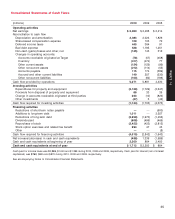

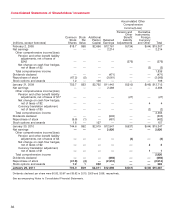

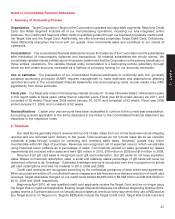

Target 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

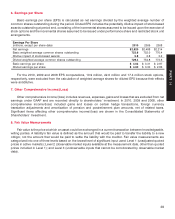

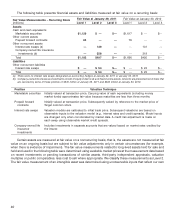

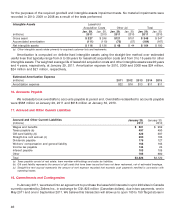

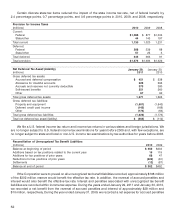

January 2011. The credit quality segmentation presented below is consistent with the approach used in

determining our allowance for doubtful accounts.

Receivables Credit Quality

(millions) 2010 2009

Nondelinquent accounts (Current and 1 - 29 days past due)

FICO score of 700 or above $2,819 $2,886

FICO score of 600 to 699 2,737 3,114

FICO score below 600 868 1,272

Total nondelinquent accounts 6,424 7,272

Delinquent accounts (30+ days past due) 419 710

Period-end gross credit card receivables $6,843 $7,982

Under certain circumstances, we offer cardholder payment plans that modify finance charges and minimum

payments, which meet the accounting definition of a troubled debt restructuring (TDR). These concessions are

made on an individual cardholder basis for economic or legal reasons specific to each individual cardholder’s

circumstances. As a percentage of period-end gross receivables, receivables classified as TDRs were 5.9 percent

at January 29, 2011 and 6.7 percent at January 30, 2010. Receivables classified as TDRs are treated consistently

with other aged receivables in determining our allowance for doubtful accounts.

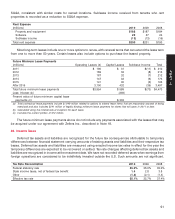

Funding for Credit Card Receivables

As a method of providing funding for our credit card receivables, we sell, on an ongoing basis, all of our

consumer credit card receivables to Target Receivables LLC (TR LLC), formerly known as Target Receivables

Corporation (TRC), a wholly owned, bankruptcy remote subsidiary. TR LLC then transfers the receivables to the

Target Credit Card Master Trust (the Trust), which from time to time will sell debt securities to third parties, either

directly or through a related trust. These debt securities represent undivided interests in the Trust assets. TR LLC

uses the proceeds from the sale of debt securities and its share of collections on the receivables to pay the

purchase price of the receivables to the Corporation.

We consolidate the receivables within the Trust and any debt securities issued by the Trust, or a related trust, in

our Consolidated Statements of Financial Position based upon the applicable accounting guidance. The

receivables transferred to the Trust are not available to general creditors of the Corporation.

In 2005, we entered into a public securitization of our credit card receivables. Note holders participating in this

securitization were entitled to receive annual interest payments based on LIBOR plus a spread. The final payment

on this securitization was made in April of 2010 as discussed in Note 19.

During 2006 and 2007, we sold an interest in our credit card receivables by issuing a Variable Funding

Certificate. Parties who hold the Variable Funding Certificate receive interest at a variable short-term market rate.

The Variable Funding Certificate matures in 2012 and 2013.

In the second quarter of 2008, we sold an interest in our credit card receivables to JPMorgan Chase (JPMC).

The interest sold represented 47 percent of the receivables portfolio at the time of the transaction. In the event of a

decrease in the receivables principal amount such that JPMC’s interest in the entire portfolio would exceed

47 percent for three consecutive months, TR LLC (using the cash flows from the assets in the Trust) would be

required to pay JPMC a pro rata amount of principal collections such that the portion owned by JPMC would not

exceed 47 percent, unless JPMC provides a waiver. Conversely, at the option of the Corporation, JPMC may be

required to fund an increase in the portfolio to maintain their 47 percent interest up to a maximum principal balance

of $4.2 billion. Due to declines in gross credit card receivables, TR LLC repaid JPMC $566 million during 2010 and

$163 million during 2009 under the terms of this agreement. No payments were made during 2008.

If a three-month average of monthly finance charge excess (JPMC’s prorata share of finance charge

collections less write-offs and specified expenses) is less than 2 percent of the outstanding principal balance of

JPMC’s interest, the Corporation must implement mutually agreed-upon underwriting strategies. If the three-month

average finance charge excess falls below 1 percent of the outstanding principal balance of JPMC’s interest, JPMC

43

PART II