Verizon Wireless 2013 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2013 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

20

Wireline’srevenuesdecreased$0.6billion,or1.4%,during2013com-

pared to 2012 primarily driven by declines in Global Enterprise Core and

Global Wholesale, partially oset by higher Consumer retail revenues

drivenbyFiOSservicesandincreasedStrategicservicesrevenueswithin

Global Enterprise.

Mass Markets

MassMarketsoperationsprovidebroadbandservices(includinghigh-

speedInternet,FiOSInternetandFiOSVideoservices),localexchange

(basic service and end-user access) and long distance (including regional

toll) voice services to residential and small business subscribers.

2013 Compared to 2012

MassMarketsrevenuesincreased$0.6billion,or3.7%,during2013com-

paredto2012primarilyduetotheexpansionofFiOSservices(Voice,

Internet and Video) as well as changes in our pricing strategies, partially

oset by the continued decline of local exchange revenues.

During2013,wegrewoursubscriberbaseby0.6millionFiOSInternet

subscribersandby0.5millionFiOSVideosubscribers,whilealsoconsis-

tentlyimprovingpenetrationrateswithinourFiOSserviceareas.Asof

December 31, 2013, we achieved penetration rates of 39.5% and 35.0%

forFiOSInternetandFiOSVideo,respectively,comparedtopenetration

ratesof37.3%and33.3%forFiOSInternetandFiOSVideo,respectively,at

December 31, 2012.

TheincreaseinMassMarketsrevenues,drivenbyFiOSservices,waspar-

tially oset by the decline of local exchange revenues primarily due to a

5.2% decline in Consumer retail voice connections resulting primarily from

competition and technology substitution with wireless, VoIP, broadband

and cable services. Total voice connections include traditional switched

accesslinesinserviceaswellasFiOSdigitalvoiceconnections.There

was also a decline in Small business retail voice connections, primarily

reecting competition and a shift to both IP and high-speed circuits.

2012 Compared to 2011

MassMarketsrevenuesincreasedduring2012comparedto2011pri-

marilyduetotheexpansionofFiOSservices(Voice,InternetandVideo)

as well as changes in our pricing strategy adopted in 2012, partially oset

by the continued decline of local exchange revenues.

We continued to grow our subscriber base and improved penetration

rateswithinour FiOSserviceareasduring2012.Also contributingto

theincreaseinrevenuefromFiOSserviceswerechangesinourpricing

strategy adopted in 2012. As of December 31, 2012, we achieved pen-

etration rates of 37.3% and 33.3% for FiOS Internet and FiOSVideo,

respectively,comparedtopenetrationratesof35.5%and31.5%forFiOS

InternetandFiOSVideo,respectively,atDecember31,2011.

MassMarketsrevenueswerenegativelyimpactedbythedeclineoflocal

exchange revenues primarily due to a 6.1% decline in Consumer retail

voice connections resulting primarily from competition and technology

substitution with wireless, VoIP, broadband and cable services. Total voice

connections include traditional switched access lines in service as well

asFiOSdigitalvoiceconnections.TherewasalsoadeclineinSmallbusi-

ness retail voice connections, primarily reecting challenging economic

conditions, competition and a shift to both IP and high-speed circuits.

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS continued

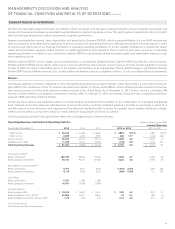

Wireline

Our Wireline segment provides voice, data and video communications products and enhanced services including broadband video and data, cor-

porate networking solutions, data center and cloud services, security and managed network services and local and long distance voice services. We

provide these products and services to consumers in the United States, as well as to carriers, businesses and government customers both in the

United States and in over 150 other countries around the world.

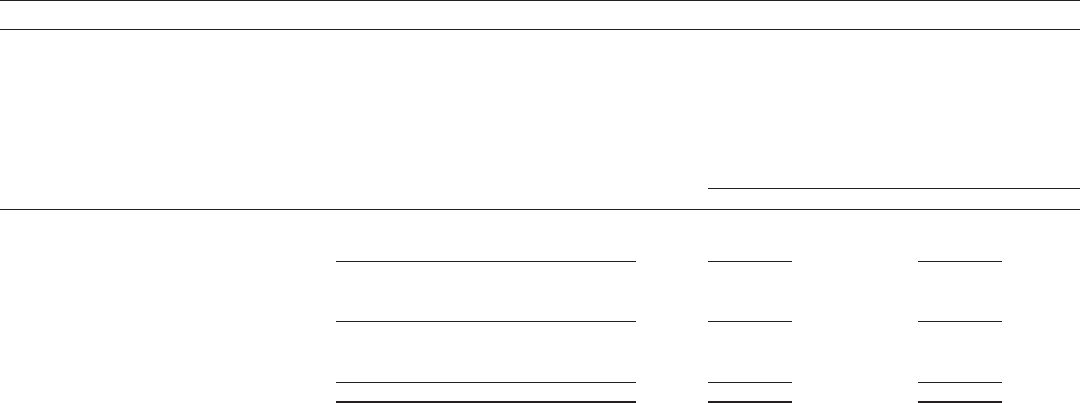

Operating Revenues and Selected Operating Statistics (dollars in millions)

Increase/(Decrease)

Years Ended December 31, 2013 2012 2011 2013 vs. 2012 2012 vs. 2011

Consumer retail $ 14,737 $ 14,043 $ 13,606 $ 694 4.9 % $ 437 3.2 %

Small business 2,591 2,659 2,731 (68) (2.6) (72) (2.6)

MassMarkets 17,328 16,702 16,337 626 3.7 365 2.2

Strategic services 8,420 8,052 7,575 368 4.6 477 6.3

Core 6,283 7,247 8,047 (964) (13.3) (800) (9.9)

Global Enterprise 14,703 15,299 15,622 (596) (3.9) (323) (2.1)

Global Wholesale 6,714 7,240 7,973 (526) (7.3) (733) (9.2)

Other 478 539 750 (61) (11.3) (211) (28.1)

Total Operating Revenues $ 39,223 $ 39,780 $ 40,682 $ (557) (1.4) $ (902) (2.2)

Connections ('000):(1)

Total voice connections 21,085 22,503 24,137 (1,418) (6.3) (1,634) (6.8)

TotalBroadbandconnections 9,015 8,795 8,670 220 2.5 125 1.4

FiOSInternetsubscribers 6,072 5,424 4,817 648 11.9 607 12.6

FiOSVideosubscribers 5,262 4,726 4,173 536 11.3 553 13.3

(1) As of end of period