Siemens 2014 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2014 Siemens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

|

|

247 D. Consolidated Financial Statements

337 E. Additional Information

213 C. Overall assessment of the economic position

214 C. Subsequent events

215 C. Sustainability and citizenship

225 C. Report on expected developments and

associated material opportunities and risks

242 C. Compensation Report and legal disclosures

242 C. Siemens AG (Discussion on basis

of German Commercial Code)

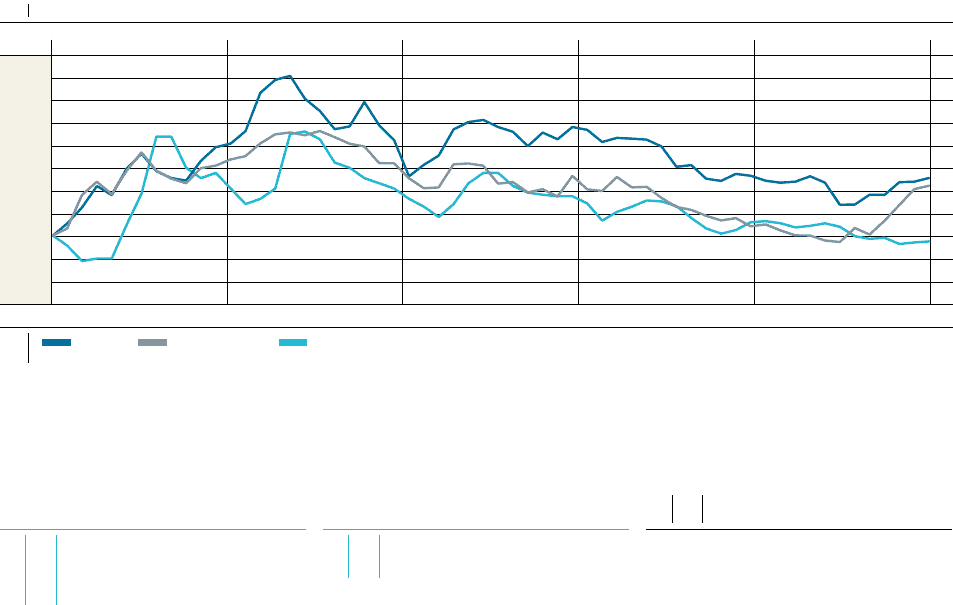

were still % lower in fiscal than the average for fiscal

, reflecting modest demand during fiscal .

Average monthly prices of aluminum traded on the London

Metal Exchange recently rebounded and were % higher

in September compared to September . Prices on a

fiscal- year average were nevertheless % lower in fiscal

than the average of fiscal . Significantly rising premiums

for physically delivered aluminum have added to the prices of

the London Metal Exchange contracts. The aluminum industry

is in a situation of a global oversupply due to rapid expansion

of capacities, while regional markets in the western world face

a tighter supply.

The average monthly steel prices for September declined

by % compared to the average monthly prices in Septem-

ber . Prices on a fiscal-year average were % lower in fiscal

than the average for fiscal .

Our main exposure to the prices of copper, aluminum and

related products is in the new Divisions Energy Management

and Process Industries and Drives. Our main price exposure

related to carbon steel and stainless steel is in our new Divi-

sions Power and Gas and Wind Power and Renewables. In addi-

tion, Siemens is generally exposed to energy and fuel prices,

both directly (electricity, gas, oil) and indirectly (energy used

in the manufacturing processes of suppliers, fuels included in

logistics costs).

Siemens employs various strategies to reduce the price risk in

its project and product businesses, such as long-term contract-

ing with suppliers, physical and financial hedging and price

escalation clauses with customers.

C... MARKET DEVELOPMENT

In fiscal , the addressed market of our Energy Sector devel-

oped stable year-over-year. Wind power markets showed the

strongest growth (both onshore and offshore). Markets for

power transmission grew slightly while market volume for

large gas turbines declined year-over-year.

Markets of the Power Generation Division declined in fiscal

compared to fiscal . In particular the advanced gas

turbine market remained difficult with a market size in fiscal

clearly below fiscal . In addition, production over-

capacities have been resulting in increased price pressure.

During the fiscal year, the overall market environment for fossil

power generation faced project shifts in various regions lead-

ing to tough competition. While key countries such as the

U.S. or China have been facing market delays, countries of the

Middle East, especially Saudi-Arabia showed higher invest-

ments in gas-fired power plants year-over-year. Demand for

industrial gas and steam turbines developed roughly flat.

Markets served by our Wind Power Division grew clearly in fis-

cal fueled by strong demand in Europe, which is the most

mature geographic market in the world for onshore and off-

shore wind power. In particular, Europe is home to almost all

offshore installations currently active worldwide. Within the

Americas, growth in the U.S. was driven by onshore wind proj-

ects, following the extension of an existing production tax

credit (PTC) for renewable energy into the first quarter of fiscal

. Market development in the Asia, Australia region was

characterized by intense local competition, particularly in

China. While China has the largest wind market in the world,

market access for foreign companies remains to be very diffi-

cult and limited. The competitive situation in the wind power

Development of raw material prices (Index: Beginning of fiscal = )

FY FY FY FY FY

Copper Aluminium (HG) Steel HRC

Source: London Metal Exchange (LME) for copper and aluminium, CRU HRC Germany for steel; cash prices in € per ton.