Verizon Wireless 2013 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2013 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

27

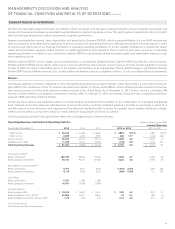

Free Cash Flow

Freecashowisanon-GAAPnancialmeasurethatmanagementbelieves

isusefultoinvestorsandotherusersofVerizon’snancialinformationin

evaluatingcashavailabletopaydebtanddividends.Freecashowiscal-

culated by subtracting capital expenditures from net cash provided by

operating activities. The following table reconciles net cash provided by

operatingactivitiestoFreecashow:

(dollars in millions)

Years Ended December 31, 2013 2012 2011

Net cash provided by operating activities $ 38,818 $ 31,486 $ 29,780

Less Capital expenditures (including

capitalized software) 16,604 16,175 16,244

Free cash ow $ 22,214 $ 15,311 $ 13,536

The changes in free cash ow during 2013, 2012 and 2011 were a result of

the factors described in connection with net cash provided by operating

activities and capital expenditures.

Employee Benet Plan Funded Status and Contributions

Pension Annuitization

On October 17, 2012, we, along with our subsidiary Verizon Investment

ManagementCorp.,andFiduciaryCounselorsInc.,asindependentdu-

ciaryoftheVerizonManagementPensionPlan(thePlan),enteredintoa

denitive purchase agreement with The Prudential Insurance Company

ofAmerica(Prudential)andPrudentialFinancial,Inc.,pursuanttowhich

the Plan would purchase a single premium group annuity contract

from Prudential.

On December 10, 2012, upon issuance of the group annuity contract by

Prudential, Prudential irrevocably assumed the obligation to make future

annuity payments to approximately 41,000 Verizon management retirees

who began receiving pension payments from the Plan prior to January 1,

2010.Theamountofeachretiree’sannuitypaymentequalstheamountof

suchindividual’spensionbenet.Inaddition,thegroupannuitycontract

is intended to replicate the same rights to future payments, such as sur-

vivor benets, that are currently oered by the Plan.

We contributed approximately $2.6 billion to the Plan between September

1, 2012 and December 31, 2012 in connection with the transaction so

thatthe Plan’sfundingpercentagewouldnotdecreaseas aresultof

the transaction.

Employer Contributions

We operate numerous qualied and nonqualied pension plans and other

postretirement benet plans. These plans primarily relate to our domestic

business units. During 2013, contributions to our qualied pension plans

were not material. During 2012 and 2011, we contributed $0.9 billion and

$0.4 billion, respectively, to our qualied pension plans, excluding the

pension annuitization discussed above. We also contributed $0.1 billion,

$0.2 billion and $0.1 billion to our nonqualied pension plans in 2013,

2012 and 2011, respectively.

In an eort to reduce the risk of our portfolio strategy and better align

assets with liabilities, we have adopted a liability driven pension strategy

that seeks to better match cash ows from investments with projected

benet payments. We expect that the strategy will reduce the likelihood

that assets will decline at a time when liabilities increase (referred to as

liability hedging), with the goal to reduce the risk of underfunding to the

plan and its participants and beneciaries, however, we also expect the

strategytoresultinlowerassetreturns.Basedonthisstrategyandthe

funded status of the plans at December 31, 2013, we expect the min-

imum required qualied pension plan contribution in 2014 to be $1.2

billion. Nonqualied pension contributions are estimated to be approxi-

mately $0.2 billion in 2014.

Common Stock

Common stock has been used from time to time to satisfy some of the

funding requirements of employee and shareowner plans, including 24.6

million common shares issued from Treasury stock during 2012, related

to dividend payments, which had an aggregate value of $1.0 billion. On

February3,2011,theBoardofDirectorsreplacedthepreviouslyautho-

rized share buyback program with a new program for the repurchase of

up to 100 million common shares terminating no later than the close

ofbusinessonFebruary28,2014.TheBoardalsodeterminedthatno

additional shares were to be purchased under the prior program. During

2013, we repurchased $0.2 billion of our common stock under this pro-

gram. There were no repurchases of common stock during 2012 or 2011.

As a result of the Wireless Transaction, Verizon issued approximately 1.27

billion shares.

Credit Ratings

Duringthethirdquarterof 2013,Verizon’s creditratingsweredown-

gradedbyMoody’sInvestorsService(Moody’s),Standard&Poor’sRatings

Services(Standard&Poor’s)andFitchRatings(Fitch)asaresultofVerizon’s

announcementoftheagreementtoacquireVodafone’s45%noncontrol-

ling interest in Verizon Wireless for approximately $130 billion including

the incurrence of third-party indebtedness to fund the cash portion of the

purchasepricefortheWirelessTransaction.Moody’sdowngradedVerizon’s

long-termdebtratingsonenotchfromA3 toBaa1,whileStandard &

Poor’s loweredits corporatecreditratingandseniorunsecureddebt

ratingonenotchfromA-toBBB+andFitchlowereditslong-termissuer

default rating and senior unsecured debt rating one notch from A to A-.

Although the ratings downgrade is not expected to signicantly impact

our access to capital, it could increase both the cost of renancing debt

and the cost of nancing any new capital requirements. Securities rat-

ings assigned by rating organizations are expressions of opinion and are

not recommendations to buy, sell or hold securities. A securities rating

is subject to revision or withdrawal at any time by the assigning rating

organization. Each rating should be evaluated independently of any

other rating.

Covenants

Our credit agreements contain covenants that are typical for large,

investment grade companies. These covenants include requirements to

pay interest and principal in a timely fashion, pay taxes, maintain insur-

ance with responsible and reputable insurance companies, preserve our

corporate existence, keep appropriate books and records of nancial

transactions, maintain our properties, provide nancial and other reports

to our lenders, limit pledging and disposition of assets and mergers and

consolidations, and other similar covenants. Additionally, the term loan

credit agreement and the 364-day revolving credit agreement require us

to maintain a leverage ratio (as such term is dened in those agreements)

not in excess of 3.50:1.00 until our credit ratings are equal to or higher

than A3 and A-.

We and our consolidated subsidiaries are in compliance with all debt

covenants.

Increase (Decrease) In Cash and Cash Equivalents

Our Cash and cash equivalents at December 31, 2013 totaled $53.5 bil-

lion, a $50.4 billion increase compared to Cash and cash equivalents at

December 31, 2012 primarily as a result of the issuance of $49.0 billion

aggregate principal amount of xed and oating rate notes.

Our Cash and cash equivalents at December 31, 2012 totaled $3.1 bil-

lion, a $10.3 billion decrease compared to Cash and cash equivalents at

December 31, 2011 as a result of the factors described in connection

with our cash ows provided by operating activities, cash ows used in

investing activities and cash ows used in nancing activities.

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS continued