Electronic Arts 2006 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2006 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

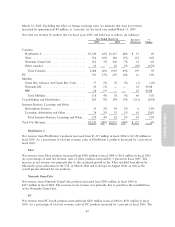

Net Income

Net income for Ñscal years 2005 and 2004 was as follows (in millions):

March 31, % of Net March 31, % of Net

2005 Revenue 2004 Revenue $ Change % Change

$504 16% $577 20% $(73) (13%)

Reported net income decreased in Ñscal 2005 as compared to Ñscal 2004 primarily due to growth in our

expenses, especially research and development, as we prepared for the adoption of next-generation

technology within our industry while at the same time we continued to devote resources to the

development of products for current-generation consoles.

Impact of Recently Issued Accounting Standards

In November 2004, the FASB issued SFAS No. 151, ""Inventory Costs Ì an amendment of ARB No. 43,

Chapter 4''. SFAS No. 151 amends the guidance in Accounting Research Bulletin No. 43, Chapter 4,

""Inventory Pricing'', to clarify the accounting for abnormal amounts of idle facility expense, freight,

handling costs, and wasted material (spoilage) and requires that those items be recognized as current-

period charges. SFAS No. 151 also requires that allocation of Ñxed production overheads to the costs of

conversion be based on the normal capacity of the production facilities. SFAS No. 151 is eÅective for

inventory costs incurred during Ñscal years beginning after June 15, 2005. We do not expect the adoption

of SFAS No. 151 to have a material impact on our Consolidated Financial Statements.

In December 2004, the FASB issued SFAS No. 123R, ""Share-Based Payment''. SFAS No. 123R requires

that the cost resulting from all share-based payment transactions be recognized in the Ñnancial statements

using a fair-value-based method. The statement replaces SFAS No. 123, ""Accounting for Stock-Based

Compensation'', supersedes Accounting Principles Board No. 25, ""Accounting for Stock Issued to

Employees'', and amends SFAS No. 95, ""Statement of Cash Flows''. While the fair value method under

SFAS No. 123R is similar to the fair value method under SFAS No. 123 with regards to measurement

and recognition of stock-based compensation, there are several key diÅerences between the two standards.

For example, SFAS No. 123 permits us to recognize forfeitures as they occur while SFAS No. 123R will

require us to estimate future forfeitures and adjust our estimate on a quarterly basis. SFAS No. 123R will

also require a classiÑcation change in the statement of cash Öows, whereby a portion of the income tax

beneÑt from stock options will move from operating cash Öow activities to Ñnancing cash Öow activities

(total cash Öows will remain unchanged). In March 2005, the Securities and Exchange Commission

(""SEC'') released SAB No. 107, ""Share-Based Payment'', which provides the SEC's views regarding the

interaction between SFAS No. 123R and certain SEC rules and regulations for public companies. In April

Annual Report

2005, the SEC adopted a rule that amends the compliance dates of SFAS No. 123R. Under the revised

compliance dates, we are required to adopt the provisions of SFAS No. 123R no later than our Ñrst

quarter of Ñscal 2007. The expensing of stock-based compensation will have a material adverse impact on

our Consolidated Statements of Operations and may not be similar to our pro forma disclosure under

SFAS No. 123, as amended.

In October 2005, the FASB issued FASB StaÅ Position (""FSP'') Financial Accounting Standard

(""FAS'') No. 123(R) 2, ""Practical Accommodation to the Application of Grant Date As DeÑned in FASB

Statement No. 123(R)''. The FASB provides companies with a ""practical accommodation'' when

determining the grant date of an award subject to SFAS No. 123R. If (1) the award is a unilateral grant,

that is, the recipient does not have the ability to negotiate the key terms and conditions of the award with

the employer, (2) the key terms and conditions of the award are expected to be communicated to an

individual recipient within a relatively short time period, and (3) as long as all other criteria in the grant

date deÑnition have been met, then a mutual understanding of the key terms and conditions of an award is

presumed to exist at the date the award is approved. In November 2005, the FASB issued FSP

FAS No. 123(R)-3, ""Transition Election Related to Accounting for the Tax EÅects of Share-Based

Payment Awards''. The FASB allows for a practical exception in calculating the additional paid Ì in

capital pool of excess tax beneÑts upon adoption that is available to absorb tax deÑciencies recognized

53