Sysco 2014 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2014 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

SYSCO CORPORATION-Form10-K40

PARTII

ITEM7Management’s Discussion and Analysis ofFinancial Condition and Results of Operations

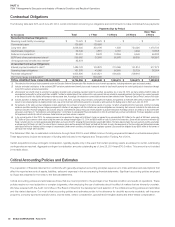

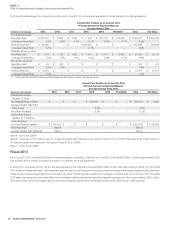

Contractual Obligations

The following table sets forth, as of June 28, 2014, certain information concerning our obligations and commitments to make contractual future payments:

(Inthousands)

Payments Due by Period

Total < 1 Year 1-3 Years 3-5 Years

More Than

5Years

Recorded Contractual Obligations:

Revolving credit facility borrowings $ 70,975 $ 70,975 $ - $ - $ -

Commercial paper 129,999 129,999 - - -

Long-term debt 2,526,305 300,196 1,356 754,020 1,470,733

Capital lease obligations 32,640 4,581 6,757 4,944 16,358

Deferred compensation(1) 80,910 8,428 13,259 9,940 49,283

SERP and other postretirement plans(2) 299,582 26,608 56,568 59,809 156,597

Unrecognized tax bene ts and interest(3) 85,878

Unrecorded Contractual Obligations:

Interest payments related to debt(4) 1,486,128 106,876 210,065 191,814 977,373

Operating lease obligations 161,838 43,065 56,960 25,729 36,084

Purchase obligations(5) 4,603,890 3,404,821 990,450 208,619 -

US Foods merger consideration(6) 5,316,110 500,000 - - 4,816,110

TOTAL CONTRACTUAL CASH OBLIGATIONS $ 14,794,255 $ 4,595,549 $ 1,335,415 $ 1,254,875 $ 7,522,538

(1) The estimate of the timing of future payments under the Executive Deferred Compensation Plan involves the use of certain assumptions, including retirement ages and payout periods.

(2) Includes estimated contributions to the unfunded SERP and other postretirement benefit plans made in amounts needed to fund benefit payments for vested participants in these plans through

fiscal 2024, based on actuarial assumptions.

(3) Unrecognized tax benefits relate to uncertain tax positions recorded under accounting standards related to uncertain tax positions. As of June 28, 2014, we had a liability of $49.2 million for

unrecognized tax benefits for all tax jurisdictions and $36.7 million for related interest that could result in cash payment. We are not able to reasonably estimate the timing of non-current payments

or the amount by which the liability will increase or decrease over time. Accordingly, the related non-current balances have not been reflected in the “Payments Due by Period” section of the table.

(4) Includes payments on floating rate debt based on rates as of June 28, 2014, assuming amount remains unchanged until maturity, and payments on fixed rate debt based on maturity dates. The

impact of our outstanding fixed-to-floating interest rate swap on the fixed rate debt interest payments is included as well based on the floating rates in effect as of June 28, 2014.

(5) For purposes of this table, purchase obligations include agreements for purchases of product in the normal course of business, for which all significant terms have been confirmed, including

minimum quantities resulting from our category management initiative. As we progress with this initiative, our purchase obligations are increasing. Such amounts included in the table above are

based on estimates. Purchase obligations also includes amounts committed with various third party service providers to provide information technology services for period up to fiscal 2019 (See

discussion under Note 20, “Commitments and Contingencies”, to the Notes to Consolidated Financial Statements in Item 8) and fixed fuel purchase commitments. Purchase obligations exclude

full requirements electricity contracts where no stated minimum purchase volume is required.

(6) In the second quarter of fiscal 2014, the company announced an agreement to merge with US Foods. Sysco has agreed to pay approximately $3.7 billion for the equity of US Foods, comprising

$3.2 billion of Sysco common stock valued using the seven day average through August 13, 2014 and $500 million of cash. As part of the transaction, Sysco will also assume or refinance US

Foods’ net debt, which is currently approximately $4.8 billion as of June 28, 2014, bringing the total enterprise value to $8.5 billion. The table above includes the cash payment and the assumption

or refinancing of US Foods’ net debt. The value of Sysco’s common stock and the amount of US Foods’ net debt will fluctuate. As such, the components of the transaction and total enterprise value

noted above will not be finalized until the merger is consummated. Under certain conditions, including lack of regulatory approval, Sysco would be obligated to pay $300 million to the owners of

US Foods if the merger were cancelled.

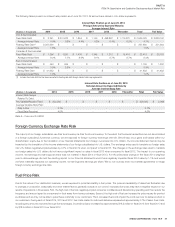

The Retirement Plan has no estimated contributions through scal 2024 to meet ERISA minimum funding requirements based on actuarial assumptions.

These assumptions include the extension of funding relief included in the Highway and Transportation Funding Act of 2014.

Certain acquisitions involve contingent consideration, typically payable only in the event that certain operating results are attained or certain outstanding

contingencies are resolved. Aggregate contingent consideration amounts outstanding as of June 28, 2014 were $70.6 million. This amount is not included

in the table above.

Critical Accounting Policies and Estimates

The preparation of nancial statements in conformity with generally accepted accounting principles requires us to make estimates and assumptions that

affect the reported amounts of assets, liabilities, sales and expenses in the accompanying nancial statements. Signi cant accounting policies employed

by Sysco are presented in the notes to the nancial statements.

Critical accounting policies and estimates are those that are most important to the portrayal of our nancial condition and results of operations. These

policies require our most subjective or complex judgments, often employing the use of estimates about the effect of matters that are inherently uncertain.

We have reviewed with the Audit Committee of the Board of Directors the development and selection of the critical accounting policies and estimates

and this related disclosure. Our most critical accounting policies and estimates pertain to the allowance for doubtful accounts receivable, self-insurance

programs, company-sponsored pension plans, income taxes, vendor consideration, goodwill and intangible assets and share-based compensation.