOKING STATEMENTS

Certain statements made herein that look forward in time or express management’s expectations or beliefs with respect

to the occurrence of future events are forward-looking statements under the Private Securities Litigation Reform Act

of 1995. They include statements about SYSCO’s ability to increase its market share and sales, long-term debt to

capitalization target ratios, anticipated capital expenditures, expected benefits of strategic business initiatives including

the timing and expected benefits of the National Supply Chain project and related redistribution centers, the potential

outcome of ongoing tax audits and SYSCO’s ability to meet future cash requirements and remain profitable.

These statements are based on management’s current expectations and estimates; actual results may differ materially

due in part to the risk factors discussed at Item 1.A. above and elsewhere. In addition, SYSCO’s ability to increase its

market share and sales, meet future cash requirements and remain profitable could be affected by conditions in the

economy and the industry and internal factors such as the ability to control expenses, including fuel costs. The ability to

meet long-term debt to capitalization target ratios also may be affected by cash flow including amounts spent on share

repurchases and acquisitions and internal growth.

ITEM 7A. Quantitative and Qualitative Disclosures About Market Risk

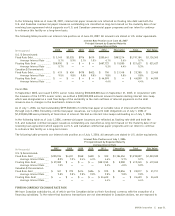

INTEREST RATE RISK

We do not utilize financial instruments for trading purposes. Our use of debt directly exposes us to interest rate risk.

Floating rate debt, where the interest rate fluctuates periodically, exposes us to short-term changes in market interest

rates. Fixed rate debt, where the interest rate is fixed over the life of the instrument, exposes us to changes in market

interest rates reflected in the fair value of the debt and to the risk that we may need to refinance maturing debt with new

debt at higher rates.

We manage our debt portfolio to achieve an overall desired position of fixed and floating rates and may employ interest

rate swaps as a tool to achieve that goal. The major risks from interest rate derivatives include changes in the interest

rates affecting the fair value of such instruments, potential increases in interest expense due to market increases in

floating interest rates and the creditworthiness of the counterparties in such transactions.

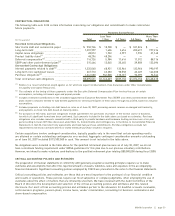

Fiscal 2007

As of June 30, 2007, we had outstanding $531,826,000 of commercial paper at variable rates of interest with maturities

through September 24, 2007. Excluding commercial paper issuances, our long-term debt obligations as of June 30, 2007

of $1,229,969,000 were primarily at fixed rates of interest. We had no interest rate swaps outstanding as of June 30, 2007.

page 30 ][ SYSCO Corporation