Siemens 2009 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2009 Siemens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

|

|

86

Reports Supervisory Board /

Managing Board Corporate Governance Management’s discussion and analysis Consolidated Financial Statements

44 Business and operating environment 63 Fiscal 2009 – Financial summary 66 Results of operations 84 Financial position

CREDIT RATINGS

A key factor in maintaining a strong financial profile is our

credit rating which is affected among other factors by the capi-

tal structure, the profitability, the ability to generate cash flow,

geographic and product diversification as well as our competi-

tive market position. Our current corporate credit ratings from

Moody ’s Investors Service and Standard & Poor’s are noted

below:

During fiscal 2009 Moody ’s Investors Service made no rating

changes. Moody ’s applied a long-term credit rating of “A1,”

outlook stable, on November 9, 2007. The rating classification

A is the third highest rating within the agency ’s debt ratings

category. The numerical modifier 1 indicates that our long-

term debt ranks in the higher end of the A category. The

Moody ’s rating outlook is an opinion regarding the likely direc-

tion of an issuer’s rating over the medium-term. Rating out-

looks fall into the following six categories: positive, negative,

stable, developing, ratings under review and no outlook.

Moody ’s Investors Service’s rating for our short-term corporate

credit and commercial paper is P-1, the highest available rating

in the prime rating system, which assesses issuers’ ability to

honor senior financial obligations and contracts. It applies to

senior unsecured obligations with an original maturity of less

than one year.

In addition, Moody ’s Investors Service published a credit opin-

ion for us. The most recent credit opinion as of June 10, 2009

classified the liquidity profile as “very healthy.”

On June 5, 2009, Standard & Poor’s downgraded our corporate

long-term credit rating from AA– to A+. At the same time Stan-

dard & Poor’s revised its outlook from “negative” to “stable” and

announced that the rating action followed weaker cash flows

and a rising pension deficit. Within Standard & Poor’s ratings

definitions an obligation rated “A” has the third highest long-

term rating category. The modifier “+” indicates that our long-

term debt ranks in the upper end of the A category. The Stan-

dard & Poor’s rating outlook assesses the potential direction of

a long-term credit rating over the medium-term. Rating out-

looks fall into the following four categories: “positive,” ”nega-

tive,” ”stable” and “developing”. Furthermore, Standard &

Poor’s downgraded our corporate short-term credit rating from

“A-1+” to “A–1.” This is the second highest short-term rating

within the S&P rating scale.

We expect no significant impact on our funding costs as a con-

sequence of the downgrade by Standard & Poor’s.

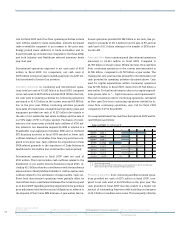

(in millions of €)

September 30,

2009 2008

Short term debt 698 1,819

Plus: Long term debt

118,940 14,260

Less: Cash and cash equivalents (10,159) (6,893)

Less: Current available for sale financial assets (170) (152)

Net debt 9,309 9,034

Less: SFS Debt excluding internally purchased

receivables (9,521) (9,359)

Plus: Funded status pension plan 4,015 2,460

Plus: Funded status other post employment

benefits 646 650

Plus: Credit guarantees 313 480

Less: approx. 50% nominal amount hybrid bond (862) (901)

Less: Fair value hedge accounting adjustment

2(1,027) (180)

Adjusted industrial net debt 2,873 2,184

EBITDA (adjusted) (continuing operations) 9,219 5,585

Adjusted industrial net debt/EBITDA

(adjusted) (continuing operations) 0.31 0.39

1 Long term debt including fair value hedge accounting adjustment of €1,027 million

and €180 million for the fiscal year ended September 30, 2009 and 2008,

respectively.

2 The fair value hedge accounting adjustment has been included in fiscal 2009 in our

definition of adjusted industrial net debt and therefore the financial information

for the prior period in this table has been adjusted accordingly. The fair value hedge

accounting adjustment is representing the change in the fair value of derivatives

relating to fixed-rate long-term debt attributable to the interest rate risk being

hedged. We believe that deducting the fair value hedge accounting adjustment from

Net debt in addition to the adjustments presented above provides to investors more

meaningful information to our scheduled debt service obligations. For further

information on fair value hedges see “Notes to Consolidated Financial Statements.”

B25T024_E

Moody’s Investors

Service

Standard &

Poor’s

Long-term debt A1 A +

Short-term debt P-1 A –1

B25T025_E