Target 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

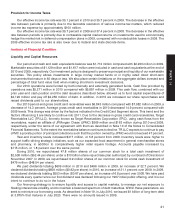

Outlook

Our outlook is based on the application of business judgment in light of current business trends, our

assumptions regarding the macroeconomic environment, and estimates of the impact of current initiatives, the

most significant of which are our store remodel program, the new 5 percent REDcard Rewards program, and our

planned Canadian expansion.

In the Retail Segment, we expect that comparable-store sales will increase in the 4 to 5 percent range in 2011.

We expect that our store remodel program will contribute incremental comparable-store sales, and net of the

adverse impact of remodel disruption, this impact will grow to a run rate of about 1.5 percentage points as we

progress through the year. Separately we expect that the sales contribution of our 5% REDcard Rewards program

will grow more rapidly in its importance, adding up to 2 percentage points to our same store sales growth later in

2011. These estimates are based on extrapolations of the current performance of these programs.

In 2011 we expect to produce a full-year EBIT margin rate consistent with 2010, due to favorable leverage of

SG&A and depreciation and amortization expenses offsetting the gross margin rate declines associated with our

store remodel and new rewards strategies. This offsetting impact is unlikely to occur in the spring, particularly in the

first quarter, resulting in modest pressure on EBIT margin rate in the spring, and modest favorability on this measure

in the fall.

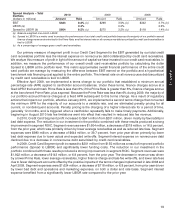

In our Credit Card Segment, we expect receivables will continue to decline in 2011, with the pace of the decline

moderating as the year progresses. We expect that the allowance for doubtful accounts will continue to decline in

2011 as well, due to this decline in receivables and expected continued improvement in portfolio risks. We also

expect measures of our rate of portfolio profitability to remain strong in 2011. Additionally, in January 2011 we

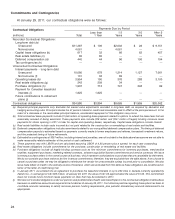

announced our plan to actively pursue the sale of our credit card receivables portfolio. As of January 29, 2011 the

gross balance of our credit card receivables portfolio was $6,843 million, of which $3,954 million was funded by

third parties and $2,889 million was funded by Target.

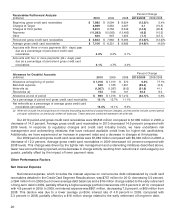

In January 2011, we entered into an agreement to purchase the leasehold interests in up to 220 sites in Canada

currently operated by Zellers Inc., in exchange for C$1,825 million, due in two payments, one in May 2011 and one

in September 2011. We believe this transaction will allow us to open 100 to 150 Target stores in Canada, primarily

during 2013. We expect that renovation of these stores will require an investment of over C$1 billion, a portion of

which may be funded by landlords. Our direct costs associated with entry into Canada may add expenses equating

to an earnings per share (EPS) equivalent in the range of $0.10 for 2011, an estimate that will continue to evolve over

time. We currently believe the aggregate effect of our Canadian expansion could result in a $0.15 to $0.20

unfavorable impact on 2011 EPS, reflecting direct incremental expenses and the indirect impact of the Canadian

investment on the pace of share repurchase. We expect that the 2012 dilutive EPS impact of the Canadian

expansion will exceed the 2011 dilutive EPS impact, due primarily to a full year of lease-related expenses.

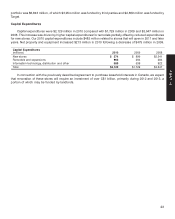

We expect 2011 capital expenditures related to our U.S. retail operations to be approximately $2.5 billion,

driven primarily by a larger remodel program. We expect to open 21 new stores in the U.S. in 2011, adding

approximately 15 new locations net of closings and relocations.

We also expect to continue to execute against our share repurchase plan, although at a slower pace due to our

Canadian expansion, investing in the range of $1.5 billion to $2.0 billion during 2011. The timing and amount of

share repurchase activity will be dependent on market conditions and the amount of future net earnings and cash

flows.

We expect our 2011 effective tax rate to be in the range of 36 to 37 percent.

Forward-Looking Statements

This report contains forward-looking statements, which are based on our current assumptions and

expectations. These statements are typically accompanied by the words ‘‘expect,’’ ‘‘may,’’ ‘‘could,’’ ‘‘believe,’’

‘‘would,’’ ‘‘might,’’ ‘‘anticipates,’’ or words of similar import. The principal forward-looking statements in this report

include: For our Retail Segment, our outlook for sales, comparable-store sales trends, including the impact of our

store remodel and 5% REDcard Rewards programs, and EBIT margin rates; for our Credit Card Segment, our

outlook for year-end gross credit card receivables, future write-offs of current receivables, rate of portfolio

28