Target 2010 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2010 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

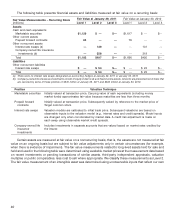

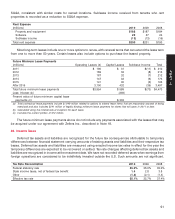

20. Derivative Financial Instruments

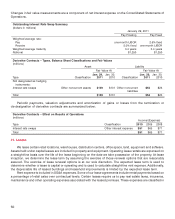

Derivative financial instruments are reported at fair value on the Consolidated Statements of Financial Position.

Historically our derivative instruments have primarily consisted of interest rate swaps. We use these derivatives to

mitigate our interest rate risk. We have counterparty credit risk resulting from our derivative instruments. This risk

lies primarily with two global financial institutions. We monitor this concentration of counterparty credit risk on an

ongoing basis.

Prior to 2009, the majority of our derivative instruments qualified for fair value hedge accounting treatment. The

changes in market value of an interest rate swap, as well as the offsetting change in market value of the hedged

debt, were recognized within earnings in the current period. We assessed at the inception of the hedge whether the

hedging derivatives were highly effective in offsetting changes in fair value or cash flows of hedged items.

Ineffectiveness resulted when changes in the market value of the hedged debt were not completely offset by

changes in the market value of the interest rate swap. For those derivatives whose terms met the conditions of the

‘‘short-cut method,’’ 100 percent hedge effectiveness was assumed. There was no ineffectiveness recognized in

2010, 2009 or 2008 related to our derivative instruments. As detailed below, at January 29, 2011, there were no

derivative instruments designated as accounting hedges.

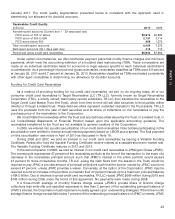

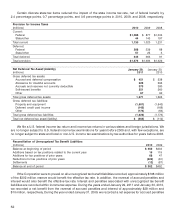

During the first quarter of 2008, we terminated certain ‘‘pay floating’’ interest rate swaps with a combined

notional amount of $3,125 million for cash proceeds of $160 million, which are classified within other operating cash

flows in the Consolidated Statements of Cash Flows. These swaps were designated as hedges; therefore,

concurrent with their terminations, we were required to stop making market value adjustments to the associated

hedged debt. Gains realized upon termination will be amortized into earnings over the remaining life of the

associated hedged debt.

Additionally, during 2008, we de-designated certain ‘‘pay floating’’ interest rate swaps, and upon

de-designation, these swaps no longer qualified for hedge accounting treatment. As a result of the de-designation,

the unrealized gains on these swaps determined at the date of de-designation will be amortized into earnings over

the remaining lives of the previously hedged items.

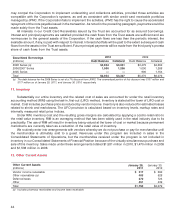

In 2010, 2009 and 2008, total net gains amortized into net interest expense for terminated and de-designated

swaps were $45 million, $60 million and $55 million, respectively. The amount remaining on unamortized hedged

debt valuation gains from terminated and de-designated interest rate swaps that will be amortized into earnings

over the remaining lives of the previously hedged debt totaled $152 million, $197 million and $263 million, at the end

of 2010, 2009 and 2008, respectively.

Simultaneous to the de-designations during 2008, we entered into ‘‘pay fixed’’ swaps to economically hedge

the risks associated with the de-designated ‘‘pay floating’’ swaps. These swaps are not designated as hedging

instruments and along with the de-designated ‘‘pay floating’’ swaps are measured at fair value on a quarterly basis.

49

PART II