Sysco 2007 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

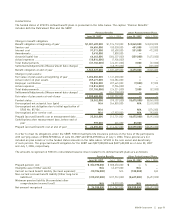

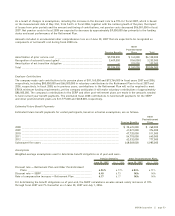

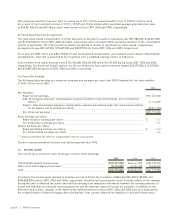

Accumulated other comprehensive loss as of June 30, 2007 consists of the following amounts that have not yet been

recognized in net benefit cost:

Pension Benefits

Other

Postretirement

Plans Total

Unrecognized prior service cost____________________________________ $ 45,678,000 $ 591,000 $ 46,269,000

Unrecognized actuarial losses (gains)_______________________________ 158,906,000 (2,741,000) 156,165,000

Unrecognized transition obligation _________________________________ — 920,000 920,000

Total ___________________________________________________________ $204,584,000 $(1,230,000) $203,354,000

Prior to the adoption of the recognition and disclosure provisions of SFAS 158, minimum pension liability adjustments

resulted when the accumulated benefit obligation exceeded the fair value of plan assets and was recorded so that the

recorded pension liability is at a minimum equal to the unfunded accumulated benefit obligation. Minimum pension liability

adjustments were non-cash adjustments that were reflected as an increase (or decrease) in the pension liability and an

offsetting charge (or benefit) to shareholders’ equity, net of tax, through comprehensive loss (or income) rather than net

income. The amounts reflected in accumulated other comprehensive income related to minimum pension liability, was

a charge of $18,030,000 as of July 1, 2006.

The accumulated benefit obligation for the defined benefit pension plans was $1,377,832,000 and $1,187,185,000 as of

June 30, 2007 and July 1, 2006, respectively.

Information for plans with accumulated benefit obligation/aggregate benefit obligation in excess of fair value of plan

assets is as follows:

June 30, 2007 July 1, 2006 June 30, 2007 July 1, 2006

Pension Benefits Other Postretirement Plans

Accumulated benefit obligation/aggregate benefit obligation __ $262,541,000 $238,599,000 $8,675,000 $8,045,000

Fair value of plan assets at end of year ____________________ ————

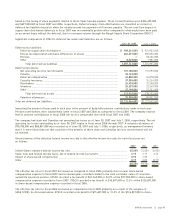

Components of Net Benefit Costs

The components of net pension costs for each fiscal year are as follows:

2007 2006 2005

Pension Benefits

Service cost ______________________________________________________ $ 84,654,000 $ 100,028,000 $ 81,282,000

Interest cost ______________________________________________________ 91,311,000 83,600,000 73,824,000

Expected return on plan assets _____________________________________ (116,744,000) (104,174,000) (82,613,000)

Amortization of prior service cost ___________________________________ 5,684,000 4,934,000 1,760,000

Recognized net actuarial loss _______________________________________ 9,686,000 46,204,000 32,605,000

Net pension costs _________________________________________________ $ 74,591,000 $ 130,592,000 $106,858,000

The components of other postretirement benefit costs for each fiscal year are as follows:

2007 2006 2005

Other Postretirement Plans

Service cost _____________________________________________________________ $ 451,000 $ 510,000 $ 477,000

Interest cost _____________________________________________________________ 531,000 472,000 488,000

Expected return on plan assets_____________________________________________ ———

Amortization of prior service cost ___________________________________________ 201,000 202,000 202,000

Recognized net actuarial gain ______________________________________________ (132,000) (15,000) —

Amortization of net transition obligation _____________________________________ 154,000 153,000 154,000

Net other postretirement benefit costs ______________________________________ $1,205,000 $1,322,000 $1,321,000

page 52 ][ SYSCO Corporation