Sysco 2007 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

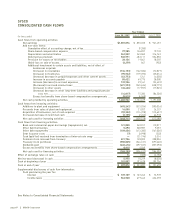

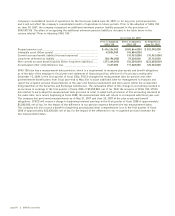

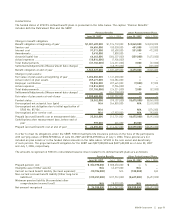

company’s consolidated results of operations for the fiscal year ended June 30, 2007, or for any prior period presented,

and it will not affect the company’s consolidated results of operations in future periods. Prior to the adoption of SFAS 158

on June 30, 2007, the company recognized an additional minimum pension liability pursuant to the provisions of

SFAS 87/106. The effect of recognizing the additional minimum pension liability is included in the table below in the

column labeled “Prior to Adopting SFAS 158.”

Prior to Adopting

SFAS 158

Effect of Adopting

SFAS 158

As Reported at

June 30, 2007

As of June 30, 2007

Prepaid pension cost __________________________________________ $ 436,236,000 $ (83,846,000) $ 352,390,000

Intangible asset (Other assets) _________________________________ 43,854,000 (43,854,000) —

Current accrued benefit liability (Accrued expenses) ______________ — (10,967,000) (10,967,000)

Long-term deferred tax liability ________________________________ (38,196,000) 73,328,000 35,132,000

Non-current accrued benefit liability (Other long-term liabilities) ___ (271,369,000) (52,289,000) (323,658,000)

Accumulated other comprehensive loss _________________________ 7,637,000 117,628,000 125,265,000

SFAS 158 also has a measurement date provision, which is a requirement to measure plan assets and benefit obligations

as of the date of the employer’s fiscal year-end statement of financial position, effective for fiscal years ending after

December 15, 2008. In the first quarter of fiscal 2006, SYSCO changed the measurement date for pension and other

postretirement benefit plans from fiscal year-end to May 31st to allow additional time for management to evaluate and

report the actuarial pension measurements in the year-end financial statements and disclosures within the accelerated

filing deadlines of the Securities and Exchange Commission. The cumulative effect of this change in accounting resulted in

an increase to earnings in the first quarter of fiscal 2006 of $9,285,000, net of tax. With the issuance of SFAS 158, SYSCO

has elected to early adopt the measurement date provision in order to adopt both provisions of this accounting standard at

the same time. As a result, beginning in fiscal 2008, the measurement date will return to correspond with fiscal year-end.

The company has performed measurements as of May 31, 2007 and June 30, 2007 of the plan assets and benefit

obligations. SYSCO will record a charge to beginning retained earnings in the first quarter of fiscal 2008 of approximately

$4,000,000, net of tax, for the impact of the difference in our pension expense between the two measurement dates.

The company will also record a benefit to beginning accumulated other comprehensive loss in the first quarter of fiscal

2008 of approximately $23,000,000, net of tax, for the impact of the difference in our recognition provision between the

two measurement dates.

page 50 ][ SYSCO Corporation