Sysco 2007 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2007 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

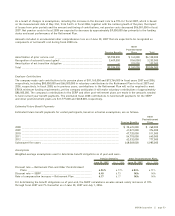

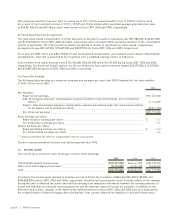

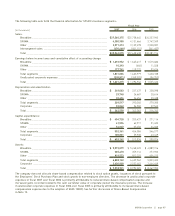

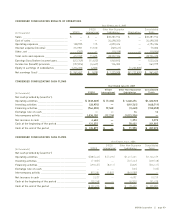

Certain acquisitions involve contingent consideration typically payable only in the event that certain operating results are

attained or certain outstanding contingencies are resolved. Aggregate contingent consideration amounts outstanding as

of June 30, 2007 included $113,303,000 in cash, which, if distributed, could result in the recording of additional goodwill.

Such amounts are to be paid out over periods of up to four years from the date of acquisition if the contingent criteria

are met.

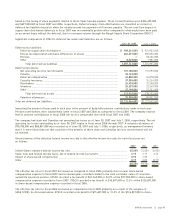

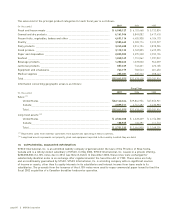

16. COMMITMENTS AND CONTINGENCIES

SYSCO is engaged in various legal proceedings which have arisen but have not been fully adjudicated. These proceedings,

in the opinion of management, will not have a material adverse effect upon the consolidated financial position or results

of operations of the company when ultimately concluded.

Product Liability Claim

In July, 2007, SYSCO was found contractually liable in arbitration proceedings related to a product liability claim from

one of its former customers. As of June 30, 2007, the company has recorded $50,296,000 on its consolidated balance

sheet within accrued expenses related to the accrual of this loss. Also as of June 30, 2007, a corresponding receivable

of $48,296,000 is included in the consolidated balance sheet within prepaid expenses and other current assets, which

represents the estimate of the loss less the $2,000,000 deductible on SYSCO’s insurance policy. The company has hold

harmless agreements with the product suppliers and is named as an additional insured party under the suppliers’ policies

with their insurers. Further, SYSCO maintains its own product liability insurance with coverage related to this claim.

The company believes it is probable that it will be able to recover the recorded loss from one or more of these sources.

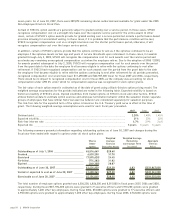

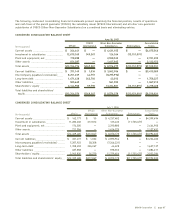

Multi-Employer Pension Plans

SYSCO contributes to several multi-employer defined benefit pension plans based on obligations arising under collective

bargaining agreements covering union-represented employees. Approximately 11% of SYSCO’s current employees are

participants in such multi-employer plans. In fiscal 2007, total contributions to these plans were approximately

$37,296,000.

SYSCO does not directly manage these multi-employer plans, which are generally managed by boards of trustees, half

of whom are appointed by the unions and the other half by other contributing employers to the plan. Based upon the

information available from plan administrators, management believes that some of these multi-employer plans are

under-funded due partially to a decline in the value of the assets supporting these plans, a reduction in the number of

actively participating members for whom employer contributions are required, and the level of benefits provided by the

plans. In addition, the Pension Protection Act, enacted in August 2006, will require under-funded pension plans to improve

their funding ratios within prescribed intervals based on the level of their under-funding, perhaps beginning as soon as

calendar 2008. As a result, SYSCO’s required contributions to these plans may increase in the future.

Under current law regarding multi-employer defined benefit plans, a plan’s termination, SYSCO’s voluntary withdrawal,

or the mass withdrawal of all contributing employers from any under-funded multi-employer defined benefit plan would

require SYSCO to make payments to the plan for SYSCO’s proportionate share of the multi-employer plan’s unfunded

vested liabilities. SYSCO does not believe that it is probable that there will be a mass withdrawal of employers from the

plans or that any of the plans will terminate in the near future. In addition, if a multi-employer defined benefit plan fails

to satisfy certain minimum funding requirements, the IRS may impose a nondeductible excise tax of 5% on the amount

of the accumulated funding deficiency for those employers contributing to the fund.

Based on the information available from plan administrators, SYSCO estimates that its share of withdrawal liability on all

the multi-employer plans it participates in could be as much as $120,000,000.

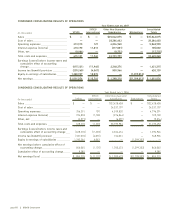

BSCC Cooperative Structure

SYSCO’s affiliate, BSCC, is a cooperative taxed under subchapter T of the United States Internal Revenue Code. SYSCO

believes that the deferred tax liabilities resulting from the business operations and legal ownership of BSCC are

appropriate under the tax laws. However, if the application of the tax laws to the cooperative structure of BSCC were to

be successfully challenged by any federal, state or local tax authority, SYSCO could be required to accelerate the payment

of all or a portion of its income tax liabilities associated with BSCC that it otherwise has deferred until future periods in

that event, would be liable for interest on such amounts. As of June 30, 2007, SYSCO has recorded deferred income tax

SYSCO Corporation ][ page 63