Electronic Arts 2006 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2006 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

assets associated with our hedging activities are recorded at fair value in other current assets in our

Consolidated Balance Sheet. The eÅective portion of gains or losses resulting from changes in fair value of

these hedges is initially reported, net of tax, as a component of accumulated other comprehensive income

in stockholders' equity and subsequently reclassiÑed into net revenue or operating expenses, as appropriate

in the period when the forecasted transaction is recorded. The ineÅective portion of gains or losses

resulting from changes in fair value, if any, is reported in each period in interest and other income, net in

our Consolidated Statement of Operations. Our hedging programs reduce, but do not entirely eliminate,

the impact of currency exchange rate movements in revenue and operating expenses. As of March 31,

2006, we had no foreign currency option contracts outstanding. As of March 31, 2005, we had foreign

currency option contracts outstanding with a total fair value of $1 million included in other current assets.

We utilize foreign exchange forward contracts to mitigate foreign currency risk associated with foreign-

currency-denominated assets and liabilities, primarily intercompany receivables and payables. The forward

contracts generally have a contractual term of approximately one month and are transacted near month-

end. Therefore, the fair value of the forward contracts generally is not signiÑcant at each month-end. Our

foreign exchange forward contracts are not designated as hedging instruments under SFAS No. 133 and

are accounted for as derivatives whereby the fair value of the contracts are reported as other current assets

or other current liabilities in our Consolidated Balance Sheet, and gains and losses from changes in fair

value are reported in interest and other income, net. The gains and losses on these forward contracts

generally oÅset the gains and losses on the underlying foreign-currency-denominated assets and liabilities,

which are also reported in interest and other income, net, in our Consolidated Statement of Operations.

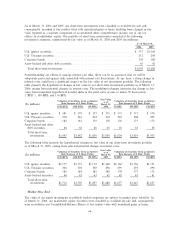

As of March 31, 2006, we had forward foreign exchange contracts to purchase and sell approximately

$161 million in foreign currencies. Of this amount, $132 million represented contracts to sell foreign

currencies in exchange for U.S. dollars, $14 million to sell foreign currencies in exchange for British pound

sterling and $15 million to purchase foreign currency in exchange for U.S. dollars. As of March 31, 2005

we had forward foreign exchange contracts to purchase and sell approximately $425 million of foreign

currencies. Of this amount, $379 million represented contracts to sell foreign currencies in exchange for

U.S. dollars, $22 million to sell foreign currencies in exchange for British pound sterling and $24 million to

purchase foreign currency in exchange for U.S. dollars. The fair value of our forward contracts was

immaterial as of March 31, 2006 and March 31, 2005.

The counterparties to these forward and option contracts are creditworthy multinational commercial banks.

The risks of counterparty nonperformance associated with these contracts are not considered to be

material.

Notwithstanding our eÅorts to mitigate some foreign currency exchange rate risks, there can be no

Annual Report

assurances that our hedging activities will adequately protect us against the risks associated with foreign

currency Öuctuations. As of March 31, 2006, we had no foreign currency option contracts outstanding. As

of March 31, 2005, a hypothetical adverse foreign currency exchange rate movement of 10 percent or

15 percent would not have resulted in a material loss in fair value of our option contracts under either

scenario. However, a hypothetical adverse foreign currency exchange rate movement of 10 percent or

15 percent would result in potential losses on our forward contracts of $16 million and $23 million,

respectively, as of March 31, 2006, and $40 million and $61 million, respectively, as of March 31, 2005.

This sensitivity analysis assumes a parallel adverse shift in foreign currency exchange rates, which do not

always move in the same direction. Actual results may diÅer materially.

Interest Rate Risk

Our exposure to market risk for changes in interest rates relates primarily to our short-term investment

portfolio. We manage our interest rate risk by maintaining an investment portfolio generally consisting of

debt instruments of high credit quality and relatively short maturities. Additionally, the contractual terms

of the securities do not permit the issuer to call, prepay or otherwise settle the securities at prices less than

the stated par value of the securities. Our investments are held for purposes other than trading. Also, we

do not use derivative Ñnancial instruments or leverage in our short-term investment portfolio.

63