Sysco 2014 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2014 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

SYSCO CORPORATION-Form10-K 71

PARTII

ITEM8Financial Statements and Supplementary Data

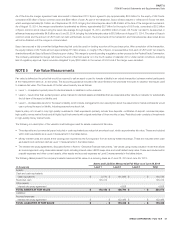

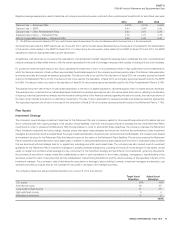

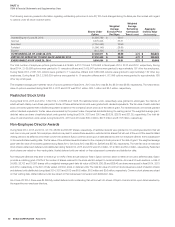

Weighted-average assumptions used to determine net company-sponsored pension costs and other postretirement bene t costs for each scal year were:

2014 2013 2012

Discount rate — Retirement Plan 5.32% 4.81% 5.94%

Discount rate — SERP 4.94 3.96(1) 5.93

Discount rate — Other Postretirement Plans 5.32 4.81 5.94

Expected rate of return — Retirement Plan 7.75 7.75 7.75

Rate of compensation increase — Retirement Plan 3.89 5.30 5.30

(1) The SERP was remeasured in November 2012 as a result of the plan freeze discussed above. The rate in the table above reflects the discount rate as of this remeasurement.

As bene t accruals under the SERP were frozen as of June 29, 2013, due to the plan freeze discussed above, future pay is not projected in the determination

of net pension costs related to the SERP for scal 2014. For determining the net pension costs related to the SERP for scal 2013 and 2012, the SERP

calculations utilized an age-graded salary growth assumption.

A healthcare cost trend rate is not used in the calculations of postretirement bene t obligations because Sysco subsidizes the cost of postretirement

medical coverage by a xed dollar amount, with the retiree responsible for the cost of coverage in excess of the subsidy, including all future cost increases.

For guidance in determining the discount rate, Sysco calculates the implied rate of return on a hypothetical portfolio of high-quality xed-income investments for

which the timing and amount of cash out ows approximates the estimated payouts of the company-sponsored pension plans. The discount rate assumption

is reviewed annually and revised as deemed appropriate. The discount rate to be used for the calculation of scal 2015 net company-sponsored bene t

costs for the Retirement Plan is 4.74%. The discount rate to be used for the calculation of scal 2015 net company-sponsored bene t costs for the SERP

is 4.59%. The discount rate to be used for the calculation of scal 2015 net company-sponsored bene t costs for the Other Postretirement Plans is 4.74%.

The expected long-term rate of return on plan assets assumption is net return on assets assumption, representing gross return on assets less plan expenses.

The expected return is derived from a mathematical asset model that incorporates assumptions as to the various asset class returns, re ecting a combination

of rigorous historical performance analysis and the forward-looking views of the nancial markets regarding the yield on bonds, the historical returns of

the major stock markets and returns on alternative investments. The rate of return assumption is reviewed annually and revised as deemed appropriate.

The expected long-term rate of return to be used in the calculation of scal 2015 net company-sponsored bene t costs for the Retirement Plan is 7.75%.

Plan Assets

Investment Strategy

The company’s overall strategic investment objectives for the Retirement Plan are to preserve capital for future bene t payments and to balance risk and

return commensurate with ongoing changes in the valuation of plan liabilities. Over time, the company intends to decrease the risk of the Retirement Plan’s

investments in order to preserve the Retirement Plan’s funded status. In order to accomplish these objectives, the company oversees the Retirement

Plan’s investment objectives and policy design, decides proper plan asset class strategies and structures, monitors the performance of plan investment

managers and investment funds and determines the proper investment allocation of pension plan contributions and withdrawals. The company has created

an investment structure for the Retirement Plan that takes into account the nature of the Retirement Plan’s liabilities. This structure ensures the Retirement

Plan’s investments are diversi ed within each asset class, in addition to being diversi ed across asset classes with the intent to build asset class portfolios

that are structured without strategic bias for or against any subcategories within each asset class. The company has also created a set of investment

guidelines for the Retirement Plan’s investment managers to specify prohibited transactions, including borrowing of money except for real estate, private

equity or hedge fund portfolios where leverage is a key component of the investment strategy and permitted in the investments’ governing documents,

the purchase of securities on margin unless fully collateralized by cash or cash equivalents or short sales, pledging, mortgaging or hypothecating of any

securities, except for loans of securities that are fully collateralized, market timing transactions and the direct purchase of the securities of Sysco or the

investment manager. The purchase or sale of derivatives for speculation or leverage is also prohibited; however, investment managers are allowed to use

derivative securities so long as they do not increase the risk pro le or leverage of the manager’s portfolio.

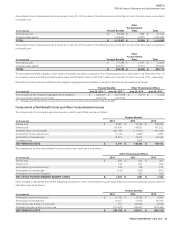

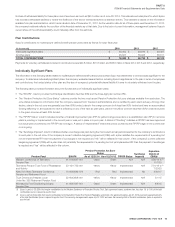

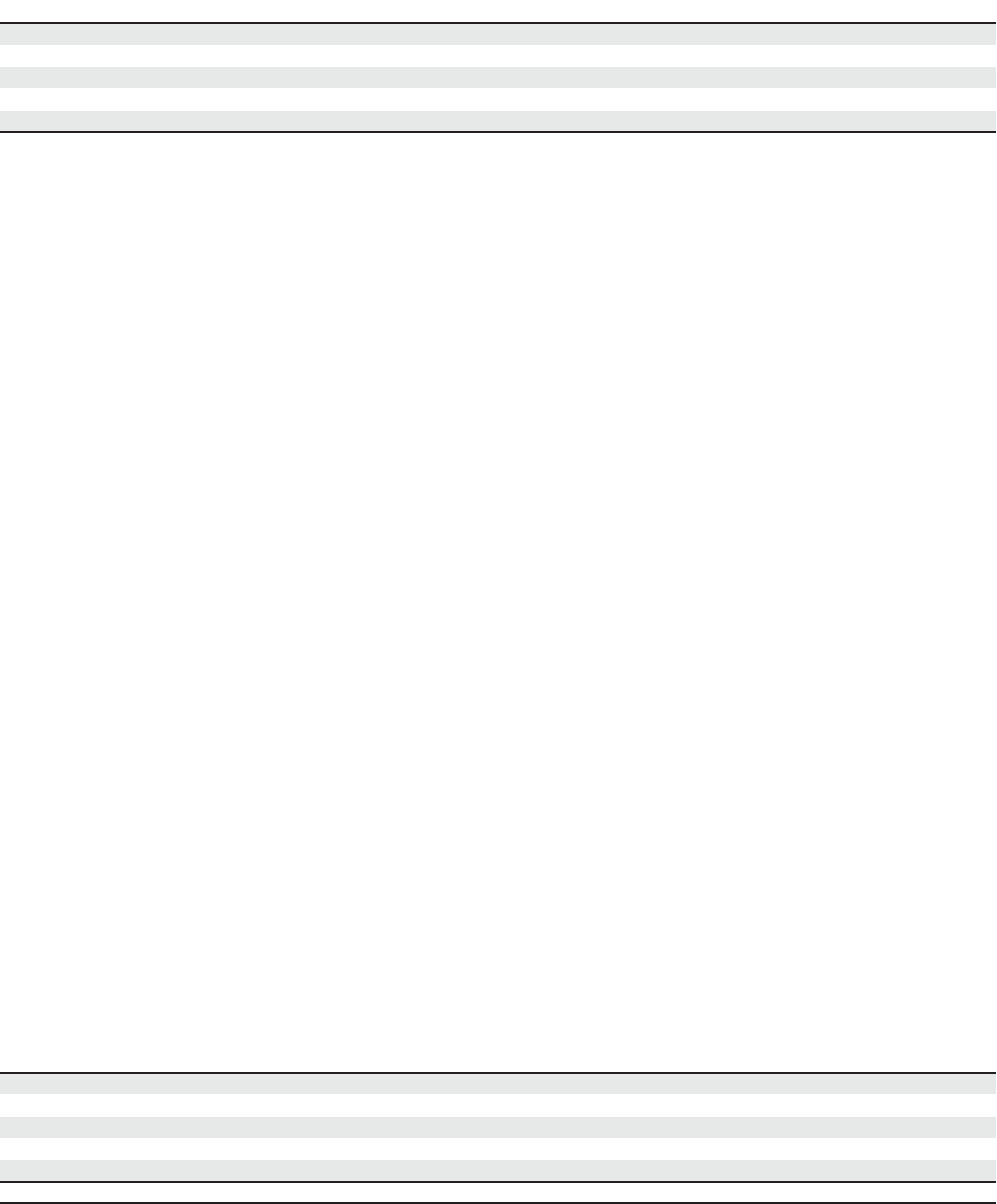

The company’s target and actual investment allocation as of June 28, 2014 is as follows:

Target Asset

Allocation

Actual Asset

Allocation

U.S. equity 29% 39%

International equity 29 25

Long duration xed income 27 26

High yield xed income 5 4

Alternative investments 10 6

100%