Electronic Arts 2006 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2006 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

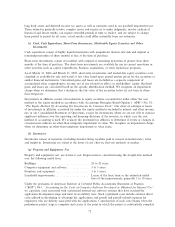

Statement No. 123(R)''. The FASB provides companies with a ""practical accommodation'' when

determining the grant date of an award subject to SFAS No. 123R. If (1) the award is a unilateral grant,

that is, the recipient does not have the ability to negotiate the key terms and conditions of the award with

the employer, (2) the key terms and conditions of the award are expected to be communicated to an

individual recipient within a relatively short time period, and (3) as long as all other criteria in the grant

date deÑnition have been met, then a mutual understanding of the key terms and conditions of an award is

presumed to exist at the date the award is approved.

In November 2005, the FASB issued FSP FAS No. 123(R)-3, ""Transition Election Related to

Accounting for the Tax EÅects of Share-Based Payment Awards''. The FASB allows for a practical

exception in calculating the additional paid-in capital pool of excess tax beneÑts upon adoption that is

available to absorb tax deÑciencies recognized subsequent to adoption SFAS No. 123R. Accordingly, we

may adopt either the method prescribed under SFAS No. 123R or the one prescribed under FSP

FAS No. 123(R)-3. We have not yet determined which method to adopt.

In February 2006, the FASB issued FSP FAS No. 123(R)-4, ""ClassiÑcation of Options and Similar

Instruments Issued As Employee Compensation That Allow for Cash Settlement upon the Occurrence of a

Contingent Event'', which amends certain paragraphs in SFAS No. 123R. FSP FAS No. 123(R)-4

addresses situations when a company has option plans that require the company to settle outstanding

options in cash upon the occurrence of certain contingent events. Although we are required to apply FSP

FAS No. 123(R)-4 when we initially adopt SFAS No. 123R, we do not expect it to impact our

Consolidated Financial Statements.

(p) Foreign Currency Translation

For each of our foreign operating subsidiaries the functional currency is generally its local currency. Assets

and liabilities of foreign operations are translated into U.S. dollars using month-end exchange rates, and

revenue and expenses are translated into U.S. dollars using average exchange rates. The eÅects of foreign

currency translation adjustments are included as a component of accumulated other comprehensive income

in stockholders' equity.

Foreign currency transaction gains and losses are a result of the eÅect of exchange rate changes on

transactions denominated in currencies other than the functional currency. Foreign currency transaction

gains (losses) of $(1) million, $25 million and $44 million for the Ñscal years ended March 31, 2006,

2005 and 2004, respectively, are included in interest and other income, net, in our Consolidated

Statements of Operations.

Annual Report

(q) Impact of Recently Issued Accounting Standards

In November 2004, the FASB issued SFAS No. 151, ""Inventory Costs Ì an amendment of ARB No. 43,

Chapter 4''. SFAS No. 151 amends the guidance in Accounting Research Bulletin No. 43, Chapter 4,

""Inventory Pricing'', to clarify the accounting for abnormal amounts of idle facility expense, freight,

handling costs, and wasted material (spoilage) and requires that those items be recognized as current-

period charges. SFAS No. 151 also requires that allocation of Ñxed production overheads to the costs of

conversion be based on the normal capacity of the production facilities. SFAS No. 151 is eÅective for

inventory costs incurred during Ñscal years beginning after June 15, 2005. We do not expect the adoption

of SFAS No. 151 to have a material impact on our Consolidated Financial Statements.

In May 2005, the FASB issued SFAS No. 154, ""Accounting Changes and Error Corrections Ì A

Replacement of APB Opinion No. 20 and FASB Statement No. 3''. SFAS No. 154 changes the

requirements for the accounting and reporting of a change in accounting principle. Under previous

guidance, changes in accounting principle were recognized as a cumulative eÅect in the net income of the

period of the change. The new statement requires retrospective application of changes in accounting

principle, limited to the direct eÅects of the change, to prior periods' Ñnancial statements, unless it is

impracticable to determine either the period-speciÑc eÅects or the cumulative eÅect of the change.

Additionally, this Statement requires that a change in depreciation, amortization or depletion method for

77