Electronic Arts 2006 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2006 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

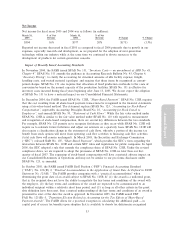

subsequent to adoption SFAS No. 123R. Accordingly, we may adopt either the method prescribed under

SFAS No. 123R or the one prescribed under FSP FAS No. 123(R)-3. We have not yet determined which

method to adopt. In February 2006, the FASB issued FSP FAS No. 123(R)-4, ""ClassiÑcation of Options

and Similar Instruments Issued As Employee Compensation That Allow for Cash Settlement upon the

Occurrence of a Contingent Event'', which amends certain paragraphs in SFAS No. 123R. FSP

FAS No. 123(R)-4 addresses situations when a company has option plans that require the company to

settle outstanding options in cash upon the occurrence of certain contingent events. Although we are

required to apply FSP FAS No. 123(R)-4 when we initially adopt SFAS No. 123R, we do not expect it

to impact our Consolidated Financial Statements.

In May 2005, the FASB issued SFAS No. 154, ""Accounting Changes and Error Corrections Ì A

Replacement of APB Opinion No. 20 and FASB Statement No. 3''. SFAS No. 154 changes the

requirements for the accounting and reporting of a change in accounting principle. Under previous

guidance, changes in accounting principle were recognized as a cumulative eÅect in the net income of the

period of the change. The new statement requires retrospective application of changes in accounting

principle, limited to the direct eÅects of the change, to prior periods' Ñnancial statements, unless it is

impracticable to determine either the period-speciÑc eÅects or the cumulative eÅect of the change.

Additionally, this Statement requires that a change in depreciation, amortization or depletion method for

long-lived, nonÑnancial assets be accounted for as a change in accounting estimate aÅected by a change in

accounting principle and that correction of errors in previously issued Ñnancial statements should be

termed a ""restatement''. SFAS No. 154 is eÅective for accounting changes and correction of errors made

in Ñscal years beginning after December 15, 2005. We do not believe that, upon adoption, SFAS No. 154

will have a material impact on our Consolidated Financial Statements, however, after adoption, if a change

in accounting principle is made, SFAS No. 154 could have a material impact on our Consolidated

Financial Statements.

In February 2006, the FASB issued SFAS No. 155, ""Accounting for Certain Hybrid Financial

Instruments Ì An Amendment of FASB Statements No. 133 and 140''. SFAS No. 155 (1) permits fair

value measurement for any hybrid Ñnancial instrument that contains an embedded derivative that

otherwise would require bifurcation, (2) clariÑes that interest-only strips and principal-only strips are not

subject to the requirements of SFAS No. 133, ""Accounting for Derivative Instruments and Hedging

Activities'', (3) establishes a requirement to evaluate interests in securitized Ñnancial assets to identify

interests that are freestanding derivatives or that are hybrid Ñnancial instruments that contain an embedded

derivative requiring bifurcation, (4) clariÑes that concentrations of credit risk in the form of subordination

are not embedded derivatives, and (5) amends SFAS No. 140, ""Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities Ì A Replacement of FASB Statement 125'' to

eliminate the prohibition on a qualifying special-purpose entity from holding a derivative Ñnancial

instrument that pertains to a beneÑcial interest other than another derivative Ñnancial instrument.

SFAS No. 155 is eÅective for all Ñnancial instruments acquired or issued for Ñscal years beginning after

September 15, 2006. We do not believe the adoption of SFAS No. 155 will have a material impact on our

Consolidated Financial Statements.

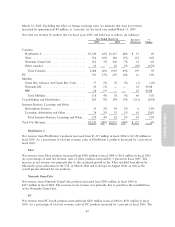

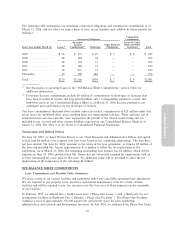

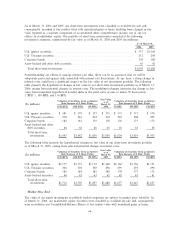

LIQUIDITY AND CAPITAL RESOURCES

Year Ended

March 31, March 31, Increase/

2006 2005 (Decrease)

(In millions)

Cash and cash equivalents ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $1,242 $ 1,270 $ (28)

Short-term investments ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $1,030 $ 1,688 $ (658)

Marketable equity securities ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 160 140 20

Total ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $2,432 $ 3,098 $ (666)

Percentage of total assets ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 55% 71%

54