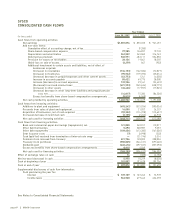

Sysco 2007 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

Long-Lived Assets

Management reviews long-lived assets, including finite-lived intangibles, for indicators of impairment whenever events or

changes in circumstances indicate that the carrying value may not be recoverable. Cash flows expected to be generated by

the related assets are estimated over the asset’s useful life based on updated projections. If the evaluation indicates that

the carrying amount of the asset may not be recoverable, the potential impairment is measured based on a projected

discounted cash flow model.

Goodwill and Intangibles

Goodwill and intangibles represent the excess of cost over the fair value of tangible net assets acquired. Goodwill and

intangibles with indefinite lives are not amortized. Intangibles with definite lives are amortized on a straight-line basis

over their useful lives, which generally range from three to ten years.

Goodwill is assigned to the reporting units that are expected to benefit from the synergies of the combination. The

recoverability of goodwill and indefinite-lived intangibles is assessed annually, or more frequently as needed when events

or changes have occurred that would suggest an impairment of carrying value, by determining whether the fair values of

the applicable reporting units exceed their carrying values. The reporting units used to assess goodwill impairment are

the company’s six operating segments as described in Note 17, Business Segment Information. The components within

each of the six operating segments have similar economic characteristics and therefore are aggregated into six reporting

units. The evaluation of fair value requires the use of projections, estimates and assumptions as to the future performance

of the operations in performing a discounted cash flow analysis, as well as assumptions regarding sales and earnings

multiples that would be applied in comparable acquisitions.

Derivative Financial Instruments

SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities” (SFAS 133), requires the recognition of

all derivatives as assets or liabilities within the consolidated balance sheets at fair value. Gains or losses on derivative

financial instruments designated as fair value hedges are recognized immediately in the consolidated results of

operations, along with the offsetting gain or loss related to the underlying hedged item.

Gains or losses on derivative financial instruments designated as cash flow hedges are recorded as a separate component

of shareholders’ equity until settlement (or until hedge ineffectiveness is determined), whereby gains or losses are

reclassified to the Consolidated Results of Operations in conjunction with the recognition of the underlying hedged item.

To the extent that the periodic changes in the fair value of the derivatives are not effective, or if the hedge ceases to

qualify for hedge accounting, the ineffective portion of the periodic non-cash changes are recorded in operating expenses

in the consolidated results of operations in the period of the change.

Certain agreements entered into by the company for the procurement of fuel, electricity and product commodities related

to SYSCO’s business meet the definition of a derivative. The company has assessed these agreements and determined that

they qualify for the normal purchase and sale exemption under SFAS 133 (as amended and interpreted) and documents

and accounts for them accordingly.

Treasury Stock

The company records treasury stock purchases at cost. Shares removed from treasury are valued at cost using the

average cost method.

Foreign Currency Translation

The assets and liabilities of all Canadian subsidiaries are translated at current exchange rates. Related translation

adjustments are recorded as a component of accumulated other comprehensive income (loss).

Revenue Recognition

The company recognizes revenue from the sale of a product when it is considered to be realized or realizable and earned.

The company determines these requirements to be met at the point at which the product is delivered to the customer.

The company grants certain customers sales incentives such as rebates or discounts and treats these as a reduction of

sales at the time the sale is recognized. Sales tax collected from customers is not included in revenue but rather recorded

page 42 ][ SYSCO Corporation